Slowdown In Cloud Stocks On Thin Ice Following Q1 Guides

March 29, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Mar 23, 2023,09:56pm EDT

Following last quarter’s earnings, we published an analysis on cloud that showed hyperscalers were slowing (5%) sequentially and best-of-breed was slowing (12%) sequentially, based on Q4 guides.

What was most important for tech investors to realize, is that this is out of character for cloud, as Q4 is typically the strongest quarter. We concluded that this foreshadows a weaker-than-expected Q1 and also a weaker FY2023 than was currently baked into estimates.

Following the most recent earnings reports, our prediction is playing out that the slowdown we had predicted would worsen after the current quarter results.

This is important because the cloud category has treated investors quite well with recurring revenue, resiliency during Covid, and some of the strongest examples of product-market fit available on the public markets. However, not even this can overcome the effects of lower budgets and cloud spend, which is the top driver in terms of year-over-year comparisons.

Below, we discuss the fundamental weakness apparent in the most recent earnings reports. For our Premium Research Members, we are extending the analysis next week to include a few outliers that seem more resilient than others in the category, and those that are definitively the weakest.

Often times, identifying one or two strong companies in a category and patiently waiting can pay off, as the cloud category will put downward pressure on the stock price, including the outliers. Our goal is to buy the outlier(s) after they’ve been unduly penalized.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Big Tech: Bellwethers for Cloud Spend

Big Tech competes with best-of-breed cloud companies in nearly every capacity. For example, although most think of Azure when looking at Microsoft’s earnings reports, the company has a formidable presence in cybersecurity worth over $20 billion in revenue. Google’s BigQuery is one of Snowflake’s largest competitors, as is Amazon’s RedShift. I covered the differences between the three for Forbes here.

We also made the following point about why the Big 3 is an important proxy in our analysis: “Slowing Growth in Cloud Stocks: When Will We Hit a Bottom”

“The Big 3 are the best proxy because their reports represent the layer in the tech stack that tends to be the most resilient in terms of churn. The switching costs are quite high for cloud IaaS services. The Big 3 also afford a more concentrated view by owning 66% of market share across three companies whereas SaaS is spread across thousands of companies.”

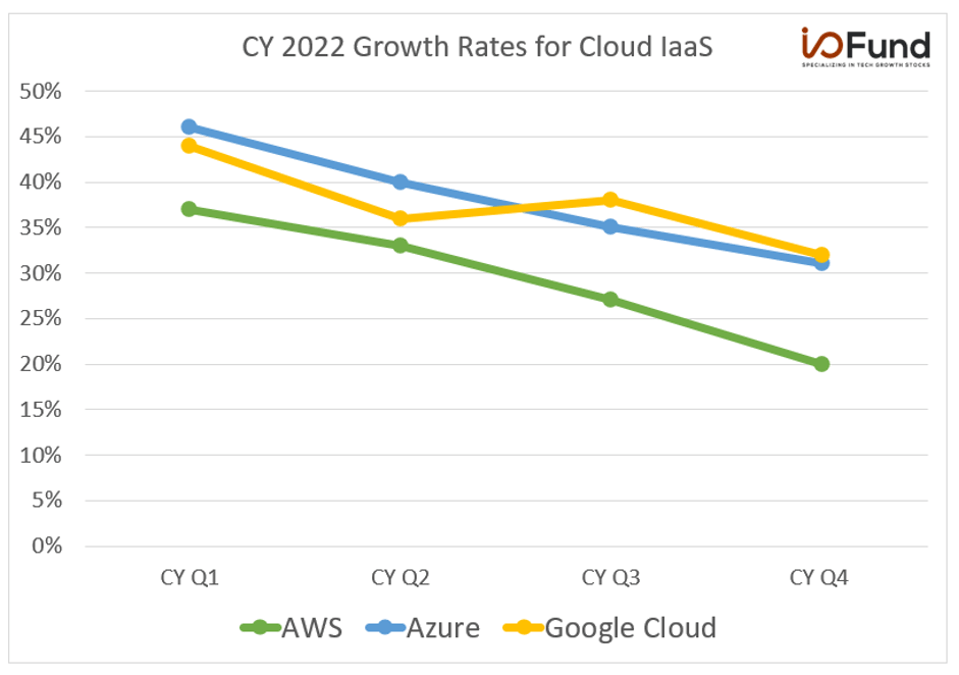

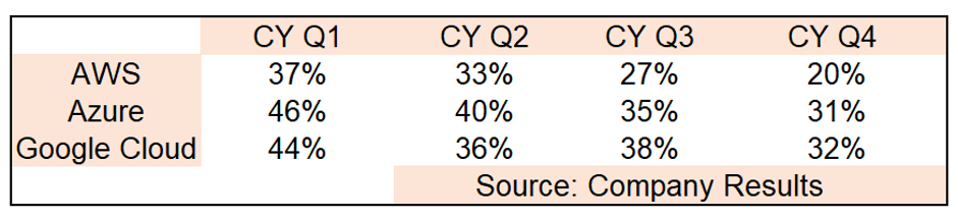

The slowdown over the past four quarters is quite visible:

The Cloud slowdown over the past four quarters is quite visible - I/O FUND

The Cloud slowdown over the past four quarters - COMPANY RESULTS

Key Highlights from the Cloud Hyperscalers:

AWS:

- AWS sales grew by 20% YoY to $21.4 billion in Q4, down from 27% YoY growth reported in Q3 and down from 33% YoY reported in Q2

- Q4 2022 growth rate of 20% was halved as AWS sales grew by 40% YoY in Q4 2021

- AWS revenue also missed the management guidance of 25% growth

- Guidance for Q1 was not provided, however, it was stated the YoY growth rates in January were “in the mid-teens”

Azure:

- Microsoft Azure revenue grew by 31% YoY and was down from 35% in Q3. In constant currency, it grew 38% and beat the management guidance by 1%.

- Microsoft Azure revenue grew by 46% YoY and also in CC basis in Q4 2021.

- The management provided guidance of 30% to 31% growth rate for the March quarter, down from 38% this quarter and down from 49% on a CC basis in the year ago March quarter.

- You may recall the 5-point deceleration announced in the October report caused concern in the market. This is technically a steeper deceleration.

GCP:

- Google Cloud revenue grew by 32% YoY to $7.3 billion and was down from 38% growth in Q3. Revenue missed the analyst consensus estimates by 1.5%.

- The growth rate was also significantly lower than last year’s growth (down about 1/3rd) when Google Cloud revenue grew by 45% YoY in Q4 2021.

What Big 3 Management Teams are Saying

When there’s evidence of a deceleration, analysts will typically ask the management teams to elaborate on the call with the idea of identifying how much more deceleration may be reported in the future and for how long.

Here’s a question regarding AWS’s slowdown:

Mark Mahaney

[…] Brian, just any color on why mid-teens is kind of a holdable growth rate for AWS over the next couple of quarters, given what looks like pretty clearly, continuing deterioration in enterprise demand?

Brian Olsavsky (CFO)

So on the AWS growth rate, I'm not sure I can forecast for you with any level of certainty what is going to happen beyond this quarter. You kind of — this is a bit uncharted territories economically. And as we mentioned, there's some unique things going on with the customer base that I think many in this industry are all seeing the same thing.

[..] And whether there's short term, perhaps short-term belt tightening in the infrastructure expense by a lot of companies, I think the long-term trends are still there. And I think the quickest way to save money is to get to the cloud, quite frankly.”

Amazon’s management also volunteered the following in their opening remarks:

“Starting back in the middle of the third quarter of 2022, we saw our year-over-year growth rates slow as enterprises of all sizes evaluated ways to optimize their cloud spending in response to the tough macroeconomic conditions. As expected, these optimization efforts continued into the fourth quarter.”

They expect the optimization efforts to continue at least for the next couple of quarters and, in the absence of proper guidance for Q1, said that the YoY growth rates in January were in the mid-teens.”

Per management: “As we look ahead, we expect these optimization efforts will continue to be a headwind to AWS growth in at least the next couple of quarters. So far in the first month of the year, AWS year-over-year revenue growth is in the mid-teens.”

Here’s what Microsoft’s CEO, Satya Nadella, said in the first part of his opening comments:

“As I meet with customers and partners, a few things are increasingly clear. Just as we saw customers accelerate their digital spend during the pandemic, we are now seeing them optimize that spend. Also, organizations are exercising caution given the macroeconomic uncertainty.”

Later in the call the CFO mentions, “As noted earlier, growth continued to moderate, particularly in December, and we exited the quarter with Azure constant currency growth in the mid-30s.”

The I/O Fund has launched a new $99/year Premium Newsletter called "Essentials" -- this newsletter delivers premium samples for our readers who want more actionable analysis for their tech portfolios. This month, we released a stock pick that we believe will be a leader in 2023 plus a video with the buy plan.

My Translation:

Cloud will see belt tightening in 2023 and investors will have to gamble on the timing for when this turns around. It could be in the next few quarters or it could take years. Most of this will depend on the economy, as the common denominator for cloud stocks is budgets.

To be clear, the category has the potential to be quite resilient, which we covered in 2019 when we said, “My prediction is this may be one of the last cycles when tech is considered less safe than value stocks. As the market will find out (the hard way), cloud software is actually very safe. It is insulated from trade wars and overseas manufacturing issues. It reduces costs for enterprises, which is ideal for a recession. Lastly, cloud software is at the beginning of a rapid growth cycle compared to its counterparts in tech — such as mobile, e-commerce and advertising — which are reaching saturation, are finding themselves in the cross hairs of anti-trust and are susceptible to consumer spending changes.”

There are a lot of cloud software bulls and for good reason, this category has treated investors well with predictable revenue growth. Cloud software is resilient because it drives down costs and increases productivity. We know this scenario well as we wrote about it many times in the past few years to defend cloud. Often, cloud selloffs were welcomed to position for a 6-month bounce back after the category sold off (40%) or more. I pointed this out in the past on the free side and here on MarketWatch (behind paywall) in 2019 (i.e., when we weren’t facing a brick wall on growth).

The issue with this assumption is that Cloud growth is actually slowing down —- that is the reality of things —- and this wasn’t true in 2019 and hasn’t been true in the last decade. Couple this with weak bottom lines that require cash injections, and what get is a sector that is largely out of favor.

What Analysts are Saying about the Big 3

Institutional analysts are able to do channel checks. It doesn’t hurt to see if there is more information available directly from large cloud customers.

Here are some recent analyst notes:

BMO Capital analyst Keith Bachman said until Azure growth stabilizes, the shares are likely to be range bound. The firm believes there is too much remaining uncertainty on Azure, which represents about 31% of BMO's revenue estimates.

Piper Sandler analyst Thomas Champion said that the Alphabet’s Q4 revenue and EBITDA missed across the board with advertising trends slightly weaker than expected, driven especially by Network. Search growth also slowed and Cloud growth decelerated 550 basis points. He further said Alphabet is transitioning the cost base for slower growth.

Piper Sandler analyst said that the Amazon’s Q4 results were mostly positive with revenues topping the high end of the guidance range. However, Amazon's guidance was slightly weak as Consumers sound cautious and the Cloud deceleration cadence appears to be landing in the mid-teens for Q1. The analyst believes management comments suggest the company is still navigating a difficult stretch.

Interesting enough, Dan Ives lowered his price target on Microsoft following earnings, yet has raised the price target again recently stating:

[…] [Wedbush is] "seeing steady cloud enterprise spending for Microsoft that has stabilized from the softness we saw in the month of December." Wedbush added that Microsoft, along with cloud competitors such as Amazon (AMZN), Google (GOOG), Oracle (ORCL), and IBM (IBM), are "seeing a surge of Beltway cloud deal activity in 2023 with a major shift to cloud underway from the Pentagon to civil agencies in the 202 area code."

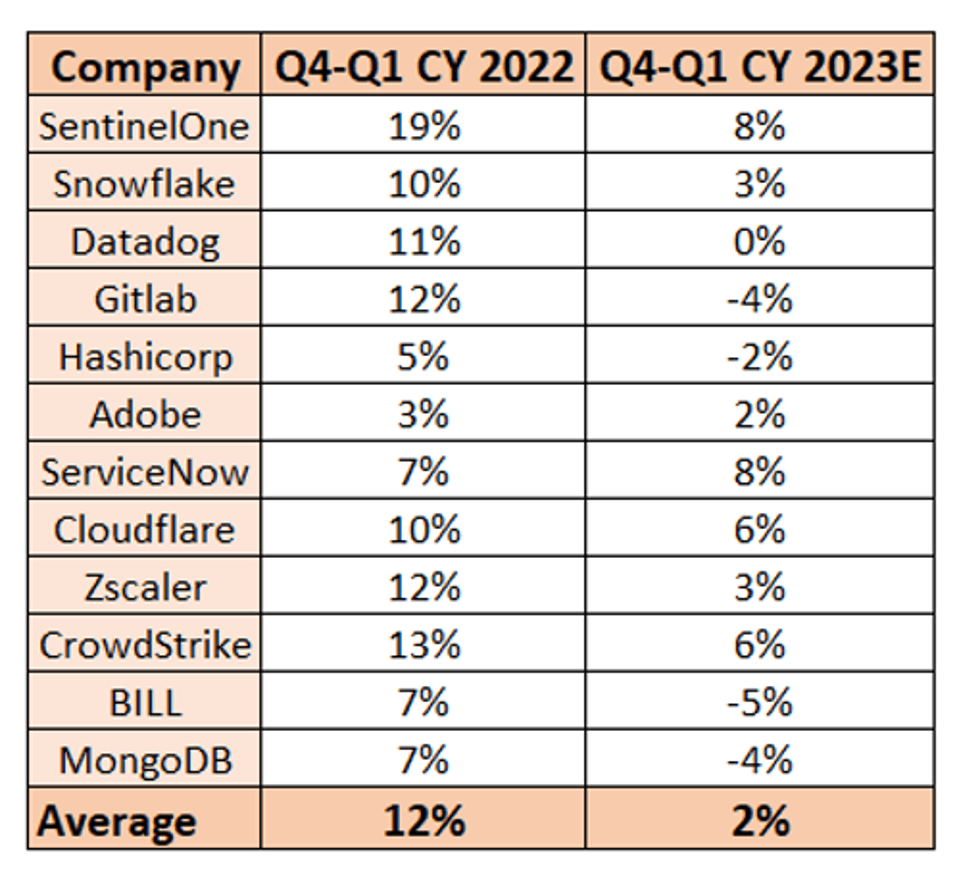

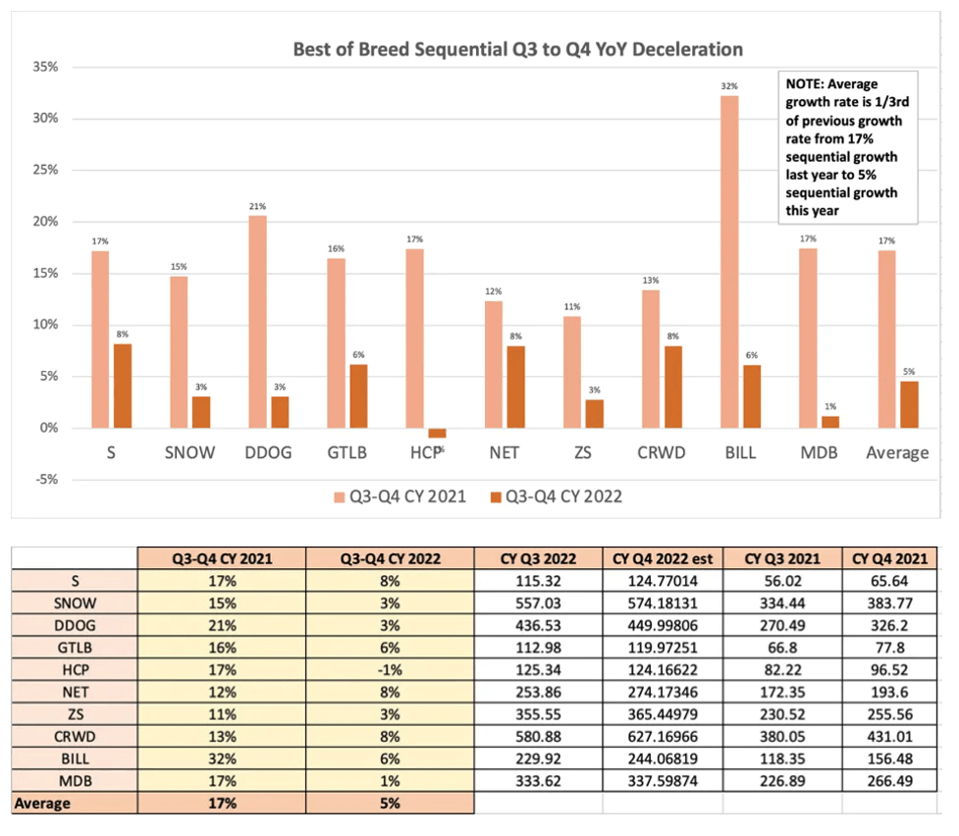

More on Best-of-Breed

To help illustrate how the deceleration is quite steep for some best-of-breed names, we took a sample of the top-ranking cloud stocks on revenue growth, free cash flow, adjusted operating margin and/or valuations.

Among the best-of-breed cloud stocks, only ServiceNow’s guide shows sequential growth. The company’s QoQ growth was 7% last year and is expected to be 8% this year. The largest deceleration was in GitLab, with revenue that grew 12% QoQ last year, is expected to decline (4%) sequentially this year.

Overall, the category is slowing down sequentially (a rather drastic) 83% for Q1 guides compared to the previous year — from an average of 12% QoQ last year to 2% QoQ growth this year.

As stated in our previous analysis, it’s assumed that H1 2022 was strong so YoY is less important than QoQ/YoY. This is because the cloud slowdown happened later in the market cycle with first management comments appearing in Q3.

For example, best-of-breed cloud reported a 71% slowdown in QoQ/YoY growth for Q4 guides and is now guiding for a 83% slowdown in QoQ/YoY growth for Q1 guides.

Best-of-breed cloud reported a 71% slowdown in QoQ/YoY growth for Q4 guides and is now guiding for a 83% slowdown in QoQ/YoY growth for Q1 guides. - YCHARTS

Here is how this compares to last quarter when we were seeing a 2/3 slowdown from 17% to 5% when I stated:

“Yet, the Q4 guidance is out of character as we see a 2/3 decline in average sequential growth rate from 17% to 5%. This is the more severe drop off because Q4 2021 was much better than Q2 2022 in terms of the economy. However, my contention is that Q4 could be reflecting what is to come in 2023 rather a reflection of budgets from 2022 as the slowdown is more pronounced in Q4 than it has been in previous quarters from 2022.”

Source: YCHARTS

Conclusion

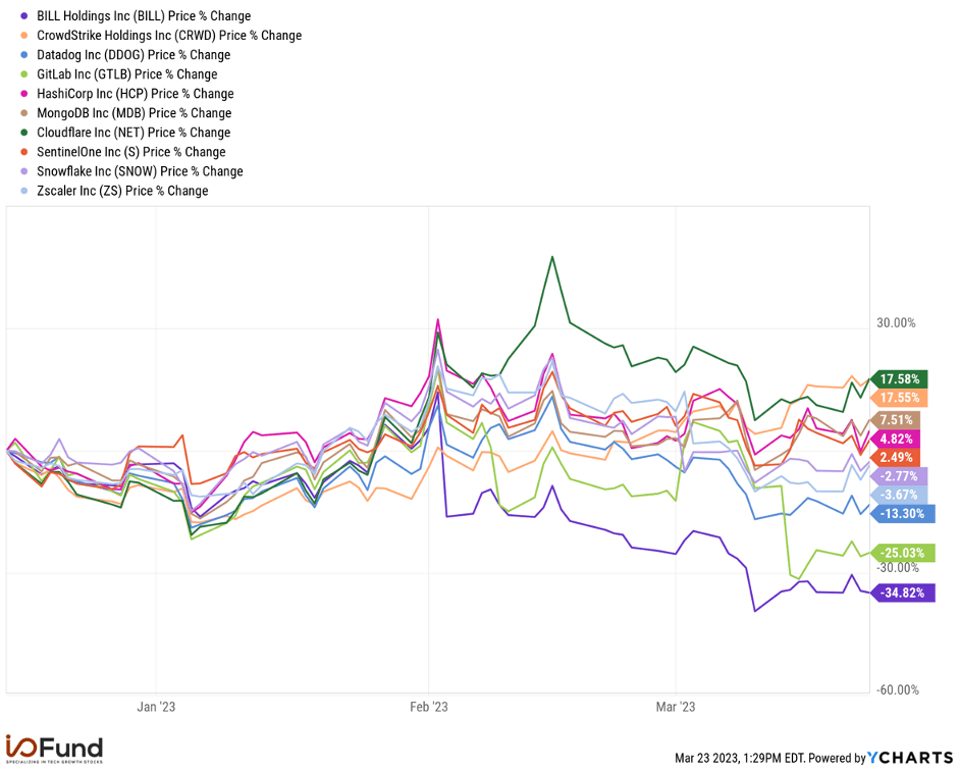

Below is cloud’s price action since we last covered the weakness in this sector. This is despite a surprisingly strong January and February for tech.

Above is cloud’s price action since we last covered the weakness in this sector. This is despite a surprisingly strong January and February for tech. - YCHARTS

Both Bill.com and GitLab saw weak price action compared to the others, and coincidentally, both saw sequential growth turn negative. Prior to the current earnings reports, I spoke about Bill.com and GitLab specifically with Samuel Burke of Real Vision when I forecast there would be further weakness in this category.

Many cloud stocks are on thin ice in this regard, and I imagine that if/when more cloud stocks turn negative on a QoQ/YoY basis compared to last year, weak price action will follow.

Source: Beth Kindig speaks with Real Vision about the cloud slowdown - REAL VISION

Every investor must determine their personal risk tolerance. The I/O Fund noticed unusually weak fundamentals in cloud in Q3 and re-allocated our positions to other sectors within tech at that time. However, we are hard at work in determining the one or two cloud positions we’d like to buy when this category reaches a bottom. We share our stock picks plus entries and exits with our premium members. You can learn more here.

Royston Roche, Equity Analyst at the I/O Fund, contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i