Oracle Soars After Earnings – Is ORCL Stock Still a Buy?

September 11, 2025

Beth Kindig

Lead Tech Analyst

This quarter was less about the headline P&L figures and more about a narrative shift: Oracle’s stockis being re-rated by the market as a hyperscaler and AI infrastructure play, not a slow-growth enterprise software company. The 36% gap reflects a structural repricing based on unprecedented backlog visibility and OCI’s growth trajectory.

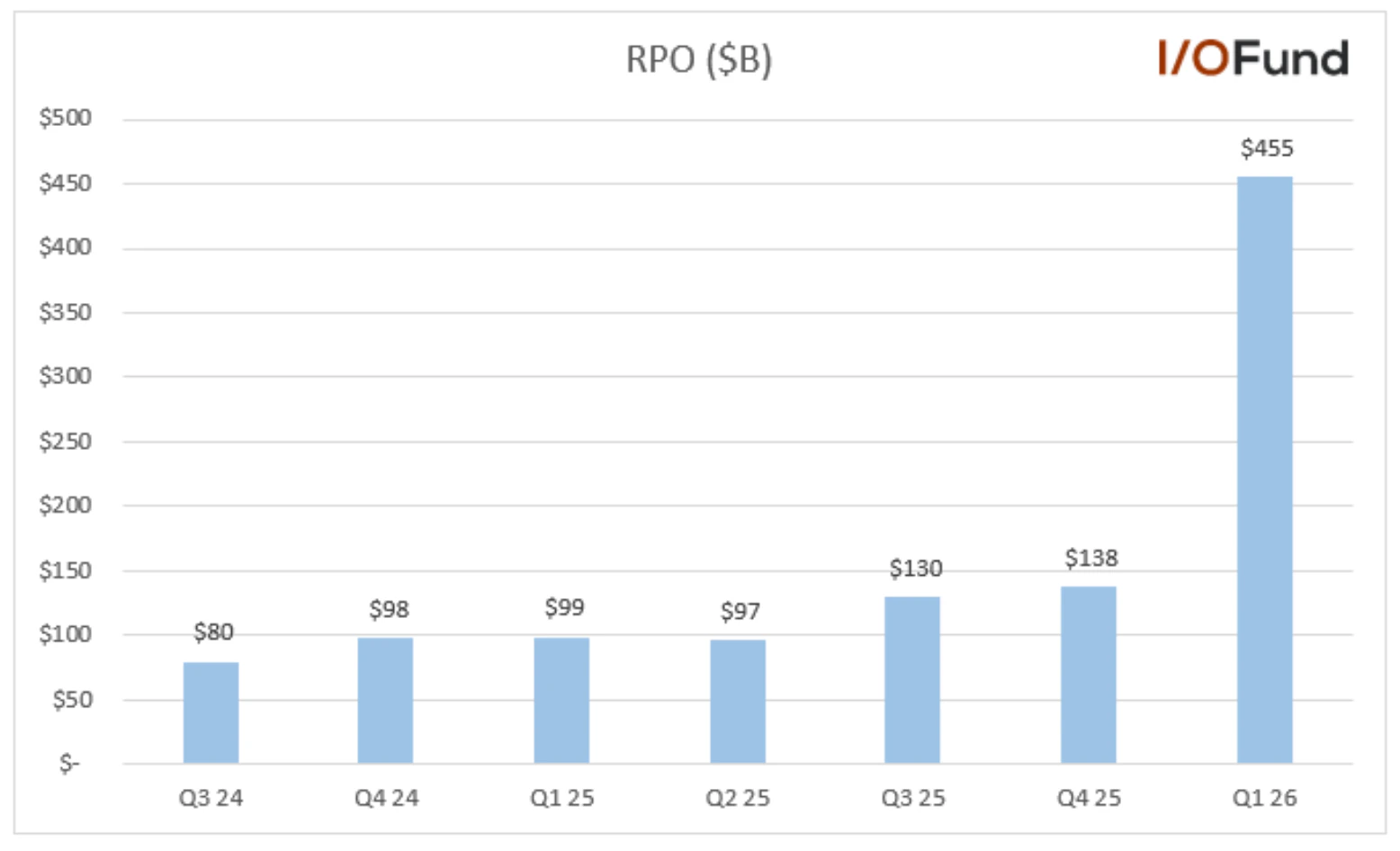

The market is clearly excited about this report, and for good reason. Remaining performance obligations (RPO) grew 359% YoY with cloud RPO growing “nearly 500%” on top of 83% growth last year. This compares to RPO growth of 41% YoY last quarter and cloud RPO growth of 83% last year. The RPO growth was strong enough to negate the miss Oracle reported in the current quarter.

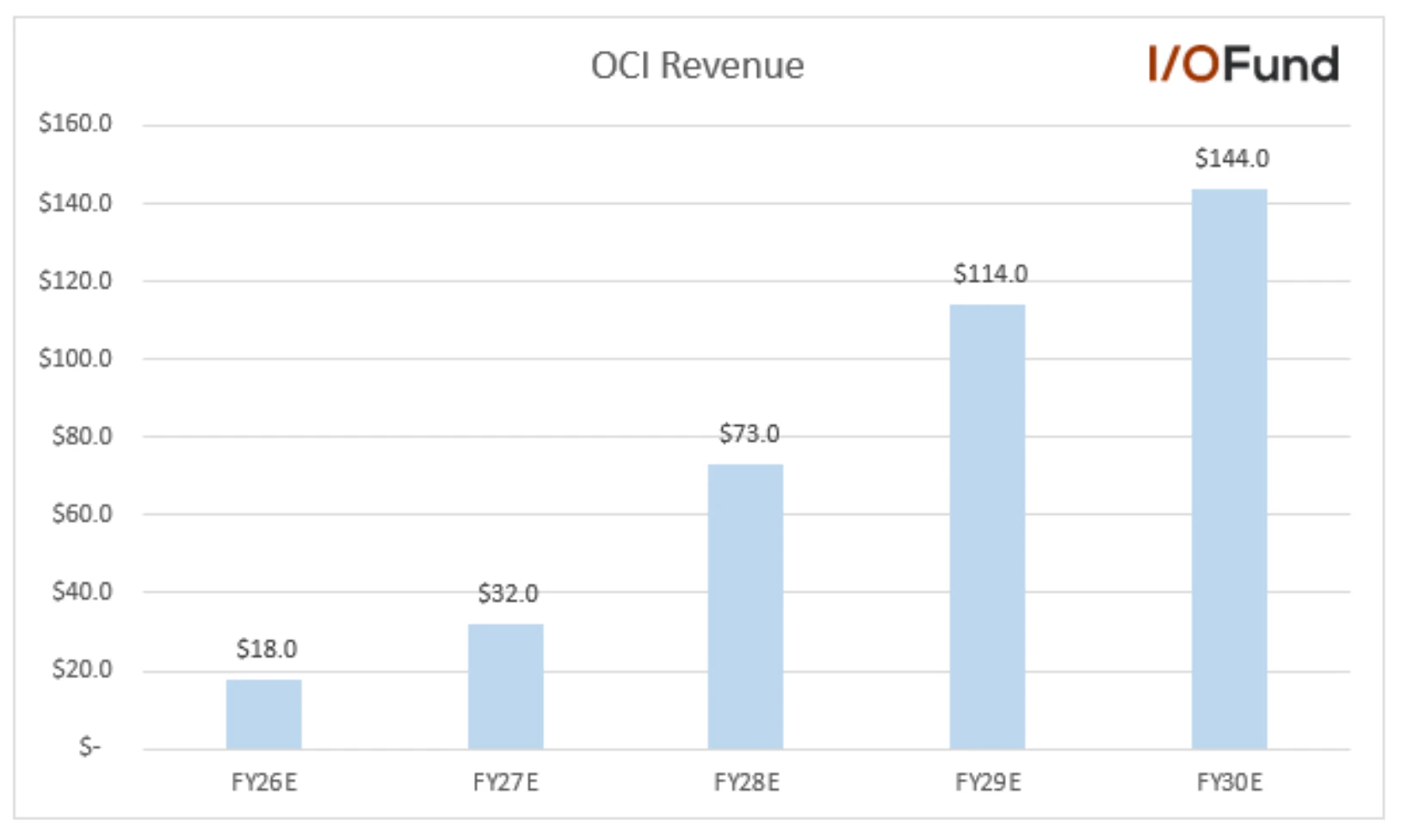

Another key reason that Oracle’s stock is exploding higher despite a lagging fiscal Q1, is that Oracle Cloud Infrastructure (OCI) was forecast to “grow 77% to $18 billion this fiscal year and then increase to $32 billion, $73 billion, $114 billion and $144 billion over the following 4 years.” You can think of this as an acceleration from roughly 50% growth on IaaS in recent quarters to up to 128% growth in future years, specifically from the $32B to $73B in the medium-term of two years out. Also, consider that Azure is at $75 billion, which means Oracle and Microsoft will likely be on par with each other over a four-year period for their infrastructure segments.

Given this, there’s no denying that Oracle reported impressive results, yet can the stock continue its run – or has the easy money been made? Below, we look more closely at Oracle’s report plus offer a buy plan that discusses how the I/O Fund – a leading AI tech portfolio - is approaching this stock.

RPO Surges to 359% YoY Growth, up from 83% Last Quarter

Remaining Performance Obligations (RPO) exploded to $455 billion, up 359% YoY. Management also guided that it could exceed $500 billion in the near term with additional multi-billion-dollar contracts, stating: “Over the next few months, We expect to sign-up several additional multi-billion-dollar customers and RPO is likely to exceed half-a-trillion dollars.” This backlog provides unprecedented revenue visibility, locking in future OCI and SaaS growth.

Oracle reported surging RPO, causing the stock to go up 36% from the earnings report.

Oracle Cloud Infrastructure (OCI) Could Surpass the Big 3 with 77% Growth

OCI (IaaS) revenue grew 55% YoY to $3.3 billion, faster than hyperscaler peers. We had pointed out in the analysis “Can Oracle Become the Next $1 Trillion AI Stock” that Oracle was quietly sneaking up on AWS, Azure and Google Cloud with a higher growth rate, stating:

“Though Oracle is growing off a much smaller cloud base than say Azure, robust IaaS momentum could drive its Cloud growth at a much faster rate than the Big 3 – defined as Microsoft, Amazon, and Alphabet -- over the next few years.

As stated above, consensus currently models in $46 billion in IaaS revenue in FY28. For the IaaS segment to increase 4.5x from FY25’s $10.2 billion in revenue, this requires growth at a 65.2% CAGR, or a slight deceleration from >70% YoY in FY26 to >60% YoY in both FY27 and FY28.

This rapid IaaS growth could fuel a 40% CAGR for Oracle’s total Cloud growth by FY28, taking its Cloud segment from $24.4 billion to $66 billion. This 40% CAGR will far outpace AWS’ growth in the high-teens, and Google Cloud and Azure in the high-20% to low-30% range.”

The earnings report is especially groundbreaking as Oracle is now forecasting an even higher number than our previous models had indicated. Management raised its guidance to +77% growth in FY26 to $18B, with a clear multi-year ramp to $144 billion within five years.

Our firm had begun to form a picture that Oracle could become more attractive than the Big 3 based on previous estimates of $46 billion in FY2028. As of last night, these estimates are now at $73 billion – suggesting Oracle is becoming a force to contend with.

Oracle’s infrastructure-as-a-service segment (IaaS) is growing faster than the Big 3, putting Oracle’s revenue on a path to contend with traditional hyperscalers.

MultiCloud DB up 1,529%YoY

Over the past 1-2 years, Oracle has been working with AWS, Azure and Google Cloud to offer database collocation, running Exadata and Oracle Autonomous Database within their cloud infrastructure. This allows enterprises to leverage Oracle’s database platforms across a multi-cloud environment without major migrations and lower data egress costs This led to multicloud database revenue with Amazon, Google, and Microsoft surging 1,529% YoY.

Oracle discussed ways that multicloud will continue to grow, citing that multicloud will continue to grow from 37 data centers to a total of 71 over the next several years. These data centers host Oracle’s databases that are embedded into the Big 3 with low latency.

Oracle’s Fiscal Q1 Earnings Results

Oracle delivered Q1 revenue of $14.9 billion, growing 12% YoY but slipping 6% sequentially, coming in just shy of the Street’s $15.0 billion estimate. While the headline miss and QoQ contraction might have raised eyebrows in another context, management quickly shifted the focus forward, guiding Q2 revenue growth of 12-14% YoY – an outlook that suggests a rebound and signals confidence that momentum will accelerate from Q1 levels.

Segment Level Results: All Eyes on Cloud

Diving deeper, Oracle’s segment level results highlight a company amid a decisive mix shift. Cloud is the clear growth engine, with revenue climbing to $7.2 billion, up a robust 28% YoY and 7.3% sequentially from $6.7 billion in Q4. Cloud now represents 48% of total revenue, a sharp step up from 42% a year ago – underscoring the Company accelerating mix shift toward next-gen infrastructure and applications. Within the segment, Cloud Infrastructure (IaaS) stood out with $3.4 billion in revenue (+12% QoQ), sustaining hyperscaler-like momentum, while Cloud Applications (SaaS) delivered a steady $3.8 billion (+4% QoQ), anchored by Fusion ERP and NetSuite growth. Together, these results reinforce that Oracle’s transformation is no longer aspiration – the company is increasingly defined by Cloud, not legacy software.

Oracle’s Software revenue came in at $5.7 billion in Q1’26, essentially flat YoY but sharply lower sequentially, making it the primary drag on total revenue this quarter. The decline underscores the continued erosion in legacy licensing which remains a structural headwind. While maintenance and support revenues provide a degree of stability, the segment is steadily losing relevance in the growth narrative. Investors should expect Software to remain a transition burden until Oracle’s cloud scale-up fully eclipses the legacy base.

Oracle’s Hardware revenue was $670 million in Q1’26, essentially flat YoY (+2%) but down 21% sequentially from Q4. While the sharp QoQ decline is a visible drag on top-line optics, Hardware now represents less than 5% of total revenue and continues to shrink in strategic importance. Management has long signaled that the mix shift away from on-prem hardware is deliberate, freeing up resources to scale higher-growth cloud infrastructure. For investors, Hardware is best viewed as a legacy headwind that will gradually fade from relevance, with little bearing on the core thesis around OCI and Saas growth.

Oracle’s Services Revenue reached $1.35 billion in Q1’26, up 7% YoY from $1.27 billion but essentially flat sequentially. This segment provides steady, recurring revenue, anchored by consulting, support, and implementation work tied to Oracle’s enterprise base. While not a growth engine, Services play an important supporting role in the broader cloud story, helping customers migrate workloads and deepen adoption of Oracle’s SaaS and OCI platforms. The real value here is its stickiness – ensuring that once customers enter Oracle’s ecosystem, they are more likely to expand and consume additional cloud services over time.

EPS Split: GAAP Miss, Adjusted Beat

EPS Trends reflect a split narrative, as GAAP EPS missed while non-GAAP EPS beat. Both GAAP and adjusted EPS fell QoQ as the Company leaned heavily into investment mode. Adjusted EPS still showed positive YoY growth, flexing underlying profitability despite the cloud buildout. The market appears to have looked past the GAAP miss because adjusted EPS and cloud momentum underscore the long-term growth story.

- GAAP EPS of $1.01, down 15% QoQ from $1.19 in Q4’25 and flat YoY vs. $1.03 in Q1’FY25. This figure was also lower than the analyst estimates of $1.04. This decline was largely driven by restructuring charges, higher interest expense, and heavy investment.

- Non-GAAP EPS of $1.37, up 6% YoY from $1.39 in Q1’25 but down 14% QoQ from $1.70 in Q4’25.

Liquidity Steady, Capex Heavy as Oracle funds the Cloud Buildout

Oracle’s balance sheet and cash flow metrics show a deliberate tilt toward aggressive investment as the company is pulling every lever (e.g. heavy capex, payables management, heavy debt burden, etc.) in the near term to build datacenter capacity and capture OCI demand. Operating Cash flow is growing and outpacing revenue growth slightly, signaling operational effectiveness and economies of scale. Liquidity remains adequate with cash steady at $10B and deferred revenues providing visibility, but working capital is increasingly cloud-contract driven. The tradeoff here is clear: short term FCF pain for long-term hyperscaler positioning.

Next week, we will break down how capex compares to AI revenue for the major hyperscalers plus Oracle – which stock is seeing the highest ROI? Sign up here to get this free analysis in your inbox.

How Oracle Compares to the Big 3

Oracle’s ability to drive lower latency and high performance is one of the main reasons enterprises use Oracle for AI, as it allows enterprise customers to run demanding AI workloads faster and at a lower cost.

RDMA (Remote Direct Memory Access) is helping to drive Oracle’s AI story by enabling direct memory access between servers without utilizing CPUs, resulting in low-latency, high-bandwidth performance. Bypassing the CPU greatly accelerates data transfer rates, a necessity for large AI workloads requiring massive compute.

RDMA is integral to Oracle Cloud Infrastructure as the backbone of Oracle’s Gen2 Cloud and increasingly large Superclusters for AI training and inference, allowing ultrafast, near real-time performance. Oracle says that it can offer less than 10 microseconds of latency between nodes, improving efficiency.

Oracle offers the widest range of bare metal GPU instances among major cloud providers, and scalability at any size up to 65,536 Hopper GPU clusters and 131,072 B200 GPU clusters, which are expected to come online in 2025. Oracle also offers very flexible VM instances, letting customers pay for only the capacity they need as they need it for any size workload, rather than offering fixed instance sizes.

With less overhead and fewer CPU cycles, RDMA helps Oracle offer its AI clusters at a lower cost: Oracle says it “consistently charges less than Amazon Web Services (AWS) for the equivalent compute capacity.”

Last night in the call, Oracle emphasized how cheap they are compared to the Big 3, stating: “We have gotten the entire Oracle Cloud, the whole thing, every feature, every function of the Oracle Cloud down to something we can put into a handful of racks, 3 racks, we call it Butterfly that cost $6 million. So we can give you a private version of the Oracle Cloud with every feature, every security feature, every function, everything we do for $6 million. I think the cost for the other hyperscalers is more than 100x that.”

The Importance of Vectorized Data

Oracle’s AI vector capabilities also stand out given Oracle’s database roots, offering native AI vector search capabilities with seamless integration to leading AI models from OpenAI, xAI, Meta, Cohere and more. AI vector search lets enterprises search both structured and unstructured data in a variety of manners, enabling intelligent, relevant and accurate AI responses utilizing their data. Oracle noted in Q3 that its Oracle Database 23ai can convert data into any vector format to be understood by an AI model of choice, facilitating AI training and inference on private data in Oracle’s Database.

The announcement of Oracle’s AI database is particularly interesting in terms of the stock extending its run. As explained in the call last night, the combination of vectorizing data to where it can be understood by AI models with the ability to connect private databases to AI reasoning models will result in enterprises unlocking higher value from AI. Here is what was

said: “Then we made it very easy for our customers to directly connect all their databases, all their new Oracle AI databases and cloud storage, OCI Cloud storage to the world's most advanced AI reasoning models, ChatGPT, Gemini, Grok, Llama, all of which are uniquely available in the Oracle Cloud. After you vectorize your data and link it to an LLM, the LLM of your choice, you can then ask any question you can think of. Who's offering that to customers? We'll be the first when we deliver it and demonstrate it at AI World next month.”

After a 35% Gap Up, is ORCL Stock Still a Buy?

After a historic day in the markets with Oracle up 36% after Tuesday's print, the main question that remains is if Oracle is still a buy or has the easy money been made? Considering that RPO is up 359%, cloud RPO is up nearly 500% and multi-cloud database growth is up over 1,500% - it’s well worth the time to look at what the technicals are saying as Oracle approaches a $1 trillion market cap.

Below, we discuss:

- Is Oracle stock still a buy using technical analysis to discuss potential entry points.

- What levels to watch to confirm Oracle still has room to run ahead of a highly anticipated Oracle Cloud World next month.

- The key to Oracle’s stock expanding – which was not in the most recent earnings report, but rather, the two key items that will help drive the stock upward in 2026 and beyond.

The I/O Fund is a leading AI portfolio with 45% allocation to tech stocks going into 2023 before Wall Street caught onto the potential of AI, yet this stands at an 87% allocation to AI stocks today. With cumulative returns of 210%, we’d place #2 if we were a hedge fund and #5 if we were an ETF.

The Key to Oracle’s Stock Expanding is Two-Fold

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i