I/O Fund’s Preview of 7 Cloud Stocks for Q4 Earnings

January 28, 2022

Royston Roche

Equity Analyst

IBM released upbeat results recently as the company beat consensus analysts’ revenue estimates by $740 million and adjusted EPS by $0.06. Even though IBM is not a pure-play cloud company, it has increased its focus in the cloud segment to stay in the race. IBM’s cloud revenues increased 16% YoY in Q4 and the results brought some relief to the investors after the recent volatility in the stock market.

On the other hand, Microsoft beat analysts’ revenue estimates by 1.9% and adjusted EPS by 6.9%. Microsoft Cloud revenue grew 32% to $22.1 billion. This is a positive sign for the broader cloud market. The company’s capex has also been strong, suggesting that management believes demand is structural.

Our Cloud companies’ earnings preview includes Dynatrace, Unity Software, JFrog, DigitalOcean, UiPath, Palantir, and BigCommerce. To understand valuations across the cloud companies and how the sector is positioned moving into earnings, please reference our analysis, “I/O Fund’s Cloud Q4 2021 Earnings Overview.”

Dynatrace Inc – Earnings on February 02nd

ARR: Annualized Recurring Revenue

Source: YCharts, Earnings Reports, and I/O Fund

The company’s revenue in Q2 FY22 grew 34% YoY to $226.35 million. According to the analysts’ consensus estimates, revenue is expected to grow 28% YoY to $234.6 million in the next quarter. The management has been positive on the long-term growth prospects due to the digital transformation across industries. In the last earnings call, they mentioned that the near-term market expansion opportunities include the U.S. government's investments in cloud platforms.

Barclays analyst Raimo Lenschow has lowered the price target to $65 from $85. He has an Overweight rating. According to the analyst, the main question for software investors in 2022 is not around end demand, as there are "no issues there," but the correct valuation level for the space. "Are we going back to the long-term average, or should software bounce back to the more recent highs given the exciting structural growth profile? We are in the former camp,” says the analyst as he gets a bit cautious on the sector.

Jefferies analyst Brent Thill also lowered the price target to $60 from $75 and has kept the hold rating. He adjusted his targets across the app, infrastructure and security software spaces. “Software underperformed the S&P 500 by 15% in 2021 as overall valuations contracted 10%,” according to Thill, who thinks multiples in the space will continue to compress in 2022 as 80% of software names are expected to decelerate with "digital digestion" happening coming out of the pandemic.

Please note that the I/O Fund may or may not agree with the above financial analysts, yet we objectively report what the Street is saying. You may view our previous analysis of the company below:

3 Different Ways Companies Can Game Their Topline Growth Rates

Podcast with Motley Fool: I’m Bullish on These Trends for 2021

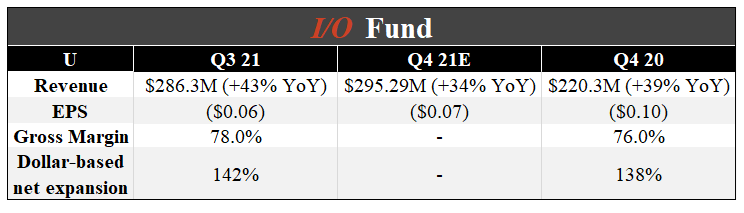

Unity Software Inc – Earnings on February 03rd

Source: YCharts, Earnings Reports, and I/O Fund

Unity’s revenue grew by 43% YoY in Q3 and is expected to grow 34% to $295.29M in the next quarter. The company recently completed the acquisition of Weta Digital. Weta is a digital visual effects company known for its work in Lord of the Rings, Avatar, and Wonder Woman. The management believes that the company’s addressable market will increase by about $10 billion from the acquisition.

Piper Sandler analyst Brent Bracelin made an interesting point that the company is an indirect beneficiary of Activision and the Microsoft deal due to its unique position as the leading 3D creator platform for gaming, movies, AR/VR, and metaverse applications. The analyst also believes that Unity can expand its footprint as a 3D creator platform in the coming year.

Stifel analyst J. Parker Lane has initiated coverage of the company with a buy rating and a price target of $190. According to the analyst, “Unity's broad set of solutions has made the company a market leader in the gaming industry and positioned its platform to address emerging use cases in other industry verticals.” Lane further adds, “Additionally, the company's continued investment in research and development, tuck-in acquisitions, and presence in gaming has helped it withstand the headwinds of IDFA and gain market share in a competitive advertising market.”

Read our previous article on the company below:

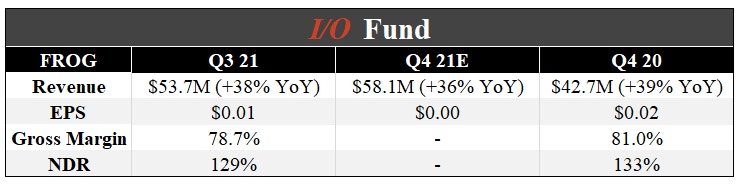

JFrog Ltd – Earnings on February 10th

Source: YCharts, Earnings Reports, and I/O Fund

The company’s revenue grew by 38% YoY in Q3 and the consensus analysts’ estimates suggest revenue to grow 36% to $58.1 million in the next quarter. The management expects revenue in the range of $57.5 million to $58.5 million and adjusted earnings per share of break-even to $0.01. For the full year, management expects revenue in the range of $205 million to $206 million, representing a growth of 36% YoY at the mid-point.

Stifel analyst Brad Reback has a buy rating and a $45 price target. He sees the company is well positioned to sustain 30%-plus revenue growth as it leverages its "unique position within the DevSecOps workflow.” He further believes that JFrog has a growing suite of solutions to help customers build, manage, distribute, and secure their respective applications more effectively and efficiently.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Needham analyst Jack Andrews has a buy rating and a $71 price target. The analyst is positive on its leverage to strong macro demand trends for DevOps tools and practices, expects its key financial metrics to inflect higher. He further believes that the company is trading at a discount to the broader software companies creating a favorable risk/reward. At the time of the writing, the company was trading at 6.0x EV/Fwd revenue multiple.

Read our previous article on the company below:

Tech Growth Earnings Review for Q3 2020 - Part 2

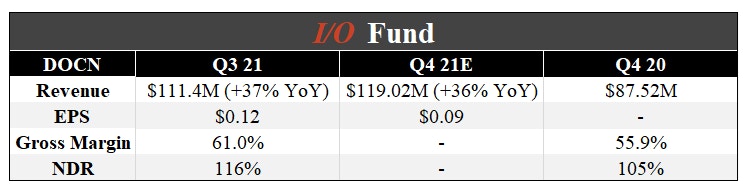

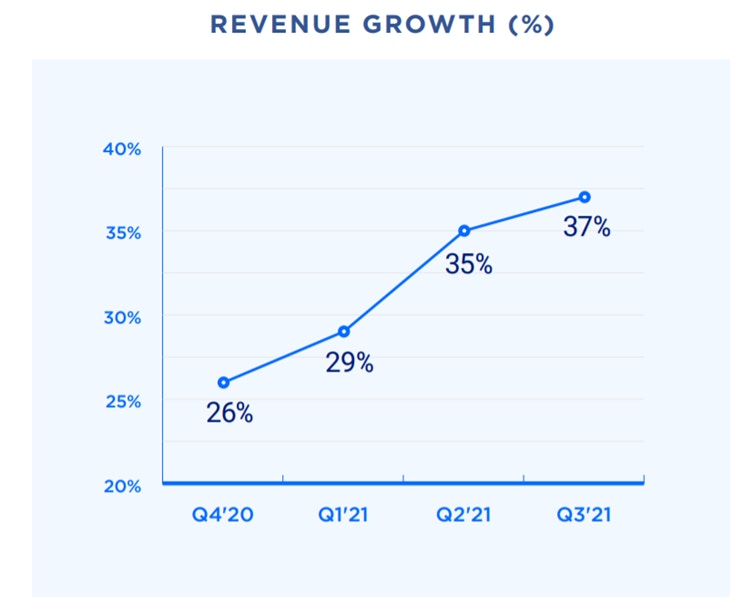

DigitalOcean Inc - Tentative Earnings date is February 15th

Source: YCharts, Earnings Reports, and I/O Fund

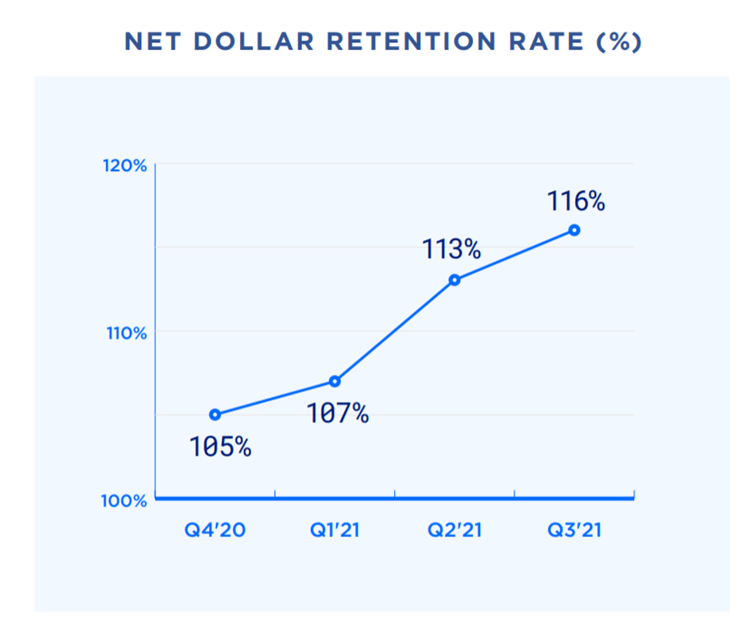

The company’s shares got listed in March 2021. The stock rose about 30% since its IPO. The consensus analysts’ estimates suggest revenue to grow 36% YoY to $119.02 million. The company’s net dollar retention rate (NDR) has shown improvement from 105% in Q4 20 to 116% in the last quarter. On the other hand, the growth rate has also shown acceleration for three consecutive quarters.

Source: Investor Presentation

Source: Investor Presentation

William Blair analyst James Breen has initiated coverage of the company with an Outperform rating. He notes, “DigitalOcean is a comprehensive cloud platform designed to simplify cloud infrastructure for developers, start-ups, and small to midsize businesses.” He is also positive on the large and growing addressable market, which is expected to reach $116 billion by 2024.

UiPath Inc – Tentative Earnings date is February 15th

Source: YCharts, Earnings Reports, and I/O Fund

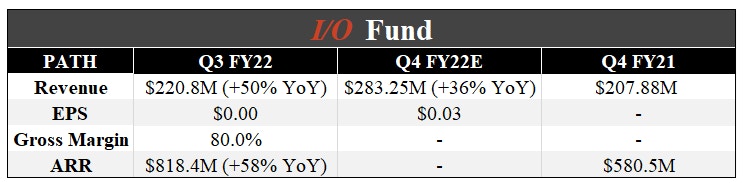

UiPath had a successful listing in April 2021. The company’s revenue grew 50% YoY in Q3 and the consensus analysts’ estimates suggest revenue to grow 36% to $283.25M. The company is betting on the robotic process automation market (RPA). According to Precedence Research, the Robotic Process Automation market is expected to reach $23.9 billion by 2030, growing at a compound annual growth rate of 28% from 2021 to 2030.

Oppenheimer analyst Brian Schwartz has upgraded the company to Outperform with a $56 price target. In his opinion, “UiPath as the RPA market leader should benefit from a strong top-line driver with good business efficiency tools demand this year. At the same time, valuation risk has lessened considerably.”

Wells Fargo analyst Michael Turrin upgraded the company to Overweight with a price target of $60. The analyst sees a "potential tailwind emerging" for the company from a tightening labor market, which he thinks could benefit automation-centric vendors.

Palantir Inc - Tentative Earnings date is February 15th

Source: YCharts, Earnings Reports, and I/O Fund

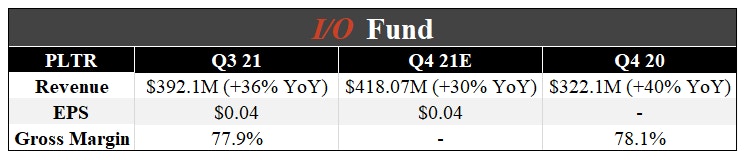

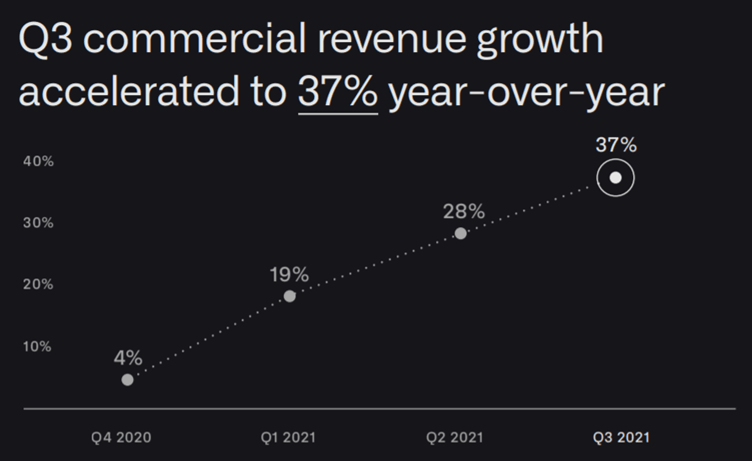

Palantir's revenue grew 36% YoY in Q3 and the consensus analysts estimate revenue to grow 30% to $418.07 million. The company's initial focus was on the government sector. The company's first platform Gotham was mainly built for government operatives in the defense and intelligence sector. The company continues to win deals from the public sector. On the other hand, the commercial revenue segment has also shown strong growth in the past few quarters.

Source: Investor Presentation

Jefferies analyst Brent Thill lowered the company’s price target to $24 from $31. He kept a Buy rating on the shares and adjusted his targets across the app, infrastructure, and security software spaces.

Deutsche Bank analyst Brad Zelnick lowered the firm's price target to $18 from $25 and kept a Hold rating on the shares. The analyst is bullish on software industry fundamentals but recommends a balanced approach with greater valuation sensitivity than in recent years.

Read our previous article on the company below:

Q1 Earnings Analysis for Etsy, Square, and Palantir

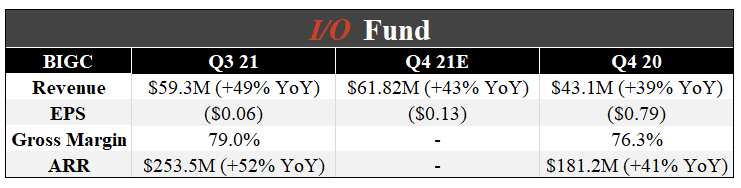

BigCommerce Inc – Tentative Earnings date is February 18th

ARR: Annual revenue run-rate

Source: YCharts, Earnings Reports, and I/O Fund

The company’s revenue grew 49% YoY to $59.3 million in Q3. It included $5.9 million from the recently acquired Feedonomics, a data feed optimization platform. The consensus analysts estimate revenue to grow 43% to $61.82 million in the next quarter. Management expects revenue in the range of $61.3 million to $61.7 million, representing a growth of 42% to 43%. The guidance includes expected Feedonomics revenue of $7.1 million to $7.3 million. For the full year, the management expects revenue in the range of $216.2 million to $216.6 million, representing a growth of about 42%.

Needham analyst Scott Berg has been positive on the recent acquisition and also has a bullish stance on the company. In his words, "We came away incrementally more confident in BIGC’s positioning in the market entering 2022 and its growth opportunity upmarket as large organizations look to re-platform from legacy on-prem solutions to a flexible, multi-tenant SaaS platform." He has a buy rating and a price target of $85.

On the other hand, a few other Wall Street analysts have lowered the price target on the company due to overall weak market sentiment. KeyBanc analyst Josh Beck lowered the price target to $40 from $75. Barclays analyst Raimo Lenschow lowered the price target to $36 from $67.

The I/O Fund is a team of analysts that share their research publicly as they build a portfolio of 20 stocks. Our team has record results for a retail Fund and we also have four-digit gains on some of our free newsletter coverage. You can learn more about our premium service by clicking here or sign up for our free newsletter here.

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

More To Explore

Newsletter

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s