June 20th is the official date of the Slack IPO, although the technical term is not an IPO but rather a DPO for Direct Public Offering. Of the cloud software companies to go public over the last few years, Slack may be Silicon Valley’s pet favorite. You can think of Slack as a cloud-based messaging and delivery hub for teams as email is ineffective for frequent communication and projects. The product is simply amazing in terms of productivity and team work flow. From a customer perspective, the cost of the paid product is offset by the time employees save by eliminating collaboration friction such as long email threads and lost files. With that said, there will be plenty of product bias on this stock from Slack power users.

Prior to the Slack IPO (or DPO to be exact), I had cautioned that cloud software is pricey right now and is breaking records from the dot-com era on price-to-sales ratios. Cloud software has carried the Nasdaq rally from December lows with some cloud software stocks seeing 100% returns compared to 13% on average from mega-cap FANG stocks over the last six months.

IPOs in the cloud software category have been especially rewarding over the last two years with PagerDuty, Okta, Twilio, Zoom and a few others trading at triple percentages from their IPO price. By simply breathing the same air as the cloud software vertical, Slack is likely to see a healthy bump when the company officially begins to trade. Notably, Class B shares are trading privately between $21 and $31.50 over the past four months with a volume weighted average of $26.38, which represents a 142% increase in value from the last private valuation of $7 billion in August of 2018.

Keep in mind, we saw the fragile ground cloud software companies are on with Zuora, which reported disappointing earnings resulting in an overnight loss of 30% in value with stock price dropping from $20 to $14 on May 31st.

Setting aside my affection for Slack (I’m logged in on two separate accounts as I write this), there are a couple of issues that require more visibility. One paramount issue is that direct listings are risky as there is no lock-up period and this didn’t go well for Spotify. The financials also reveal paid users are decreasing even though paid accounts over $100,000 are increasing. Ideally, these two metrics would both be in an uptrend. Net dollar retention rate is strong with Slack, although it has the benefit of being a fairly young company with the product having launched in 2014, and this puts the retention rate in Slack’s favor compared to prior IPOs in the same category.

You can read my analysis on Spotify here – which also had a direct listing.

1. Slack IPO Pro: The Product is Awesome

First and foremost, Slack is an exceptional product in a high-growth category and has a loyal user base. Slack currently holds the title of fastest-growing SaaS startup in history. Enough said.

2. Slack IPO Con: Direct Listing

Slack is not looking to raise money, and has chosen a direct listing as opposed to a traditional initial public offering. This means insiders will initially sell their stock and there will be no lock-up period. Eliminating the lock-up period creates even more risk than usual compared to traditional IPOs that have six-month lock-up periods.

There is quite a bit of information about Slack’s direct listing available, as well as Spotify’s direct listing, and therefore, I will not go into an exhaustive analysis of the pros and cons (there are primarily cons for public market investors). You can read my analysis on Spotify stock here when I said the stock was too high at $185 and is now priced at $127.

The issue with a direct listing for Slack is that the company should be raising money with the level of competition the company is currently facing from Microsoft globally (Microsoft is technically in the lead, according to Gartner and a few other sources). In addition, Slack has partnered with other collaborative cloud software products, such as Atlassian and Oracle, but both of these companies are much larger than Slack and are able to copy what Slack offers.

Slack has 10 million customers which is not much considering Microsoft is already in the lead and some startups may nip on their heels such as Asana. In addition, we see in the financials that Slack’s cost of user acquisition with around 50-60% of revenue spent on sales and marketing over the last two years. If this number is not improving, then Slack should be raising money to expand its reach.

3. Slack IPO Con: Net Losses Not Improving

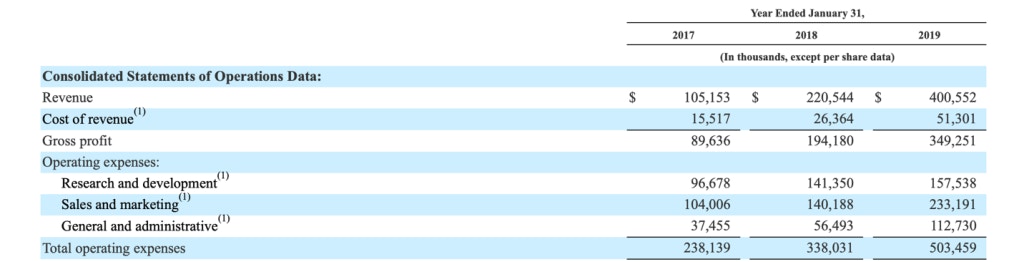

Slack’s prospectus reports “good enough” financials that will satisfy most growth investors. Revenue grew from about $105 million in 2017 to $220 million in 2018 to $400 million in 2019 representing growth of 110% and 82% respectively. International represents one-third of the revenue. The net losses were relatively flat, ranging between $138 million to $146 million for all three years, although Slack’s prospectus states the “net losses have been decreasing as a percentage of revenue over time as revenue growth has outpaced the growth in operating expenses.” This is true, but the decrease in operating expenses is due to cutting back on R&D as a percentage of revenue rather than sales and marketing. Relative to revenue growth, we see that the cost of acquisition remained the same with sales and marketing at about 64% of revenue in 2018 and 58% of revenue in 2019. As pointed out above, Slack should be spending on R&D to remain competitive in the cloud collaboration space.

On June 3rd, Slack released an updated prospectus that does not show any improvement in the net losses although the revenue grew to $134M in the most recent quarter compared to $80M in the year-ago quarter. In fact, the net losses of $38M in the most recent quarter are higher than the year-ago quarter of $26M.

Notably, according to the updated Prospectus, Slack shows growth in customers over $100,000, yet shows a decline across all paid user growth from 9,000 in the year-ago quarter compared to 7,000 in the current quarter. In other words, there is a divergence as overall paid users are declining while customer accounts over $100K is growing with the current quarter growing 24% compared the year-ago quarter. More quarterly earnings will be needed to determine which direction this will ultimately go.

4. Slack IPO Pro: Net Dollar Retention Rate

Slack provided limited key metrics in the S-1 filing although the company did provide net dollar retention rate. Net dollar retention rate depicts what percent of revenue from current customers is retained from the prior year, after accounting for upgrades, downgrades and churn. The formula for net dollar retention is:

Beginning of period revenue + upgrades – downgrades + churn = y with y / beginning of period revenue

If net dollar retention is above 100%, then the growth from the existing customer base offsets the losses. If the number is below 100% then downgrades and churn exceed growth.

Slack’s Net Retention Rate at 143% is very good and outperforms most cloud software IPOs that provided this number in the past. As mentioned in the introduction of this analysis, Slack has power users and a loyal brand following, which is reflected in the retention rate.

One thing to note about the retention rate is that Slack officially launched in 2014, and has a shorter history than other companies on this list with many having launched ten years prior to IPO. Typically, the longer the time period, the lower the net retention rate due to customer stabilization.

Conclusion: Slack will likely make a good trade due to brand appeal, traction and the current strength of cloud software in the market. The company knows how to make the financials look good by reducing R&D and maintaining similar levels of user acquisition as the year prior. For a long-term trade, I’d wait to see if the net losses improve and if Slack can prove that a direct listing was the best thing for the longevity of the company rather than in the best interest of the insiders. For Spotify, a direct listing did not fare well for early investors (including George Soros). With that said, Slack has stronger fundamentals than Spotify and is likely to be a very hot IPO. Follow me for updates, as the total addressable market for cloud collaboration is at $24 billion and with one or two strong quarterly earnings reports, Slack could transition from a solid short-term trade into a solid long-term holding.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per