Why Nvidia Stock Could Reach a $20 Trillion Market Cap by 2030

November 19, 2025

Beth Kindig

Lead Tech Analyst

The statement that Nvidia stock could reach a $20 trillion market cap by 2030 will trigger plenty of emotion — it sounds fantastical, full of hype, or like a prediction made far too early in the AI cycle. Yet what I offer you below is a data-driven, fundamentally grounded case for how Nvidia can realistically reach a $20 trillion valuation by 2030.

When it comes to Nvidia’s AI story, I’ve offered the earliest and most consistent analysis, covering the company’s AI trajectory earlier than anyone on record. For instance, I told my premium stock research members in September of 2019 that Nvidia would become one of the world’s most valuable companies when it was only a $110 billion valuation (it’s now up 40X). I also publicly stated that Nvidia would surpass Apple when Nvidia had just one-fifth of Apple’s market cap — $550 billion versus $2.5 trillion — writing: “The conclusion to my analysis is the same as the introduction, which is that I believe Nvidia is capable of outperforming all five FAAMG stocks and will surpass even Apple’s valuation in the next five years.” Fast forward and Nvidia stock is up 8X since that analysis.

Last year, when Nvidia stock was valued at $3 trillion, I projected the stock would reach $10 trillion market cap by 2030 — a forecast that no longer looks aggressive now that the stock has briefly broken above $5 trillion. Today, with an even clearer view into the company’s product cadence, software moat, and AI systems dominance, my new, updated thesis is that Nvidia’s stock is on track to reach a $20 trillion market cap by 2030.

This is supported by Nvidia’s aggressive 1-year product roadmap, an impenetrable software ecosystem through CUDA, and its evolution into a full-stack AI systems provider. When these elements are modeled together — alongside the rapid expansion in global AI infrastructure capex — the path to $20 trillion becomes less sensational and more a reflection of compounding fundamentals.

Nvidia’s Data Center Needs to Grow at 36% CAGR to Reach $20T Market Cap

To get down to brass tacks, Nvidia will have to grow its data center segment at a 36% CAGR to reach a $20 trillion market cap if we assume its 5-year median sales valuation of 25 forward PS remains intact. This will put the company’s data center revenue at a run rate in the mid-$900 billion range.

Pictured above: Nvidia stock could see a $20 trillion market cap by 2030 based on a 36% CAGR in its data center segment

About eighteen months ago, I highlighted the importance of Nvidia reaching a $50 billion data center segment by year-end in the article, Here's Why Nvidia Stock Will Reach $10 Trillion Market Cap By 2030, stating:

In my analysis last month on the Blackwell architecture, I made the argument these estimates are too low and that my firm expects we will see a $200 billion data center segment by end of CY2025 propelled forward by the B100, B200 and GB200, including the following points: “Taiwan Semi’s CoWos capacity, which is essential for Blackwell’s architecture, is estimated to rise to 40,000 units/month by the end of 2024, which is more than a 150% YoY increase from ~15,000 units/month at the end of 2023. Applied Materials has boosted its forecast for HBM packaging revenue from a prior view for 4X growth to 6X growth this year.”

The data center segment for Nvidia of $320 billion by 2027 would result in 260% growth for Nvidia’s DC from where it stands today and up 120% from DC revenue estimates for end of CY2025.”

It’s highly probable that Nvidia will blow past the $50 billion data center segment mark this evening - one quarter earlier than my original prediction - which puts the company on the path for a $75 billion segment in Q4 of next year. Tracking these milestones is crucial as it helps support that Nvidia is well on its way to reaching my firm’s brand-new updated estimate for a $230 billion data center quarter by Q4 of 2030 or $930 billion for the full year.

Industry analysts have AI accelerators growing at 31.5% CAGR through 2033 with McKinsey putting out a prediction for $7 trillion in AI infrastructure spend through 2030 with $5.2 trillion going toward building data centers for AI workloads. Dr. Lisa Su and Jean Hsu echoed McKinsey’s projections, stating the AI data center market could be worth $1 trillion by 2030, referring to the addressable market of AI accelerators where AMD competes.

mid

Regardless of which way you dice it, industry estimates point toward AI spend exceeding current expectations. For example, Dr. Su originally had predicted a $500 billion market by 2028. Her updated forecast assumes 35% growth over the next three to five years – the same growth rate required for Nvidia to reach the assumptions underpinning my thesis for a $20 trillion market-cap scenario.

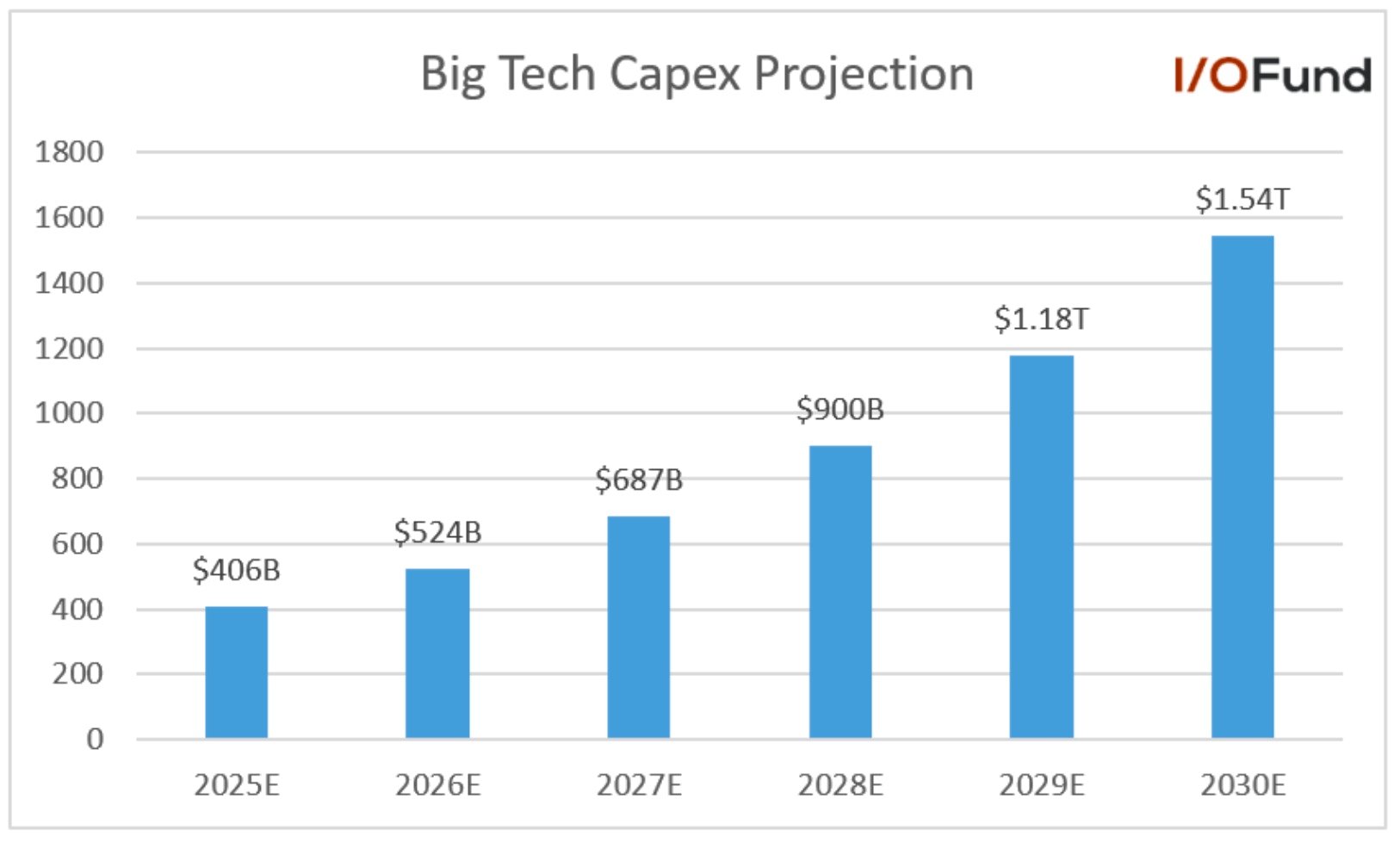

McKinsey’s $5.2 trillion AI infrastructure forecast implies roughly $1.5 trillion in annual AI spending by 2030. Under this framework, our assumptions are slightly on the aggressive side, as they imply Nvidia captures about 60% of total AI capex. Back-of-the-napkin math suggests Nvidia is currently capturing closer to 50% of AI spend, given today’s $405 billion capex run rate and Nvidia’s data center segment set to surpass a $200 billion run rate in this evening’s report.

Pictured above: Big Tech AI Capex expected to surge from $406B in 2025 to over $1.5 trillion by 2030, reflecting the massive growth in the AI data center market.

Offense is the Best Defense: Nvidia’s Rapid Product Road Map

The saying goes “the best offense is the best defense” and Nvidia is fully applying this philosophy by leading with its design prowess to ensure custom silicon cannot replace its lead in AI systems. There will certainly be a market for custom silicon as it excels at application specific workloads, which is attractive to Big Tech companies that can use custom silicon to optimize their recommendation engines, run inference at scale and optimize specific internal models. However, custom silicon cannot compete with GPUs and Nvidia’s CUDA software platform on general workloads, which excels at running every model, every framework and every new architecture.

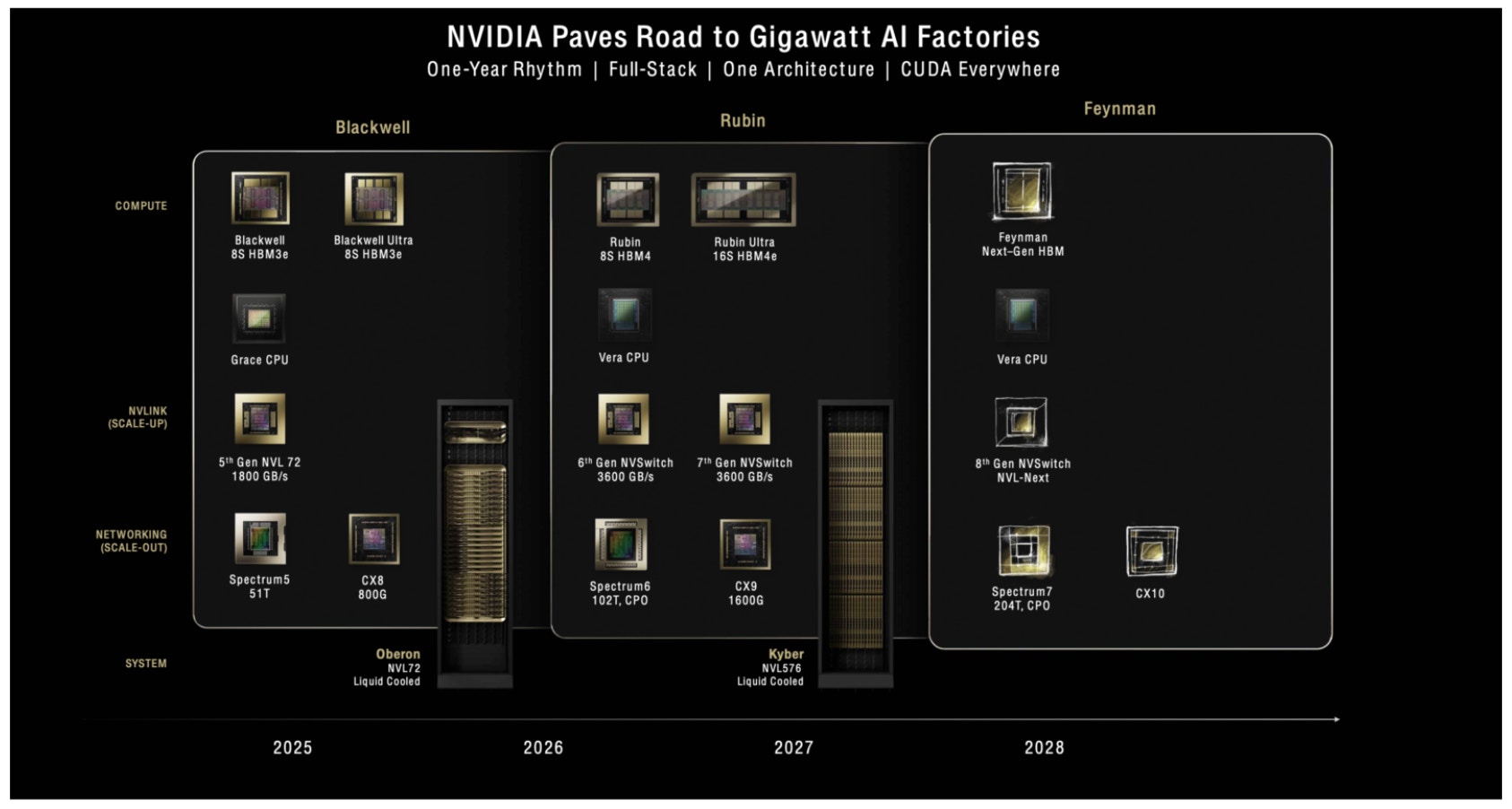

The key reason that Nvidia can reach a $20 trillion market cap by 2030 is because the company is moving its GPU generation cadence to a rapid 12-18 month cycle compared to custom silicon, which is typically on a 3-5 year cycle. Even for Nvidia, the goal of releasing a new GPU generation every year was once unthinkable. Yet this offensive measure will be transformative, turning what was once a cyclical revenue profile into a consistent and compounding growth trajectory.

Source: Nvidia GTC Conference, March 2025 Last March, Nvidia revealed their plans for a 1-year product cadence, a key element to the I/O Fund’s thesis that Nvidia can reach $20 trillion market cap by 2030.

At this point, Nvidia is competing with itself with Blackwell offering 208 billion transistors compared to Hoppers 80 billion transistors. By combining 72 GPUs, the Blackwell systems offer 30X to 40X faster inference and are up to 2.5X faster on training. The memory capacity has increased to 192GB of HBM3e for Blackwell and 288GB for Blackwell Ultra. Energy efficiency is also improved by 25X. The 30X improvement in running AI reasoning models is primarily from leveraging FP4 format and fifth-generation NVLink at rack scale level. Blackwell arrived in H1 of 2025 and Blackwell Ultra is shipping now in H2 2025.

Vera Rubin increases the number of GPUs to 144, up from 72 GPUs, for 3.3X higher performance. Vera Rubin doubles the FP4 performance from 20 petaflops to 50 petaflops. The new architecture will offer HBM4 memory and sixth-generation NVLink. Rubin Ultra takes rack-scale to a new level with 576 GPUs compared to Rubin’s 144, with more details to be released in the coming months. Vera Rubin is expected to arrive in H2 2026 with Rubin Ultra in H2 2027.

From there, Feynman is expected to bring to market Gigawatt AI factories, which would be up about 8X from today’s peak cluster size of 150 MW (the largest cluster right now is Colossus at 150MW with plans to expand to 300MW soon). Feynman is expected to arrive in 2028.

5X Hopper: Jensen Huang Reveals $500 Billion Blackwell and Rubin Revenue Visibility

Nvidia laid out an eye-opening stat at the company’s GTC October conference, with CEO Jensen Huang revealing the company has visibility into an astonishing $500 billion in cumulative Blackwell and Rubin revenue through the end of 2026. This is ~5X the lifetime revenue of its Hopper GPUs from 2023 through 2025 which stood at $100 billion.

Huang’s projection calls for 20 million GPU shipments, with 30% of that, or 6 million, having already been shipped; however, considering both generations have two GPUs per chip, in reality, this corresponds to 10 million chip shipments with 3 million already shipped. Huang’s forecast also excludes China but is expected to include attached networking equipment such as Nvidia’s InfiniBand and NVLink.

Reading between the lines on Huang’s comments suggests strong upside to Nvidia’s data center revenue through 2026. Over the prior three quarters heading into fiscal Q3’s report, Blackwell revenue has totaled approximately $63 billion. Including Networking over that time frame, total revenue would rise to $78 billion, still a fraction of the total overall opportunity management is projecting. Thus, if we assume that Blackwell and Rubin ramp over the next five quarters, fiscal 2027 data center revenue could be nearly $320 billion, versus estimates for around $270 billion.

This forecast is supported by the accelerated progression in GPU cluster sizes, scaling quickly from 10K clusters just two years ago to hundreds of thousands over the next few years. The first 10K Hopper GPU clusters came online in 2023 and 2024, before scaling 10X to 100K clusters by year-end 2024. Blackwell is picking up where Hopper left off, with clusters expanding from 100K to the hundreds of thousands through 2026 and 2027, such as for Microsoft’s new Fairwater data centers and xAI’s Colossus 2. This scale out of 8-10X growth to reach 1 million GPU clusters over the next few years underpins millions of GPU shipments over the coming quarters.

Consensus Estimates Still Below Nvidia's $500B Target for FY26/27

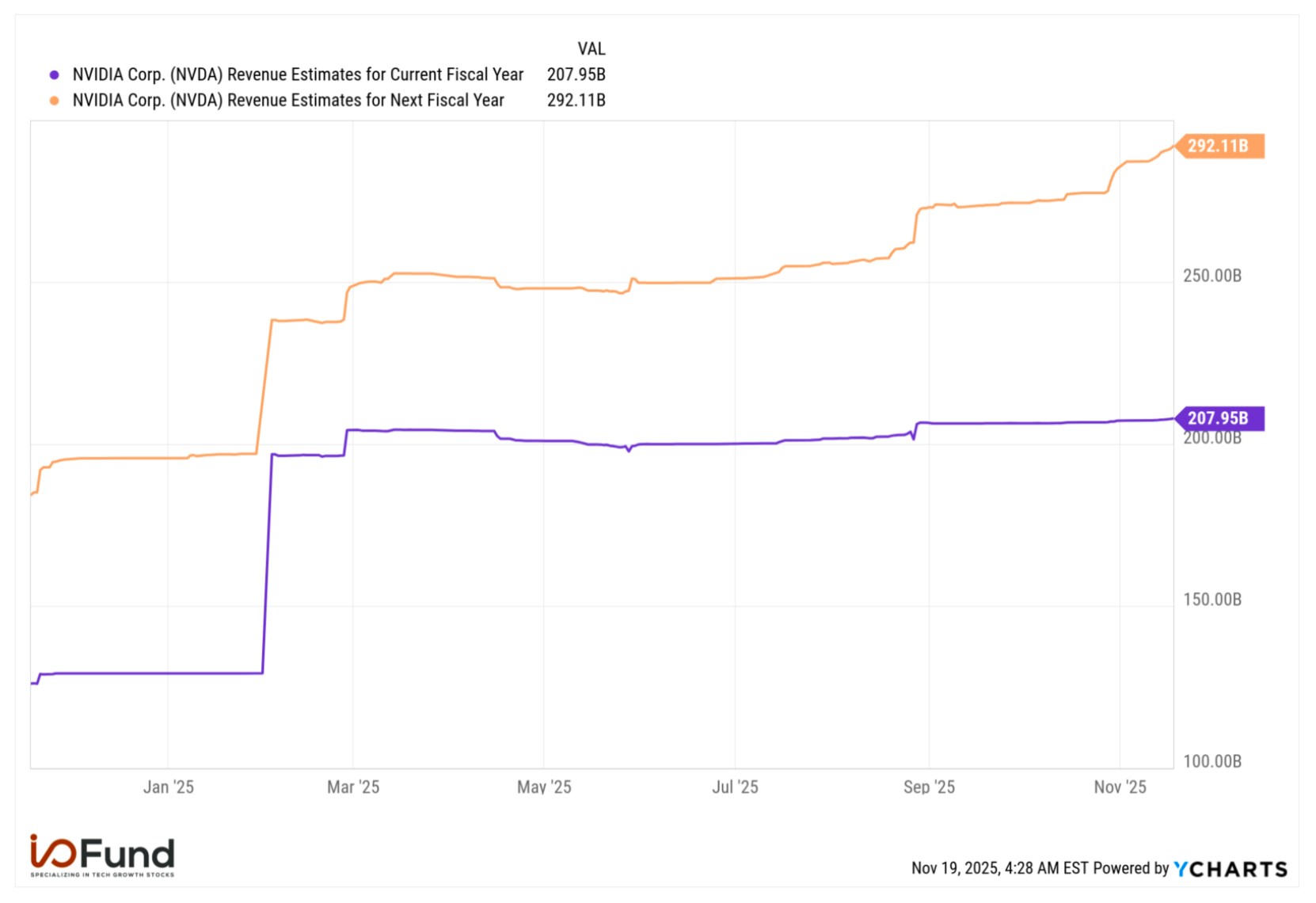

Even with the commentary for half a trillion in revenue potential for Blackwell and Rubin GPUs, consensus estimates for fiscal 2026 and 2027 still remain below $500 billion combined. This also comes despite numerous analysts pointing out that Street estimates are too low and citing substantial upside potential for data center revenue.

Source: YCharts

Current consensus estimates point to $207.6 billion in revenue in fiscal 2026, before rising to $290.5 billion in fiscal 2027, with next year seeing only a $13 billion (5%) upward revision following the $500 billion forecast. It’s important to note that some of fiscal 2026’s revenue came from the Hopper generation, which contributed ~30% of Compute revenue in fiscal Q1, or more than $10 billion.

However, analysts from Cantor, UBS, Melius and others believe estimates are too low moving through calendar 2026. New Street says the $500 billion forecast “implies a nearly doubling of Nvidia's data center revenue in 2026,” while Wolfe Research estimated that data center revenue "could be $60 billion over prior calendar 2026 estimates.”

This suggests that the Street remains cautious about this order visibility materializing in full, as current consensus estimates would project data center revenue of ~$445 billion assuming ~90% share of total revenue.

AI Buildout Accelerates: Big Tech Capex Headed for $405 Billion

Big Tech Capex grew by 75% YoY and 19% sequentially to $113.4 billion in Q3. In fact, capital spending for the AI buildout has risen 44.6% from our initial estimates. A substantial jump considering the scale already measured in hundreds of billions. This time last year, the expectations were $280 billion in Big Tech capex.

Morgan Stanley later forecast $300 billion in Big Tech capex for 2025. Capex estimates stood at $365 billion heading into Q3, and now we believe 2025 capex is on track to surpass $405 billion, representing YoY growth of 62%. This spells good things for the I/O Fund’s projected 36% CAGR for Nvidia’s data center to materialize.

Overall, analysts have clearly underestimated the growth in capex and future AI opportunities. This is also evident when AMD’s CEO Lisa Su recently increased the company’s AI total addressable market to $1 trillion in 2030, up from the previous forecast of $500 billion by 2028.

In terms of what the opportunity looks like moving forward, McKinsey is predicting 3.5X growth in gigawatts for AI data centers between 2025-2030. The costs associated with AI data centers range from $3 trillion to $8 trillion, or about $5.5 trillion at the midpoint. This correlates to about 3X growth if we assume the current run rate to 2030 is $1.8 trillion at the current capex of $405 billion.

UBS recently upgraded the AI capex estimates from the previous $375 billion to $423 billion for 2025. For the next year, they have increased the estimates from $500 billion to $571 billion, a solid 14% increase. By the year 2030, UBS expects overall spending to hit $1.3 trillion, implying a 25% compound annual growth rate (CAGR) over the next five years - or about 11 points lower than our estimate for 36% CAGR - although I still have five years to go for analysts to raise their estimates, which judging by what we’ve seen in capex estimates, could very well be doable.

Another point as to why AI spending estimates may be too low is they are still modest to global GDP. According to IMF estimates, the $1.3 trillion capex estimate would only account for 1% of GDP, whereas some of the previous investment booms like railroads, computers, telco, etc. – ranged from 1.5% to 4.5% of global GDP.

Nvidia’s Deals with OpenAI and Microsoft Fuel Insatiable GPU Demand

If a $20 trillion market cap sounds outlandish, consider the deals worth hundreds of billions that are pouring in. Not only does Nvidia have the $500 billion Stargate project underway for OpenAI, but the ChatGPT parent also committed to an additional $250 billion of compute from Azure as part of its for-profit restructure.

Additionally, Nvidia signed a partnership with OpenAI, which will see it deploy up to 10GW of Nvidia GPUs in data centers. Under the deal, Nvidia is investing up to $100 billion in OpenAI progressively as each GW is deployed. The first GW of GPUs under Nvidia and OpenAI’s agreement will be deployed in the second half of 2026 on Nvidia’s upcoming Vera Rubin platform. While there was no set timeline for the remaining nine GWs of chips, CEO Jensen Huang told CNBC that the entire deployment would represent around four to five million GPUs.

In terms of the total opportunity for Nvidia, Bank of America estimates this partnership could generate $300 billion to $500 billion in revenue overtime at full deployment. This aligns with expectations from other analysts that Rubin and Rubin Ultra will cost $30 to $35 billion per GW, with 10-15% increases per GW per each generation.

Microsoft also contracted approximately 200,000 GB300s from British startup Nscale in a deal said to be worth $14 billion, with the first smaller-scale deployment starting in Q1 followed by a 104,000 cluster in Q3 2026. This builds on Microsoft CEO Satya Nadella hinting last weekend that Microsoft is bringing online more than 100,000 GB300s this quarter, or approximately 1,389 NVL72 racks worth ~$4.17 billion at a $3 million estimated ASP.

Deals like these that continue to pop up across the industry hint that demand for GPUs remains insatiable to meet high demand. It also suggests current capex estimates may be too low as hyperscalers continue to pour tens of billions each quarter to data center infrastructure via whatever avenue possible.

Conclusion:

When you step back from the noise and look at the data, the path to $20 trillion is built on compounding fundamentals that are already surpassing the most aggressive forecasts from a year ago. Analysts continue to revise capex expectations higher, AI infrastructure projections have doubled, and Big Tech is racing to deploy unprecedented levels of compute.

The data center segment growing 36% CAGR is a tad ambitious, yet it does not factor in markets such as robotics, agentic systems and simulation. Also consider we are seeing 5X growth from the Hopper cycle to the Blackwell-Rubin cycle in the data center segment. At the end of 2026, we will need only 3X growth to deliver on my prediction of a $930 billion data center segment.

Today, my updated thesis is clear: Nvidia has a credible path to reach a $20 trillion market cap by 2030 with an aggressive product road map for Blackwell, Rubin, Rubin Ultra and eventually Feynman’s gigawatt-scale AI factories. Just as with my earlier calls on Nvidia’s stock, the data increasingly supports an outcome that was once considered impossible.

As AI accelerates into the largest technology buildout of our lifetime, we believe Nvidia remains one of the strongest beneficiaries. Our portfolio is also positioned with many of Nvidia’s lesser-known AI networking suppliers and AI energy stocks. To view the I/O Fund portfolio plus my 43-page Top 15 AI Stocks list, sign up below.

For Black Friday, we’re offering one of our biggest sales of the year — $250 off our Advanced Market Signals flagship tier. Sign up here.

Our cumulative return of 210% would place us as #2 if we were a hedge fund and #5 if we were an ETF. Our entries and exit are sent in real-time including one entry as low as $3.15 on Nvidia in 2018 and 9 alerts sent under $20 in 2021 - 2022. This year, we have an AI energy position up over 500% and others up over 100% in AI energy and AI networking. Learn more here.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund own shares in NVDA at the time of writing and may own stocks pictured in the charts.

Recommended Reading:

- Big Tech’s $405B Bet: Why AI Stocks Are Set Up for a Strong 2026

- Market Cycles, Not Headlines: What History Says About the 2025 Rally and What Comes Next

- Decoding the S&P 500: When Human Sentiment Meets Artificial Intelligence

- TSM Stock and the AI Bubble: 40%+ AI Accelerator Growth Fuels the Valuation Debate

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per