I/O Fund’s preview of 7 Ad-Tech stocks for Q4 Earnings

February 04, 2022

Royston Roche

Equity Analyst

Google parent Alphabet’s results have further renewed optimism in the stock market as the company beat analysts’ revenue estimates by 4.9% and EPS by 13%. It was led by the growth in advertising and cloud revenues. Advertising revenue grew by 33% to $61.24 billion. The company also announced the 20-for-1 stock split.

On the other hand, Facebook’s results disappointed as it missed analysts' EPS estimates by 4% and only managed to beat revenue estimates by 0.7%. The revenue outlook for the next quarter also disappointed the Street since it only expects revenue to grow in the range of 3-11% YoY. Revenue in Q4 grew by 20% to $33.67 billion. We have stayed away from the stock due to the various privacy issues and failed efforts to enter new markets like stable coins and dating. Not to mention the Cambridge Analytical data scandal.

Snap Inc. reported on February 3rd and results came in relatively stronger than Meta’s. Snap guided for sales to grow 36% YoY next quarter, well above Meta’s guide for 7% YoY growth at the mid-point. The large disparity between Snap and Meta’s forward guide highlights that Apple’s changes to iOS will have varying degrees of impacts on companies in the ad-tech space. The stock is up 59% after hours following the positive report while Facebook is down 28% following its report.

In this earnings preview, we cover Digital Turbine, Twitter, HubSpot, Trade Desk, Roku, Magnite, and PubMatic. To understand valuations across the Ad-Tech companies and how the sector is positioned moving into earnings, please reference our analysis, “I/O Fund’s Ad-Tech Q4 2021 Earnings Overview.”

Digital Turbine – Earnings on February 08th

Source: YCharts, Earnings Reports, and I/O Fund

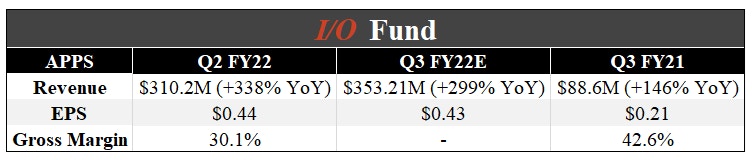

The company’s revenue grew 338% YoY to $310.2 million. However, the company’s results include AdColony and Fyber results which were acquired earlier this year. For better comparison, the management provides pro forma revenue growth i.e. 63% YoY. The analyst’s consensus estimates suggest revenue to grow 299% to $353.21 million in the next quarter.

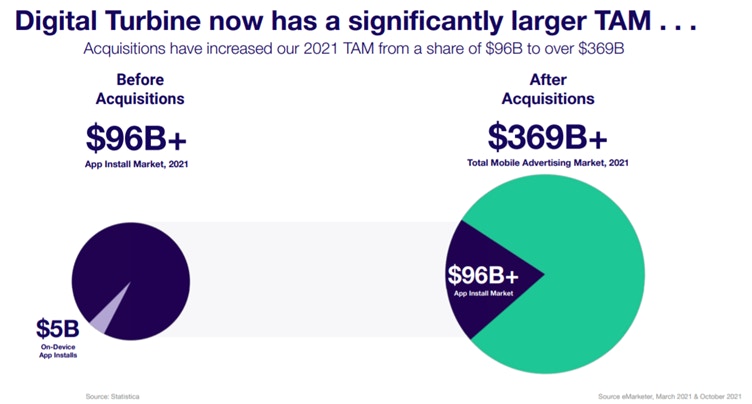

The management believes that the company’s current Total Addressable Market has significantly increased from about $96 billion to about $369 billion due to the various acquisitions.

Source: Analyst Day Presentation

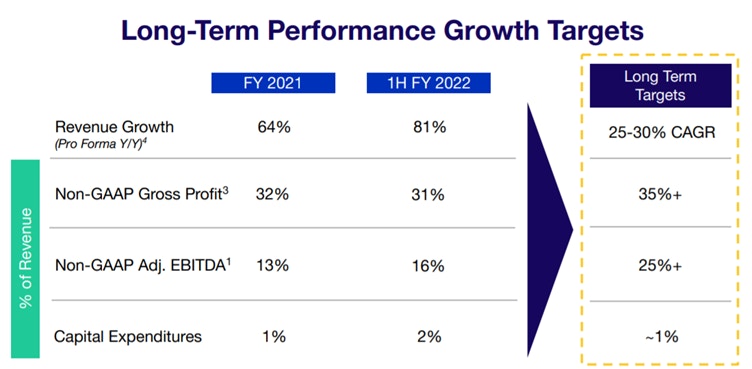

The company expects organic revenue to grow 25-30% in the long term.

Source: Analyst Day Presentation

Macquarie analyst Tim Nollen has an outperform rating and a price target of $80. He is bullish on the company due to “Industry and macro tailwinds (secular growth in mobile gaming and digital ads, alongside lower app store fees); an expansion into brand advertising (a $400 billion-plus total addressable market); upside to current estimates; and the attractive valuation.”

Roth Capital Partners analyst Darren Aftahi has a price target of $90. He is positive on the +25% revenue growth, the SingleTap feature, and also on the company’s various partnerships. “Therefore, not only can [Digital Turbine] expand its wallet share on existing devices, it can capture additional upside and long-tail revenues on new devices as well, especially with market expansion outside the U.S. given various partnerships with Samsung, Telefonica and others.”

Please note that the I/O Fund may or may not agree with the above financial analysts, yet we objectively report what the Street is saying. You may view our previous analysis of the company below:

Q3 Stock Earnings Preview - What to Expect for 7 Ad Tech Stocks

Ad Tech Stock Earnings - What to Expect for Q3 2021 Earnings

Twitter Inc – Earnings on February 10th

mDAU: Monetizable Daily Active Usage

Source: YCharts, Earnings Reports, and I/O Fund

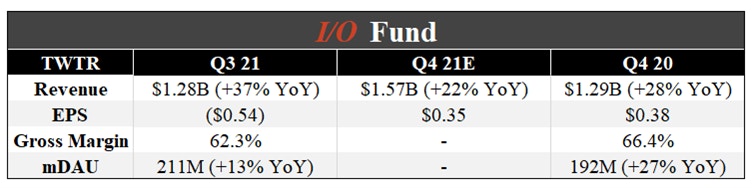

The company’s revenue grew 37% in Q3 and the consensus forecast suggests revenue to grow 22% to $1.57 billion in the next quarter. It will be the first earnings call for the new CEO, Parag Agrawal. In the Barclays Tech Conference, he mentioned his priorities include smooth transition to all the stakeholders and improving the execution to deliver great products and results.

Truist analyst Youssef Squali has a buy rating and a $50 price target. He believes, “The company's Q4 revenue growth should decelerate sequentially to 22% from 37% in Q3, reflecting tough Y/Y comps, and normalization from peak engagement on the platform due to COVID.” However, he still expects over 20% growth, led by healthy ad budgets, new monetization tools, and mDAU growth.

Mizuho analyst James Lee lowered the company’s price target to $56 from $70. He has a neutral rating on the stock. In his view, “While the management changes are necessary to enable Twitter to accelerate the development, introduction, and update of its products, it could take time for the new strategy to take shape for users and revenues to reach the company's long term targets.”

Read our previous article on the company below:

I/O Fund’s Interview with CoinDesk: Why Square’s Name Change to Block is Defensive

Social Media Projected to Lead Global Ad Spend in 2021

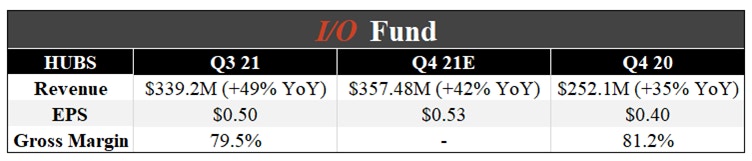

HubSpot Inc – Earnings on February 10th

Source: YCharts, Earnings Reports, and I/O Fund

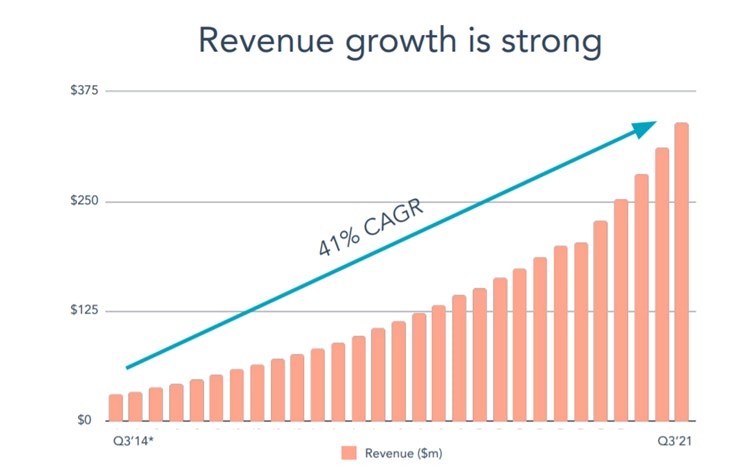

HubSpot’s Q3 revenue grew 49% to $339.2 million. The company’s total number of customers increased 34% to 128,144. The consensus analysts’ estimates suggest revenue to grow 42% in the next quarter. The company’s revenue growth has been good since it grew at a compound annual growth rate of 41% from its IPO in October 2014 till Q3 2021.

Source: Investor Presentation

Mizuho analyst Siti Panigrahi has lowered the company’s price target to $500 from $790 and has a buy rating on the stock. In his view, “Software-as-a-service momentum has stalled thus far in 2022 amid concerns over rising interest rates.” However, the analyst does not see any deterioration of fundamentals despite the market sell-off. On the other hand, Barclays has also lowered the price target to $550 from $800.

Goldman Sachs analyst Gabriel Borges has a buy rating and a $953 price target. The analyst notes that the company responded positively during the early days of the Covid-19 pandemic. He points out that the company lowered the starter package price and introduced a freemium product, which led to the increase of the customers. Over a period of time, he sees a potential for its customers to move to a higher-priced plan.

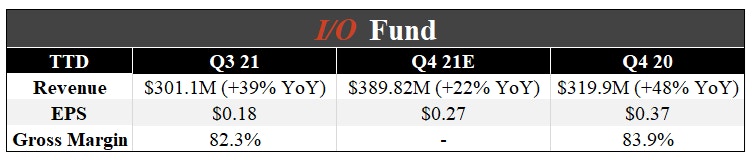

The Trade Desk Inc – Tentative Earnings Date is February 18th

Source: YCharts, Earnings Reports, and I/O Fund

The company's Q3 revenue grew 39% YoY to $301.1 million, excluding the political spend related to the previous year's U.S. elections; the growth was about 47%. The consensus analysts' estimates suggest revenue to grow 22% to $389.82 million. The management expects Q4 revenue to be about $388 million. It did not give specific guidance and mentioned about the uncertainty to the advertising industry due to rising Covid-19 cases. In the earnings call, founder and CEO Jeff Green mentioned that the IOS changes did not have any material impact on the company's business.

Jefferies has upgraded the stock to a buy rating and has a price target of $105. In his view, "Broadening adoption of connected TV viewership is driving more dollars toward programmatic advertising, from linear TV; the Solimar product launch is the biggest since Next Wave, which drove an acceleration in rev growth following its mid-2018 launch; and TTD is in a relatively better position to weather the privacy changes from Apple's iOS 14, compared to Walled Garden names like FB and SNAP."

On the other hand, Stifel analyst Mark Kelley has resumed coverage on the stock with a hold rating and a price target of $68. He says that the feedback he heard about the stock is positive. He also believes that Connected TV advertising still has room to improve. However, he sees the company's shares are "stretched at current levels."

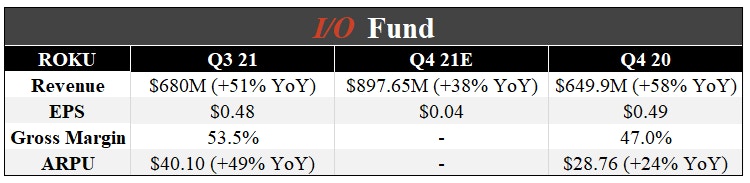

Roku Inc - Tentative Earnings Date is February 18th

Source: YCharts, Earnings Reports, and I/O Fund

The company’s Q3 revenue grew 51% to $680 million and the analysts' consensus estimate suggests revenue to grow 38% to $897.65 million in the next quarter. The management expects revenue in the range of $885 million to $900 million and adjusted EBITDA of $65 million to $75 million. The company’s active accounts at the end of Q3 were 56.4 million, a net addition of 1.3 million in Q3.

According to the NPD's Weekly Retail Tracking Service, the company has been the top-selling smart TV operating system for the second consecutive year in the U.S. Also, according to the study conducted by Hypothesis Group, Roku is Canada's number 1 streaming platform. On other recent news, Fox News International announced that it is expanding distribution on Roku, which should supplement Roku’s international growth.

Deutsche Bank analyst Jeffrey Rand has lowered the company’s price target to $300 from $400 and has kept the buy rating on the stock. He believes that the company is well-positioned in the rapidly growing connected TV market and the recent sell-off is overdone. Q4 earnings could be a positive catalyst for the stock. His checks indicate that the advertising market remained strong in Q4 despite some initial concerns about brands reducing ad spending due to supply chain issues.

Read our previous article on the company below:

Podcast: This Week in Startups and I/O Fund on Tech Investing

The Crucial Difference Between Roku and Netflix

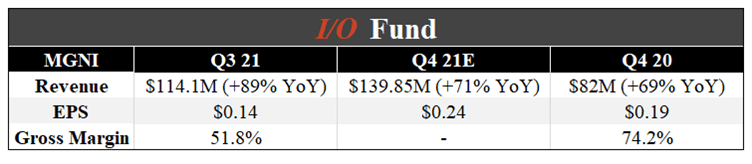

Magnite Inc – Earnings on February 23rd

Source: YCharts, Earnings Reports, and I/O Fund

The company completed the acquisitions of SpotX and SpringServe this year. Revenue excluding traffic acquisition cost (TAC) was $114.1 million, up 89% and up 26% on a pro forma basis (SpotX and SpringServe included in Q3 20 for comparisons). The consensus analysts’ estimates suggest revenue ex-TAC to grow 71% to $139.85 million. Management expects revenue ex-TAC in the range of $138 million to $142 million.

Truist analyst Matthew Thornton has a price target of $23 and a Buy rating. The analyst believes that the setup could be interesting into the second half of the year on easing supply chain issues and the stock trading 13-times and 11-times expected FY22 and FY23 adjusted EBITDA. He further notes that the Q4 consensus expectations are reasonable but a bit cautious on Q1.

Needham analyst Laura Martin has a buy rating on the stock but has lowered the price target from $70 to $25. The analyst highlights broader short-term concerns like tougher comps, supply chain concerns, and omicron variant slowing digital ad growth for companies under her Streaming and AdTech coverage that drove multiple compression last year and in 2022-to-date.

Read our previous article on the company below:

Will Dividend Stocks Become the Inflation Trade?

Podcast with Motley Fool: I’m Bullish on These Trends for 2021

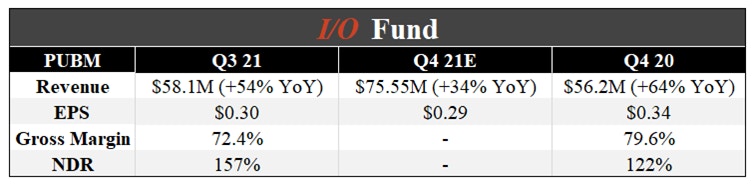

PubMatic Inc – Earnings on February 28th

Source: YCharts, Earnings Reports, and I/O Fund

PubMatic’s revenue grew by 54% in Q3 and is expected to grow 34% in the next quarter to $75.55 million. The company’s revenue grew at over 50% in the previous four quarters. It also has an excellent net-dollar retention rate (NRR) of 157% for the trailing twelve months ended September 2021.

In the words of the company’s CEO, “We use a land and expand approach, coupled with a usage-based revenue model. When we deliver incremental value to our customers, we participate in their upside which further accelerates our profitable business model and enables us to invest for future growth. This flywheel positions us well for sustained and profitable growth and market share gains.”

The management expects revenue in the range of $74 million to $76 million, representing a growth of about 34%. It had raised the full-year 2021 guidance from the range of $205 million-$209 million to the range of $225 million-$227 million, representing a growth of about 52%. It also expects the full-year 2022 revenue to be at least $281 million.

Jefferies has been positive about the company as they believe that the recent iOS changes will not have much impact on the company. They also point out that the company has been trading below its historical averages.

The I/O Fund is a team of analysts who share their research publicly as they build a portfolio of 20 stocks. Our team has record results for a retail Fund and we also have four-digit gains on some of our free newsletter coverage. You can learn more about our premium service by clicking here or sign up for our free newsletter here.

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i