Updated Nvidia Stock Price Target - AI “Bubble” Narrative Ignores Re-Acceleration in Big Tech Capex

September 18, 2025

Beth Kindig

Lead Tech Analyst

Nvidia stock faced a rare price target cut last week following a weaker-than-expected Q2 and heightened competition from Broadcom. The company has faced numerous headwinds from China and also production delays in their current generation of GPUs.

As someone who has tracked Nvidia’s cyclical downturns closely since 2018,the culmination of negative narratives in-between GPU generations is eerily familiar. Needless to say, in the past, Nvidia’s cyclical bottoms were buying opportunities where getting the stock lower helped to increase stock returns in the span of a few months.

Investors who bought Nvidia stock at the October 2022 bottom have seen more than 10X returns in just three years, underscoring Nvidia’s explosive AI-driven growth. Source: YCharts

Nvidia’s softer price action this past month is partly due to Broadcom hinting they will see strong AI growth next year. There were some important numbers in the report that we covered for our premium members to help gauge just how much growth Broadcom could see.

Although I’ve been quite vocal around Broadcom’s importance as a contender on AI accelerators, the chances are low that custom silicon can compete with the powerful and versatile NVL72 systems that Nvidia is shipping now. There will certainly be a time when custom silicon helps to drive down costs for Big Tech, especially around inference. However, it is too early for this to be a serious threat to Nvidia given one of their most important GPU generations to date is (finally) shipping in volume.

There are other clues that Nvidia’s reign will continue. Prior to the earnings report, I discussed why Big Tech is providing an important green light, stating the capex numbers we saw as recently as two weeks ago are “beautifully packaged” to help guide AI investors on where Nvidia’s stock can go next.

Nvidia $NVDA is at roughly a $160B run rate for the data center.

— Beth Kindig (@Beth_Kindig) August 27, 2025

In an interview with Caroline Hyde from @technology, I discuss the path to a $300B run rate plus the constraints that Nvidia and the broader AI market face as we approach future generations of GPUs.… pic.twitter.com/CzzYvKpC7x

In the analysis below, my firm crunched the hard data on Q2 capex numbers and what is coming down the pipe for Q3. If you are an AI investor like we are, this is an analysis you will not want to miss as the numbers below help to dictate how much room is left in many AI stocks.

As a final highlight, we are rolling out a brand-new buy plan for Nvidia stock – which is highly dependent on capex growth. When it comes to Nvidia buy plans, many of you are aware the I/O Fund has a strong track record — from our $3.15 entry in 2018, to buying at $10 in October 2022 on the very day the stock bottomed before the AI surge, with real-time trade alerts sent to Members.

More recently, we stood apart by urging caution just before the DeepSeek news, outlining a “wait to buy” strategy in the analysis “Where I Plan to Buy Nvidia Stock Next” as we anticipated Nvidia could dip below $100. That call paid off, allowing us to secure shares at $95 and $88, again with real-time alerts to Members.

Below, we present a new buy plan for you below plus a few reasons why I am (once again) saying the Street has Nvidia all wrong.

Looking back, Q1 Capex was Weak with 2% QoQ Decline

Before deep diving into Q2’25 growth, let’s contextualize Q1 and why the AI trade was soft earlier this year beyond tariff impacts. Total Capex of $77.3 billion, was up 62.4% YoY from $47.6 billion in Q1’24 but down (2.0%) QoQ when compared to $78.9 billion in Q4’24.

As seen below, this was the first quarterly decline in capex in 8 quarters, likely triggering some doubts regarding the durability of spend for short-sighted investors.

In Q1, Big Tech reported a rare 2% decline in capex, pressuring Nvidia’s stock earlier in the year as AI infrastructure spending slowed.

It is important to note that this weakness was broad-based, with three of four hyperscalers declining, signaling a timing issue rather than a fundamental demand problem. During earnings calls, management teams largely cited timing issues and power constraints as the main contributors to the QoQ decline — specifically grid hookups, permitting delays, and PPA negotiations. Needless to say, investors were especially focused on these capex numbers coming into Q2.

AI Stocks, like Nvidia, set to benefit from Q2 cap-ex acceleration

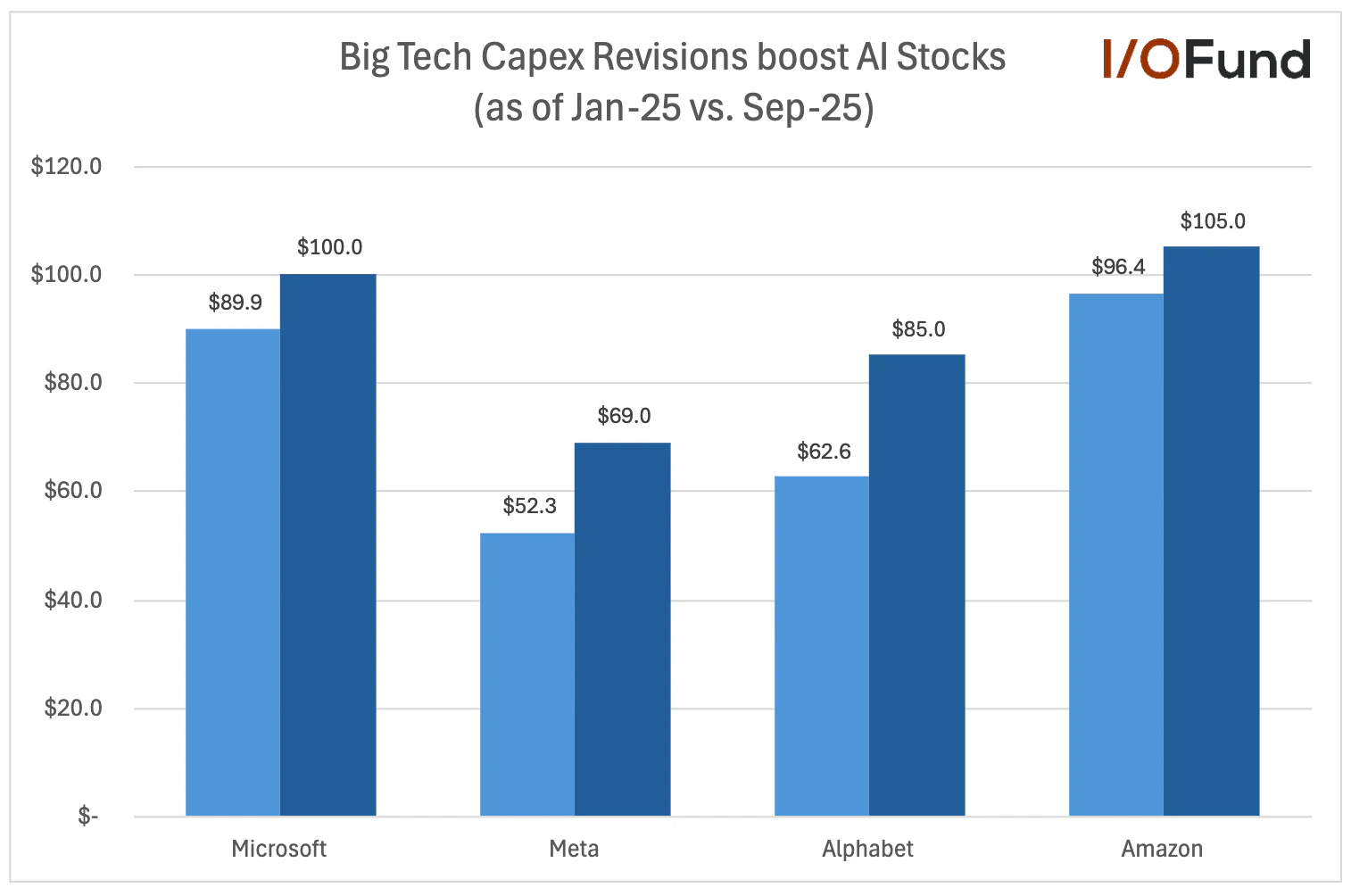

In the table below, Big Tech Capex is surging QoQ in Q2 with Alphabet, Amazon, and Meta all spending 24% and up to 30% more QoQ on AI infrastructure. This far exceeded previous estimates which led to further upward revisions of capex guidance for the full year.

In Q2 2025, Big Tech companies — Microsoft, Meta, Alphabet, and Amazon — accelerated capex spending by 24% QoQ to $95B, raising full-year guidance to $359B. This surge in cloud and AI infrastructure investment is a strong tailwind for AI stocks, including Nvidia.

Q2 hyperscaler capex hit a combined $95.0 billion (+23% QoQ, +63% YoY) with multiple raises and Q3 run-rate signals. Street’s FY25 roll-ups moved from ~$300B to ~$359B (+20% upward revision) and still look light if energization stays on track. These dollars are concentrating in servers / accelerators, DC shells, interconnects, cooling, and networking – setting up a sustained spend momentum into 2026.

The graph below shows a sharp uptick specifically in Q2 2025 compared to the previous quarter, helping to illustrate why AI spend is not slowing down (quite the opposite). This had an important readthrough for Nvidia and other hardware players like Broadcom.

Big Tech capex growth is fueling AI infrastructure demand and supports a higher move in Nvidia’s stock.

Below, we take a look at each Big Tech company and what they are individually communicating about the year ahead for AI stocks.

Microsoft Guides Capex 27% Higher than Street Estimates

Q2 capex totaled $24.2 billion (+13% QoQ, +27% YoY), reversing Q1’s brief dip and setting a quarterly record. MSFT confirmed this was driven by AI data center build-outs, with a heavy mix of short-lived IT gear (GPUs, servers, networking) versus real estate.

CFO Amy Hood stated in the earnings call that capital expenditures were expected to exceed $30 billion in Q3, driven by “continued strong demand signals”, specifically referencing AI-related services and Azure.

Azure revenue was reported as a standalone metric for the first time in its latest quarterly report, being stripped out of “Azure and Other Services.” The company stated Azure saw $75 billion in revenue or growth of 34%. For comp purposes, the original segment grew 39% up from 33% / 35% on CC basis last quarter.

According to the CEO, Microsoft is ahead of other hyperscalers in speed of data center buildouts: “We continue to lead the AI infrastructure wave and took share every quarter this year. We opened new DCs across 6 continents and now have over 400 data centers across 70 regions, more than any other cloud provider. There is a lot of talk in the industry about building the first gigawatt and multi-gigawatt data centers. We stood up more than 2 gigawatts of new capacity over the past 12 months alone. And we continue to scale our own data center capacity faster than any other competitor.”

The heightened guide was notably higher than both analysts’ expectations at the time and higher than Microsoft’s own Q2 level (~$22.6 billion), marking a sharp step-up for the quarter. FY25 total capex is now expected to reach ~$80 billion, well ahead of original Street expectations of ~$63 billion going into the year.

Alphabet Q2 is Highest Quarterly Capex Spend Ever

Q2 capex came in at $22.4 billion, up 30% QoQ & 69% YoY, marking its highest quarterly spend ever. This quarter made a significant step-up as Google accelerated TPU vNext production and bulk GPU orders alongside new data center builds.

Alphabet raised FY25 capex guide by ~$10 billion, now targeting ~$85 billion versus ~$75 billion previously. Management guided continued sequential growth in Q3, though not the same YoY % step-up seen from ’23 to ’24. Investment consists of Custom TPUs, Nvidia GPUs and Data center shells and land acquisition. Cloud remains a bright spot, with revenue growth up +35% YoY in Q2.

This elevated spend is highly correlated with Google’s new chip, Ironwood, considered its largest, fastest, and most power efficient TPU yet – designed for both AI training and inference workloads. Although Management has not provided any direct figures around spend, they noted that in April 2025 that Ironwood “ships sometime later this year. We reckon it will be towards the end of the year, perhaps in the fall and maybe even in the early winter depending on how tough manufacturing ramp is.”

This move signals Google’s ambition to reduce dependence on Nvidia, win AI cloud workloads, and monetize inference at hyperscale. Alphabet’s AI growth engine is monetizing faster than expected, validating its aggressive hardware pipeline.

Amazon Plays Catch-Up with 29% QoQ Capex Growth

Q2 capex totaled $31.4 billion, up 29% QoQ and 63% YoY, reflecting a strong ramp in AWS capacity buildouts. CEO Andy Jassy reiterated that AWS demand outstrips supply, with Q2 spend focused on GPU clusters and Trainium/Inferentia ASIC deployments.

Amazon is now signaling >$118 billion for FY25 capex vs ~$100 billion prior. Management expects Q3 capex to stay near Q2 run rate as new data centers energize and custom silicon ramps. Capex is split between Nvidia GPUs (~196K Hoppers deployed in 2024, growing further in 2025) and Next-gen Trainium 3 clusters. This capex spend is necessary to accelerate growth for AWS to compete in the marketplace, as Azure is currently growing twice as fast and gaining market share.

AWS remains the core profit driver, with >30% OP income growth for five straight quarters. Market analysts see potential for AWS re-acceleration as Morgan Stanley analysts noted that “Amazon Web Services could experience growth above 20% in 2026 as the company expands capacity to meet increasing demand”. The bank’s analysts now have “more conviction that AWS growth has the potential to accelerate to 20%+ in ’26’” which would be “ahead of our base model and key driver of AMZN’s multiple,” with a base-case valuation of $300 per share and a bull-case scenario of $350.”

While extremely optimistic on AWS, Morgan Stanley did note that that the company was continuing to operate among “capacity constraints (data center builds, delivery of chips, racks, cables, power, etc.), which our new analysis suggests AWS is working through… which we view is a positive signal of faster AWS revenue growth ahead.”

Meta Capex up 100% YoY

Q2 capex reached $17.0 billion, up 24% QoQ & 100% YoY, making it Meta’s largest quarterly spend ever. Sequential growth was driven by server deployments, with data centers and networking also stepping up. Meta tightened FY25 capex guide to $66–72B billion vs $64–72 billion prior. Management emphasized “significant growth” in 2H25, led by servers for AI training/inference and core product refresh cycles. Servers remain the largest driver and largest portion of spend.

In its latest quarter, Management stated that while the “infrastructure planning process remains highly dynamic, we currently expect another year of similarly significant CapEx dollar growth in 2026 as we continue aggressively pursuing opportunities to bring additional capacity online to meet the needs of our AI efforts and business operations.”

Meta’s rapid deployment of custom MTIA accelerators and GPUs positions it as a top-3 AI infrastructure buyer. AI-driven ad optimizations have boosted pricing and are offsetting slowing impression growth, adding incremental ROI to Meta’s infrastructure spend.

FY Capex Guidance: What These Guides Imply for Q3 & Q4

On the topic of full year guidance, all of these firms have significantly increased the fiscal -year 2025 capitalization budgets, largely due to AI, data center buildouts, and cloud infrastructure. As seen below, coming into FY25, Big Tech was expected to spend $300 billion in capex. Following Q1 & Q2 earnings announcements, these estimates have now shifted to $359 billion.

Alphabet raised 2025 capex guidance to $85 billion, Amazon is projected to exceed $100 billion with analysts estimating $117 billion, Microsoft plans $80 billion in 2025 capex, while Meta narrowed its guidance to a range of $66–72 billion.

Of the Big Tech players, only Microsoft is indicating that growth could moderate:

- Microsoft provided commentary around its capex spend, noting that elevated capex in the first half of its fiscal year (which includes Q3 of calendar year) is due to large finance lease site deliveries and datacenter ramp-ups. This indicates there may be some moderation in H2 growth driven by a softer Q4 figure.

- Meta has continued to raise full year guidance which indicates spend remains elevated, with Ad revenue seasonality and infrastructure ramp-ups likely pushing strong spending into H2.

- Amazon indicated that quarterly capex will “mirror second-quarter spending” so the expectation there is a consistent ~$31 billion spend each quarter, in line with Q2.

- Alphabet will likely distribute spending evenly across H2 to meet its FY capex guide, with potential upside in cloud infrastructure should construction projects advance in Q2.

As shown in the table above, Big Tech capex spending typically skews toward the second half (H2) of the year, supporting stronger growth for AI stocks.

In FY23, H1 represented roughly 45% of total spend while H2 accounted for ~55%. Similar trends exist as we move forward to FY24, as H1 spend accounted for roughly 43% of annual spend while H2 reflected ~57% spend.

If we assume that budgeting systems remain consistent and that H1’25 spend remains within that 43-45% band, that would imply that H2 capex spend of ~$218 billion and full year spend of ~$390 billion, well above current estimates of $359 billion.

AI bulls will point towards this calendar spend cadence as continued fuel for potential upside against current guidance.

What Big Tech Capex Means for Nvidia’s Stock

Nvidia’s Q2 results reported a decline of (1%) for the Compute segment. This alone should have tanked the stock. Instead, we saw a mild reaction because the forward-looking guidance for the Q3 quarter was quite strong. The ramp from Big Tech capex helps to support Nvidia’s strong Q3 guide. That part is key – that Big Tech and Nvidia remain in lockstep, as they have been since the start of the AI boom.

Sign up for free below to find out the following information:

- My prediction on when Nvidia will reach a $10 trillion market cap

- Why a semiconductor trough can often be the best time to buy

- The I/O Fund’s updated buy plan. We nailed Nvidia buys at $3.15 in 2018, $10 in 2022, and more recently at $95 and $88 after calling for patience ahead of the DeepSeek news. Now we’re rolling out a new buy plan — access for free below.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per