Netflix Stock Will Be A FAANG Again

November 01, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Oct 27, 2022,11:14pm EDT

Netflix lost it’s status as a FAANG when the stock fell from a $300 billion market cap to a $100 billion market cap this year. My firm entered Netflix in August as we fully expect the stock to become a FAANG again due to its revenue potential from ads and improving cash profile.

Given macro, very few tech companies have a catalyst of any kind on the horizon with many companies in a defensive stance. Netflix, on the other hand, has an offensive plan to grow subscribers and revenue even in the face of macro pressures.

In my free newsletter published on Forbes, I had stated in both June and July: “I would argue the day that Netflix’s stock price dropped 35% was consequently one of the most important days in the company’s history in terms of its chances for a boost in revenue and a renewed uptrend. Patience, though, will be required, as Netflix has work to do.”

My target for the roll-out was originally Q1 to Q2 2023, and instead, Netflix is rolling out the ad supported tier next week. My firm had entered the stock in August with a real-time trade alert, so the surprise 6-month roll-out was welcomed. The ad supported tier will monetize at the same rate or even higher than legacy tiers with a $6.99 monthly subscription combined with a $10 ARPU over time (needs time to ramp to reach this ARPU).

A high probability of revenue acceleration from ad tier combined with improved cash profile combines for an attractive stock for 2023. Not only will Q4 and Q1 provide some clues around the new trajectory but there is an additional catalyst in Q1/Q2. We are reserving details about this lesser known catalyst for our research members.

The biggest names in tech are reporting their earnings right now, and our premium members are getting updates almost daily. Learn more about about our premium membership here.

Netflix is Expected to Return to 2021 Subscriber Growth Levels

Netflix had a sizable beat on subscribers and the stock breathed a visible sigh of relief as the company comfortably beat with 2.4M net adds compared to 1M to 1.2M expected. Consensus for next quarter was 4.1M with Netflix guiding for 4.5M. This will be the largest account growth since Q3 2021.

The largest contributor to growth is the APAC region at 1.4M new subs followed by EMEA at 0.6M subscribers and LatAm at 0.3M subscribers. United States and Canada reported 0.1M subscribers whereas in the past this region saw churn.

Revenue was up 5.9% compared to 4.7% expected. On a constant currency basis, revenue grew 13% YoY.

There is a miss on revenue for next quarter due to FX headwinds. The company guided for 1% growth versus 3.5% growth expected. On a constant currency, Q4 is expected to grow 9%. This creates a slight miss on FY2022 revenue at $31.5 billion guided versus $31.6 billion expected.

The AVOD tier is most likely targeting the 100M who are sharing passwords. Therefore, I believe Q1 is when the stronger results will appear from Netflix’s AVOD entry due to the password sharing being phased out early next year.

Here was the update:

“Finally, we’ve landed on a thoughtful approach to monetize account sharing and we’ll begin rolling this out more broadly starting in early 2023. After listening to consumer feedback, we are going to offer the ability for borrowers to transfer their Netflix profile into their own account, and for sharers to manage their devices more easily and to create sub-accounts (“extra member”), if they want to pay for family or friends. In countries with our lower-priced ad-supported plan, we expect the profile transfer option for borrowers to be especially popular.”

Operating margin came in higher than expected at 19% versus management’s previous guidance of 16%. There was a 4% decline from the previous year due to FX. The company is guiding for an operating margin of 4% to 8% next quarter, or 10% on a constant currency (CC) basis. This is due to seasonal spending on marketing and content, and on a CC basis, will be higher than last year’s 8.20%.

The revenue and operating margin beats flowed through to a net income beat of $1.39B compared to $961M expected.

Operating cash flow was at $557 million and free cash flow came in at $472 million. This means management has made good on its promise to see $1 billion FCF this year. It also implies FCF could be ($287) million next quarter as we are at $1.287 billion for the year.

Netflix reiterated regarding the FCF next year: “We continue to expect FCF of +$1 billion for the full year 2022, plus or minus a few hundred million dollars and substantial growth in FCF in 2023 (assuming no further material appreciation of the US dollar).”

There was a minor improvement in Netflix’s cash and debt levels with cash increasing to $300 million to $6.18B with net debt of $7.98B. This is down from net debt of $8.5B in the previous quarter.

The company had a big beat on EPS of $3.19 versus $2.17 expected. This included a $348 million non-cash unrealized gain from FX remeasurement on Euro denominated debt.

Was the Market Wrong About Netflix Saturation?

Netflix does not believe their market is saturated, rather that advertising opens up a new, sizable addressable market. The company offered the following information: “In the 190 countries in which we operate, our $30 billion-plus of annual revenue is roughly 5% of the combined estimated ~$300 billion pay TV/streaming industry, ~$180 billion branded advertising market, and $130 billion consumers spend annually on gaming. So, we believe that we have a long runway for growth if we can continue to improve our offering steadily over time.”

We had stressed in our previous free newsletter that the lagging discussion on Netflix is that there was a subscriber decline in Q1 of 200,000, excluding Russia and a subscriber decline of 970,000 in Q2. While critics believe this is due to saturation, it’s much more likely the decline is coming from a pull forward due to Covid as all media stocks – both streaming and social media – demonstrated outsized audience growth through Q2 2021. Therefore, Netflix is lapping some tough quarters for audience growth comps and announced in April their plan to have an ad tier to help combat this.

Management’s willness to combat subscriber falloff with an ad tier is why we entered in August prior to the subscriber beat.

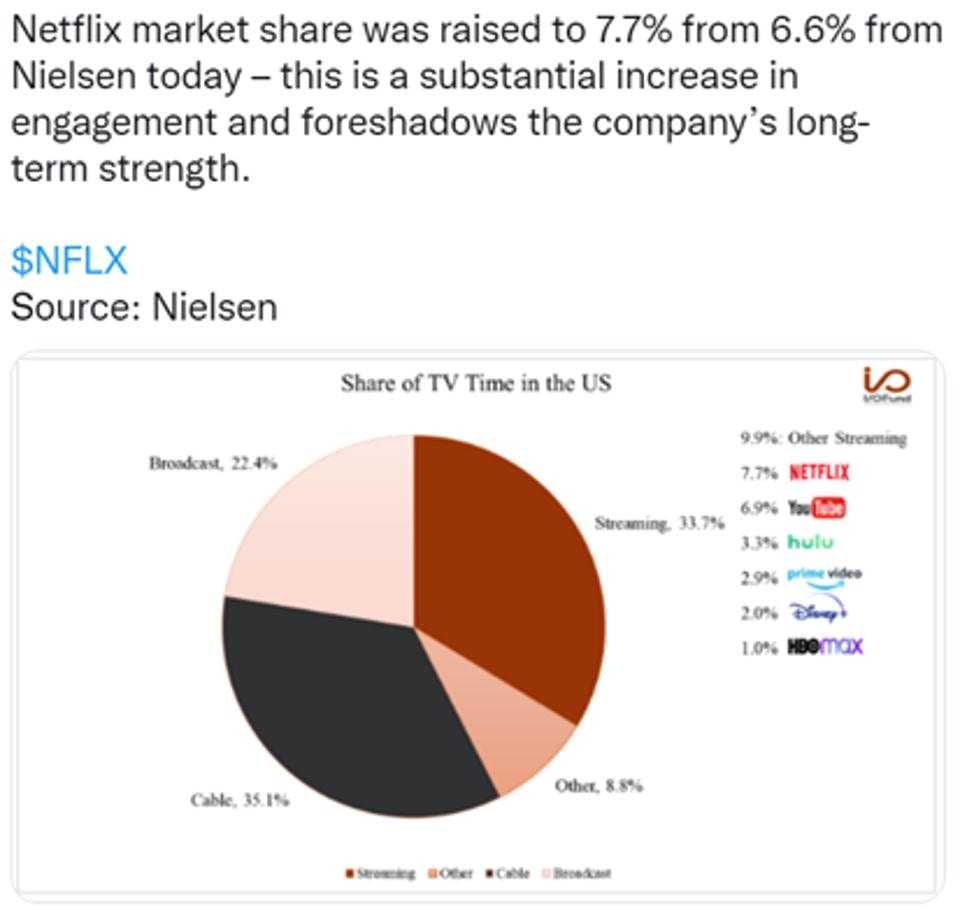

Another important point we had highlighted was there is already evidence that Netflix is taking more market share than its peers. In fact, Nielsen raised Netflix’s market share earlier this year for engagement to 7.7% from 6.6%, which puts Netflix in the lead over any other competing subscription service.

Source: Beth Kindig Twitter

Management could not be more clear in their Investor’s Letter or on the earnings call that having the streaming best content in the world is their #1 strategy for success. That is one reason I track statistics such as Netflix’s share of TV time very closely. There was discussion that Netflix fully accepts the cost of creating the content and is instead more focused on getting more value from $1 billion in content than their competitors.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

More on the Ad Tier

Here was the update from Netflix regarding the new ad-supported tier from the Investor’s Note:

“As we’ve been discussing over the past few quarters, improving our pricing strategy is an important near-term focus. Last week, we announced that we’ll be launching an ad-supported subscription plan on November 1 in Canada and Mexico; November 3 in Australia, Brazil, France, Germany, Italy, Japan, Korea, the UK, and the US; and November 10 in Spain. Cumulatively, these 12 markets account for ~$140 billion of brand advertising spend across TV and streaming, or over 75% of the global market.

To start, we’re keeping it simple by offering one low-priced ad plan – Basic with Ads – at a price that’s 20%-40% below our current starting price. So in the US, for example, Netflix will now start at $6.99 per month (compared to $9.99 today). The Basic with Ads plan will have ~5 minutes of advertising per hour, frequency capping and strong privacy protections.”

Netflix has been able to launch its ad platform within 6 months of the announcement. The announcement earlier this month was good news for Netflix investors who entered early despite many institutional analysts predicting it would be six months into 2023 before it rolled out.

Also on the earnings call, management stated they are not expecting any material financial impact this quarter from ads due to the intra-quarter launch. However, over time, the company expects the ad tier to be margin accretive. My personal take is that it can produce a slight boost in subscribers in Q4 and this glimpse is going to be one that I am very much looking forward to. Management has no visibility at this time as it launches in two weeks so it’s prudent to not guide beyond the visibility they currently have.

Summary/Conclusion:

I believe that one day, investors will look back and see that it was a buying opportunity when Netflix went down 35% in April of 2022 after the company announced it’s plans to move into advertising. The goal of the ad tier is address saturation head-on by increasing the addressable market.

Netflix beat on revenue, subscribers, operating margin, and free cash flow in the recent Q3 results with small improvements from Q2 across the board in what may have marked the bottom for this company. The Q4 guide is also in-line across the board.

The company is expected to be free cash flow positive this year. Netflix has only been FCF positive in 2020 and has not been FCF positive in any other previous year. The company also lost $3.3 billion in 2019 when it built its original content pipeline. The stock will now enter two years of FCF positive between 2022 and 2023.

Advertisers are likely to pay a high premium for Netflix’s Hollywood-level content. Notably, it was recently revealed Netflix plans to only have 5 minutes of advertisements which is why the ARPU target is $10, however, that comes out to a target of $16.99 per user with the $6.99 pricing tier.

It’s not only the 100 million people sharing passwords that illustrates what the uptake could be for a lower-priced tier, it’s also the high level of engagement the company’s content garners that could make for a nice equation for with demand from exclusive advertisers and supply from the premium content, that Netflix offers.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund own Netflix at the time of writing.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per