Apple is Not a Growth Company Anymore

November 01, 2019

Beth Kindig

Lead Tech Analyst

I grew critical of Apple earlier this year when it became clear the company would decline in revenue year-over-year, yet investors and analysts alike continued to pump the stock. With yesterday’s earnings report, we have further confirmation that Apple is not a growth company anymore although it continues to trade at growth valuations.

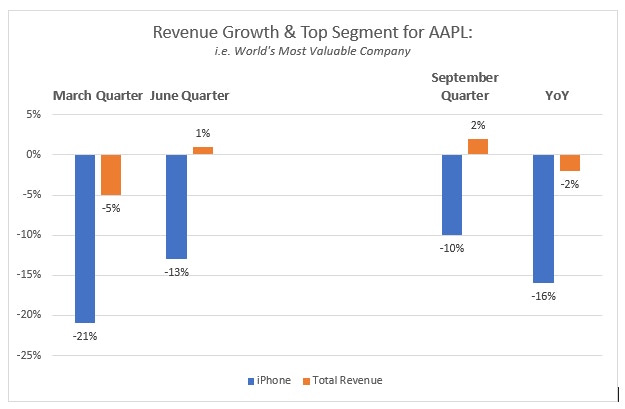

While many celebrated yesterday’s earnings report, there were notable signs of erosion. To start, Apple has lost $5 billion in revenue year-over-year, from $265 billion to $260 billion. This is despite having the “best fourth quarter ever,” according to Tim Cook. The truth is that the EPS was higher due to buybacks.

My analysis in MarketWatch published prior to earnings, pointed out that the iPhone was exposed to macro smartphone saturation. Those numbers showed a deeper decline than overall revenue with a $22 billion decline reported year-over-year.

Although Apple has ceased reporting smartphone unit sales, the numbers reveal there are fewer smartphone units being sold. Moving forward, with the recent release of the iPhone, Apple will contend with a lower average sales price. This is bound to affect smartphone device revenue moving forward, which declined at a rate of 15% year-over-year.

Overview of Mobile Saturation:

The smartphone market contracted to 1.462 billion units in 2017 and to 1.420 billion units last year. While almost 1.5 billion smartphones sales a year globally is substantial, the law of saturation drives down prices. I wrote about the price effects of mobile saturation in March, prior to Apple lowering prices for the first time with the iPhone 11.

China represents about one-third of smartphone penetration compared with the U.S., at one-12th. Pricing wars are evident in Asia, where China’s Huawei has grabbed market share to become the world’s fastest-growing smartphone seller. The company has seen a 66-fold increase from 3 million units sold in 2010.

Samsung may be the true bellwether for mobile, as the company is in first position for total smartphones shipped and is the world’s largest manufacturer of memory chips. In the first quarter, the company reported a 60% drop in operating profits, followed by a 56% decline in the second quarter. Analysts expect another decrease in the third quarter. Smartphone units have been making lower highs and lower lows over the past two years.

Samsung’s disappointing performance hints at the ties between smartphone sales and consumer confidence as China’s confidence index is languishing at a two-year low.

Notably, IDC forecasts the pricing wars will continue with 5G handsets in Asia, as low-cost models are expected to hit the market next year. In the U.S., Latin America and Japan, the average selling price (ASP) of a 5G handset will be around $1,000, while it will be $600 in China.

Don’t Believe the Earnings Beat:

The fiscal Q4 earnings beat is at odds with overall performance. Although profit topped expectations, this is the first time since Tim Cook took over in 2011 that Apple declined in profit in all four quarters of a fiscal year.

The media touts the services revenue as the answer to the iPhone decline. As we saw this year, double digit declines on the segment responsible for $165 billion in revenue (iPhone) is not easily staved off by a revenue segment posting $40 billion per year (services).

If one did not look closer at the numbers, it would easy to think services was a major growth segment. We see the growth was at 18%, which is below the 20% traditional benchmark that defines growth. As of now, this doesn’t appear to be the answer to the gaping iPhone decline. This is proven by the annual decline in overall revenue.

Wearables growth of 55% to $24 billion in revenue is decent. However, again, the iPhone decline was steep enough at $22 billion to wipe out the entire Wearables category.

I had pointed out in a Fox Business News interview prior to earnings that its unlikely lightning strikes twice with the iPhone as it’s not only one of Apple’s best growth drivers historically, but it’s also one of the best growth drivers we’ve seen across the tech industry. This is evident in last year’s smartphone revenue of $165 billion, which I also pointed out will be Apple’s peak year in mobile.

https://www.youtube.com/watch?v=ClLBzohNeE0

Note: although I provide an entry price for Apple on Fox Business News, this is something Knox Ridley specializes in and covers as a contributing analyst to our premium site Tech Insider Research. You can catch his detailed technical analysis published on Seeking Alpha next week.

Here is a snapshot of Apple’s performance over the past year. If the stock ticker was not attached to the graph, it would be hard to guess this is the world’s most valuable company.

As most investors know, Apple has plenty of cash. It produces about $50 billion-$60 billion a year in free cash flow and has over $100 billion in cumulative reserves to fund new projects. While analysts are optimistic about many new pivots, these will weigh on margins. This is especially true for Apple TV+, which comes with a high content bill and low subscription revenue, as the OTT streaming service will be bundled for free or priced at $5.

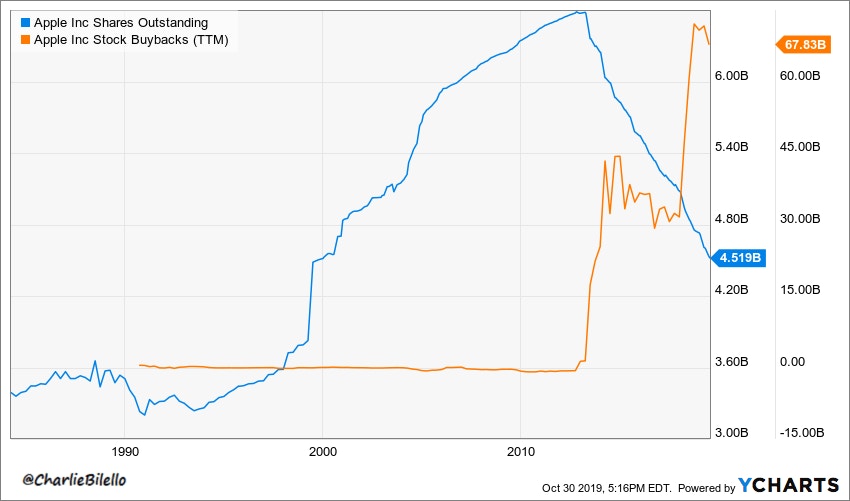

Keep in mind, Apple’s cash reserves are seeing the effects of the buybacks, and Alphabet has now surpassed Apple in cash reserves. Apple has $102 billion compared to Alphabet’s $117 billion. This is due to Apple spending $122 billion on stock buybacks since the beginning of 2018. Alphabet is growing, as well, at a rate of 20% year-over-year.

Analysts who are raising Apple’s price target based on fiscal 2020 cite Apple TV+ revenue as a primary reason with little discussion of the forecast for Apple’s main growth driver. Apple TV+, which will compete with Amazon Prime Video, Netflix and other TV-streaming services, is more likely to cause bottom-line losses in the short term as Verizon is offering the subscription for free while requiring costly original content from headliners such as Oprah. (She doesn’t come cheap.)

In my opinion, these new price targets seem more like an attempt to cover current positions, as the majority of institutions are holding this stock at lower entry points.

Also Read: Apple’s Stock Price is at Inflection Point

EPS not as Relevant Due to Buybacks

Many Apple proponents will use the stock as an income stock, yet the company trades at growth valuations. The buybacks Apple is doing on a consistent basis is alarming for a tech company, who should be innovating with cash reserves rather than propping up the stock price to beat earnings per share.

In the most recent quarter, Apple disclosed it had spent $17.9 billion to buy back 92.6 million shares during the fiscal fourth quarter. During the three prior quarters in the fiscal year, Apple had spent $49.2 billion. There is $78.9 billion remaining in its stock buyback program. The reduced share count this year has helped Apple beat earnings per share of $2.91 with $3.03 reported with fewer outstanding shares as a result of the buyback.

Apple has bought a total of 2 billion shares over the past six years, which brings the shares outstanding to their lowest level since 1999, according to Charlie Bilello, who is also a Seeking Alpha contributor.

Conclusion:

Apple will be particularly exposed to lower consumer confidence when this occurs. Mobile saturation is already showing its effects with a $22 billion loss in iPhone revenue year-over-year. In fact, the saturation of the iPhone could prove to be one of Apple’s biggest challenges to date, as the company attempts to make many pivots, all of which will add noise to the big picture that mobile’s golden days are behind it. This will not be resolved by a single quarter’s earnings “beat,” nor will it be absorbed by services revenue until at least 2023.

If your investment thesis is to focus on primarily cash reserves and cash flow, while ignoring growth and the leverage of buybacks to boost EPS, then Apple is likely in your portfolio. As a tech analyst, who look towards future growth for the highest gains, this is a company where I am personally on the sidelines and is not a company I can recommend long-term.

A version of this analysis appeared in MarketWatch on October 29th, 2019. It has been updated and lengthened post-earnings.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i