Google Cloud Will Not Be Able To Overtake Microsoft Azure

December 08, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Dec 3, 2020,11:03pm EST

Google Cloud certainly has the technical chops and engineering talent to compete with Microsoft Azure and Amazon’s AWS when it comes to cloud infrastructure, edge computing – and especially inferencing/training for machine learning models. However, Google may lack focus due to Search and YouTube being the main revenue drivers. This is seen from the company’s inability to ignite revenue growth in the cloud segment during a year when digital transformation has been accelerated by up to six years due to work-from-home orders.

In this analysis, we discuss why Google (Alphabet) may have missed a critical window this year for the infrastructure piece. We also analyze how Microsoft directed all of its efforts to successfully close the wide lead by AWS. Lastly, we look at how all three companies will bring the battle to the edge in an effort to maintain market share in this secular and fiercely competitive category.

Cloud IaaS Overview:

The three leading hyperscalers in the United States have diverse origins. Amazon found itself serendipitously holding server space year-round that it could rent out and was first to market by a wide lead. Amazon continues to release customization tools and cloud services for developers at a fast clip and this past week was no exception.

Microsoft’s roots in enterprise created a direct path to upsell on-premise and become the leader in hybrid. The majority of the Fortune 500 is on Azure as they want seamless security and APIs regardless of the environment.

Google is one of the largest cloud customers in the world due to its search engine and mass-scale consumer apps, and therefore, is often first to create cloud services and architectures internally that later lead to widespread adoption, such as Kubernetes. Machine learning is another piece where Google was one of the first to require ML inference for mass-scale models.

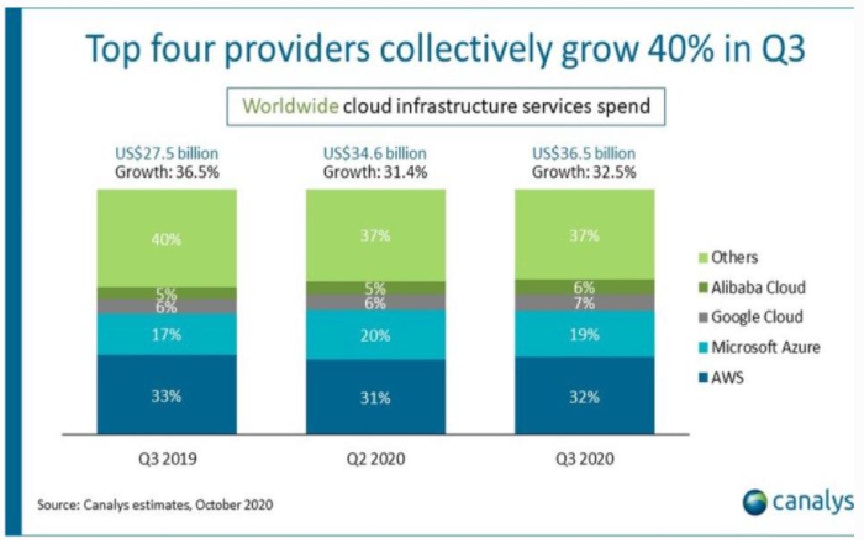

Despite all three having very talented teams of engineers and various areas of strength, we see AWS maintain its lead and Microsoft Azure firmly hold the second-place spot. Keep in mind that Azure launched one year after Google Cloud yet has 3X the market share and is growing at a higher percentage.

CANALYS

Google Cloud grew two percentage points from 5% to 7% since 2018 while Azure grew four percentage points from 15% to 19% in the same period. In the past year, Google Cloud saw a 1% gain compared to Azure’s 2% gain, according to Canalys.

Azure is under Intelligent Cloud but the company does break down the growth rate which was 48%. Although Google Cloud Is not specifically broken down, the Google Cloud segment grew 45% year-over-year compared to Microsoft Azure up 48% year-over-year.

Amazon Web Services is growing at 29%, which is substantial considering the law of large numbers. In the past two quarters, Google Cloud reported 43% year-over-year growth and 52% in the quarter before that. Microsoft has seen a slightly less deceleration from 51% and this is down from the 80%-range almost two years ago.

The key thing here is that when Microsoft held the percentage of market share that GCP currently holds, Azure was growing in the 80-90% range. This is the range we should be seeing from Google Cloud if the company expects to catch up to Azure.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

In 2020, the term “digital transformation” has become a buzzword with cloud companies seeing up to six years of acceleration. Nvidia is a bellwether for this with triple-digit growth in the data center segment in both Q2 and Q3. Despite this catalyst, Google has lagged the category in Q2 and Q3 in terms of both growth and percentage share of market. If there were any year that Google Cloud could pull ahead, it should have been this year.

Alphabet has emphasized that GCP is a priority and the company will be “aggressively investing” in the necessary capex. However, the window of opportunity was wide open this year and aggressive investments would ideally have been allocated during the years of 2017-2018 to stave off Azure’s high-growth years with 80-90%.

Google is Capable but Lacks Focus

There is no argument that Alphabet is an innovator within cloud and a leader in its own right. Across public, private and hybrid cloud, containers are used by 84% of companies and 78% of those are managed on Kubernetes – which has risen in popularity along with cloud-native apps, microservices architectures and an increase in APIs. Kubernetes was first created by Google engineers as the company ran everything in containers internally and this was powered by an internal platform called Borg which generated up to 2 billion container deployments a week. This led to automated orchestration rather than manual and also forced a new architecture away from monolithic as server-side changes were required.

Kubernetes also helps with scaling as it allows for scaling of the container that needs more resources instead of the entire application. Microservices dates back to Unix, while Kubernetes, the automation piece around containers, is what Google engineers invented before releasing it to the Cloud Native Foundation for widespread adoption.

Just as Google was one of the first to need automated orchestration for containerization of cloud-native apps, the company was also one of the first to require low-power machine learning workloads. The compute intensive workloads were running on Nvidia’s GPUs for both training and inferencing until Google made their own processing unit called Tensorflow (TPUs) to perform the workload at a lower cost and higher performance.

Performance between TPUs and GPUs is often debated depending on the current release (A100 versus fourth-generation TPUs is the current battle). However, the TPU does have an undisputed better performance per watt for power-constrained applications. Notably, some of this comes with the territory of being an ASIC, which is designed to do one specific application very well whereas GPUs can be programmed as a more general-purpose accelerator. In this case, the benchmarks where TPUs compete are object detection, image classification, natural language processing and machine translation – all areas where Google’s product portfolio of Search, YouTube, AI assistants, and Google Maps, for example, excels.

Notably, TPUs are used internally at Google to help drive down the costs and capex of its own AI and ML portfolio and they are also available to users of Google’s AI cloud services. For example, eBay adopted TPUs to build a machine learning solution that could recognize millions of product images.

Unless Google releases an internal technology as open-source, it won’t be adopted by the competitors. This is where Nvidia’s agnosticism becomes a positive as it’s universally used by Amazon, Microsoft, Google —- and Alibaba, Baidu, Tencent, IBM and Oracle. Meanwhile, TPUs create vendor lock in which most companies want to avoid in order to get the best capabilities across multiple cloud operators (i.e. multi-cloud). eBay is the exception here as the company needs Google-level object detection and image classification.

In a similar vein of Google being early to the company’s internal requirements, BigQuery is also a superior data warehouse system that competes with Snowflake (I cover Snowflake with an in-depth analysis here). BigQuery has a serverless feature that makes it easier to begin using the data warehouse as the serverless feature removes the need for manual scaling and performance tuning. Dremel is the query engine for BigQuery.

BigQuery has a strong following with nearly twice the number of companies as Snowflake and is growing around 40%. Due to AWS being a first mover and having a large cloud IaaS market share, Redshift has the biggest market presence but growth is nearly flat at 6.5%.

Point being, Google has important areas of strength and first-hand experience – whether it’s in data analytics, machine learning/inference or cloud-native applications at scale. Google’s search engine and other applications are often the first globally to challenge current architectures and inferencing capabilities.

However, as we see in the contrast between Google and Microsoft in the most recent earnings calls, Google has a hard time prioritizing cloud over the bigger revenue drivers. Meanwhile, Microsoft has a no holds barred approach with one, singular focus: Azure.

Q3 Earnings Calls

The most recent earnings calls from both Microsoft and Google could not have carried more contrast. Google focused primarily on search and YouTube while adding towards the last half of the call that GCP is where the majority of their investments and new hires were directed. Notably, one analyst wondered if the capex investments would eat at margins and produce enough returns.

Microsoft, on the other hand, held an hour-long call that was nearly all-Azure including what the company is doing right now to capture more market share, a laundry list of large enterprises coming on board and strategic partnerships to strengthen its second place standing. The company’s beginning, middle and end was Azure and cloud services.

Here is a preview of how the two opened:

Thanks for joining us today. This quarter, our performance was consistent with the broader online environment. It's also testament to the investment we've made to improve search and deliver a highly relevant experience that people turn to for help in moments big and small. We saw an improvement in advertiser spend across all geographies, and most of verticals, with the world accelerating its transition to online and digital services. In Q3, we also saw strength in Google Cloud, Play and YouTube subscriptions.

This is the third quarter we are reporting earnings during the COVID-19 pandemic. Access to information has never been more important. This year, including this quarter showed how valuable Google's founding Product Search has been to people. And importantly, our products and investments are making a real difference as businesses work [indiscernible] and get back on their feet. Whether it's finding the latest information on COVID-19 cases in their area, which local businesses are open, or what online courses will help them prepare for new jobs, people continue to turn to Google search.

You can now find useful information about offerings like no contact delivery or curbside pickup for 2 million businesses on search and maps. And we have used Google's Duplex AI Technology to make calls to businesses and confirm things like temporary closures. This has enabled us to make 3 million updates to business information globally.

We know that people's expectations for instant perfect search results are high. That's why we continue to invest deeply in AI and other technologies to ensure the most helpful search experience possible. Two weeks ago, we announced a number of search improvements, including our biggest advancement in our spelling systems in over a decade. A new approach to identifying key moments and videos, and one of people's favorites hum to search which will identify a song noticed based on the humming. -Sundar Pichai, Q3 2020 Earnings Call

Compare this to the tone for Microsoft’s earnings call …

We’re off to a strong start in fiscal 2021, driven by the continued strength of our commercial cloud, which surpassed $15 billion in revenue, up 31% year-over-year. The next decade of economic performance for every business will be defined by the speed of their digital transformation. We’re innovating across the full modern tech stack to help customers in every industry improve time to value, increase agility, and reduce costs.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Now, I’ll highlight examples of our momentum and impact starting with Azure. We’re building Azure as the world’s computer with more data center regions than any other provider, now 66, including new regions in Austria, Brazil, Greece, and Taiwan. We’re expanding our hybrid capabilities so that organizations can seamlessly build, manage, and deploy their applications anywhere. With Arc, customers can extend Azure management and deploy Azure data services on-premise, at the edge, or in multi-cloud environments.

With Azure SQL Edge, we’re bringing SQL data engine to IoT devices for the first time. And with Azure Space, we’re partnering with SpaceX and SES to bring Azure compute to anywhere on the planet.

Leading companies in every industry are taking advantage of this distributed computing fabric to address their biggest challenges. In energy, both BP and Shell rely on our cloud to meet sustainability goals. In consumer goods, PepsiCo will migrate its mission critical SAP workloads to Azure. And with Azure for Operators, we’re expanding our partnership with companies like AT&T and Telstra, bringing the power of the cloud and the edge to their networks. Just last week, Verizon chose Azure to offer private 5G mobile edge computing to their business customers. -Satya Nadella, Fiscal Q1 2021 Earnings (Calendar Year Q3 2020)

The calls continue in a similar manner with Microsoft making it clear they have their entire weight behind cloud while Google must continue to cater to its largest revenue drivers – search and consumer. The main takeaway we get from the call is that Google is investing in GCP rather than a takeaway of market dominance or growth. Here are a few examples:

As we’ve told you on these calls, given the progress we’re making, and the opportunity for Google Cloud in this growing global market, we continue to invest aggressively to build our go-to-market capabilities, execute against our product roadmap, and extend the global footprint of our infrastructure … And another: An obvious example is Cloud. We do intend to maintain a high level of investment, given the opportunity we see. That includes the ongoing increases in our go-to-market organization, our engineering organization, as well as the investments to support the necessary capex. So, hopefully, that gives you a bit more color there. And, also here … And the point that both Sundar and I have underscored is that we are investing aggressively in Cloud, given the opportunity that we see. And, frankly, the fact that we were later relative to peers, we're encouraged, very encouraged, by the pace of customer wins and the very strong revenue growth in both GCP and Workspace. We do intend to maintain a high level of investment to best position ourselves. And I kind of went through some of those items, the go-to-market team, the engineering team, and capex. And so we describe this as a multi-year path because we do believe we're still early in this journey.

The question remains if aggressively investing will have the same impact after the digital transformation has been accelerated by up to six years. Nobody could have predicted covid and the work-from-orders but we see from the growth rates on large revenue bases that AWS and Azure were better positioned to answer the demand.

Edge Computing: No rest for the weary

The race for cloud IaaS dominance is only beginning and the hyperscalers are not resting on their laurels as they compete for the edge. Major strategic partnerships are being struck with telecom companies to break open new uses cases for decentralized applications and increased connectivity. Google mentioned Nokia in their earnings call while Microsoft mentioned AT&T, Verizon and Telstra. Amazon also has partnerships with Verizon and Vodafone. (For brevity sake, you can assume every telecom company is either partnered or will be partnering with multiple hyperscalers for edge computing).

Here is a breakdown of the buildout and how these strategic partnerships plan to profit from 5G. The result will be new use cases, such as remote surgery, autonomous vehicles, AR/VR and a significant number of internet of things devices that aren’t feasible with 4G and/or with the current centralized cloud IaaS servers.

AWS Wavelength:

Amazon’s edge computing technologies are being rapidly built-out. For example, Wavelength is being embedded in Vodafone’s 5G networks throughout Europe in 2021 after being in beta for two years. This will provide ultra-low latency for application developers enabled by 5G. On Vodafone’s end, they have developed multi-access edge computing (MEC) to fit both 4G and 5G networks to process data and applications at the edge. This lowers processing time from about 50-200 milliseconds to 10 milliseconds. Amazon is also expanding its Local Zones to offer low-latency in metro areas from L.A. to about a dozen cities in 2021.

In order to support its retail business, AWS built out 200 points of presence where serverless processing like Lambda can run. The network latency map will be enhanced by telco partnerships who have about 150 PoPs per telco.

Microsoft Azure with Edge Zones:

Azure has the largest global footprint across the cloud providers. Where AWS has been the long-standing developer preference, Microsoft is the C-suite/enterprise preferred company across the Fortune 500. Microsoft’s goal will be to move compute closer to end users and to offer Azure-hosted compute and storage as a single virtual network with security and routing.

Microsoft excelled at hybrid as a strategy for taking market share (which I also detailed as the investment thesis for my position in Microsoft after the company missed Q3 2018 earnings and prior to winning the JEDI contract). Azure Edge Zones extends the current hybrid network platform to allow distributed applications to work across on-premise, edge data centers both public and private, Azure IaaS both public and private. This allows the same security and APIs to work seamlessly across these hybrid environments. The overarching performance will attempt to combine the range of compute and storage capabilities of Azure with the speeds/low-latency of the edge.

Google Cloud with Global Mobile Edge Cloud (GMEC):

Google is also partnering with telecom companies such as AT&T to deploy Google hardware inside AT&T’s network edge to run AI/ML models and other software for 5G solutions. Similar to AWS and Azure, the goal is to open up new use cases for industries, such as retail, manufacturing and transportation.

Anthos for Telecom is a Kubernetes-orchestrated infrastructure that can be deployed anywhere including an AWS cluster. In this way, the strategy for Google continues to amplify its strengths which is containerized network functions to merge edge and core infrastructure. This helps with decentralized applications and could potentially compete with “network slices” to where AT&T could potentially use local breakouts to offer a cloud service tier in a few years from now.

Conclusion:

We’ve seen Google build some of the best products for developers in terms of automating microservices and container-orchestration with Kubernetes and also ASIC chips (TPUs) that compete with the likes of Nvidia. I’m not betting against Google’s talented engineers by any means, rather I’m simply observing that the infrastructure piece is leaning towards more of a duopoly at this time. Cloud is expensive on a capex level, so if Google doesn’t find its footing, the margins driven by ads could take a hit in the near-term.

Who will lead software and AI applications is impossible to predict (and when) as the main competitors will be hundreds (if not thousands) of startups. With that said, I personally own Amwell because Google is a backer and I think health care is an example of a vertical where Google’s experience with data can deliver a serious competitive edge. To be clear, Alphabet may have an advantage with AI/ML software whereas this analysis is about the infrastructure. Perhaps there will be a catalyst in the future for Google Cloud to take more share but the strategy is not evident at this time.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per