Netflix Stock Stronger Than It Seems Following Q2 Earnings

July 28, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jul 22, 2022,01:44pm EDT

Netflix is trading at a 10-year historic low valuation, which means this is an opportune time to discuss the pros and cons of this stock should there be upside potential.

The lagging discussion on Netflix is that there was a subscriber decline in Q1 of 200,000, excluding Russia and a subscriber decline of 970,000 in Q2. While critics believe this is due to saturation, it’s much more likely the decline is coming from a pull forward due to Covid as all media stocks – both streaming and social media – demonstrated outsized audience growth through Q2 2021. Therefore, Netflix is lapping some tough quarters for audience growth comps.

Netflix management was clear that this quarter was “less bad” as they hinted the company is not exactly celebrating the results. The company technically returns to growth next quarter for subscribers with a guide of 1 million, yet this is a marked decline from the 4.4 million in the year ago quarter. As discussed, due to the overall impact across many media stocks from shelter-in-place, it would be hasty to believe there’s something inherently wrong with an individual company when the entire media industry was affected. It’s better to hold those conclusions until H2 2022 through H1 2023 after giving it a full year after tough Covid comps have cleared. Ultimately, media is very seasonal, and we should have a nice glimpse as to which companies emerge stronger by Q4 2022, as this is the strongest quarter seasonally.

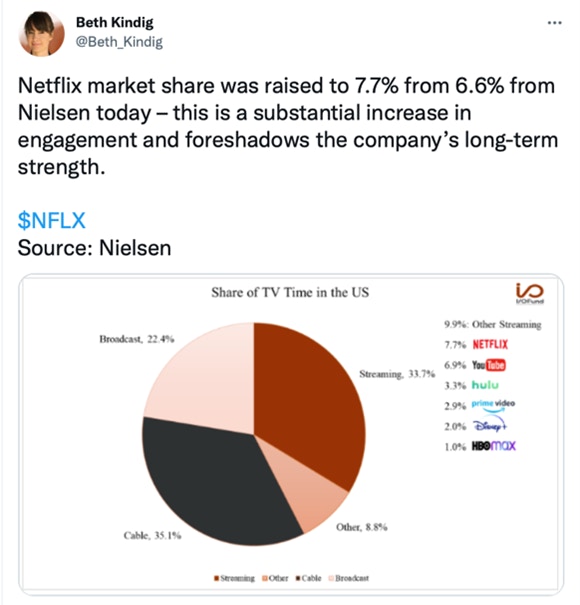

With that said, there is already evidence that Netflix is taking more market share than its peers. In fact, Nielsen is raising Netflix’s market share for engagement to 7.7% from 6.6%, which puts Netflix in the lead over any other competing subscription service. This is due to high-quality content such as Stranger Things 4, which reported 1.3 billion hours streamed.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Advertisers are likely to pay a high premium for Netflix’s Hollywood-level content. It’s not only the 100 million people sharing passwords that illustrates what the uptake could be for a lower-priced tier, it’s also the high level of engagement the company’s content garners that could make for a nice equation for industry-leading ARPU due to demand from exclusive advertisers coupled with the supply, or premium content, that Netflix offers.

Due to FX headwinds, Netflix missed on revenue in the most recent quarter at 9% revenue growth compared to 9.7% expected. However, on a constant currency basis, revenue growth was 13%. The same was true for Netflix’s guide, it was a miss due to FX headwind at 4.7% for the upcoming Q3 quarter, yet on a constant currency basis, it is a 12% guide on revenue and a beat in that regard.

Above: Portfolio Manager of I/O Fund, Knox Ridley, discusses Netflix earnings results.

Not surprisingly, the operating margin was also affected by the strong dollar at 20% in the current quarter and 16% for Q3. The strong dollar led to a slightly better EPS as Netflix saw a $305 million unrealized gain from F/X remeasurement on Euro debt.

The most important line item for Netflix is the company’s cash flow. Looking back, this has been troublesome for Netflix as the company lost $3.3 billion in cash in 2019 as it built up its original content pipeline. However, the company is on an entirely new trajectory with $1 billion in free cash flow expected this year and “substantial” free cash flow in 2023, per Netflix management.

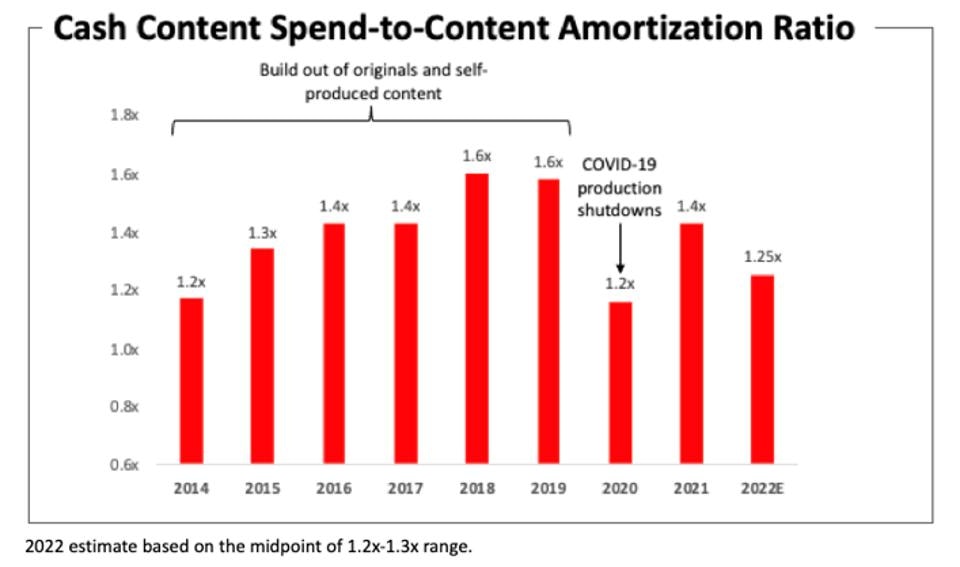

The new and improved trajectory in free cash flow won’t change the company’s debt levels anytime soon. Netflix is firmly setting expectations for $10 to $15 billion in debt into the foreseeable future. This is necessary to continue to hold its place as the top media company in terms of revenue and engagement. Gross debt stands at $14.3 billion, when accounting for $5.8 billion in cash, net debt is at $8.5 billion. The company has been able to improve its cash content spend-to-content amortization ratio from 1.6X to 1.4X in 2021 and an expected 1.2-1.3X in 2022.

NETFLIX’S Q2 2022 INVESTOR LETTER

Forward-Looking Catalysts:

Netflix has a few new paths to monetization and to re-accelerate subscriber growth. The company is rolling out a new password-sharing plan and is also now partnered with Microsoft on ads to roll out in 2023. More time than not, cross-selling results in higher revenue where someone who would normally churn can now be monetized through ads. Likewise, viewers who can try out Netflix may decide to upgrade to remove ads. Ultimately, the move towards ads also helps Netflix to be more recession-proof in the event households decide to cut costs.

Risks:

We do not see the current soft subscriber numbers as a sign of saturation. Netflix has risen in market share over the past year. Instead, soft subscriber numbers are a result of the pull forward nearly all media companies experienced from Covid. We fully expect Netflix will return to normal subscriber growth due to the catalysts listed above.

Instead, the primary risk for Netflix is its debt in a rising rate environment. This may depress the company’s valuation more than its ad-tech peers who have strong cash flow and little to no debt during tougher macro conditions. Netflix cannot temper this debt if it intends to compete against other subscription streaming services and also the many broadcast networks that have migrated to streaming.

There is also execution risk with a pivot from subscription-only to also including the ad tier. We view the Netflix management team as perhaps the most capable in the industry of pulling off this pivot as they have consistently broken ground in areas much more challenging than introducing ads. In addition to this, CTV ads can monetize at $40 ARPU and we believe Netflix content will set a new record on ARPU. With that said, even if the execution risk is lower than it would be with other management teams, Netflix is likely to fetch a higher valuation after its proven the ad tier will be successful – ETA of H2 2023.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

What to Watch: Price Action for Netflix Stock

The big picture question to ask is – has NFLX put in THE bottom? There are 3 scenarios that could unfold from the current price range, that would help us manage risk around this question:

I/O FUND

Red: If NFLX breaks below $185, the odds favor one more low, which would be targeting the $147-$115 region. If this happens, it greatly reduces the odds that NFLX will see new highs in the next growth cycle.

Orange: The current swing up breaks above $250. If this happens, the odds favor a push into the $340-$405 region. If this scenario is playing out, we would see the uptrend stall in this region in a bear market rally. The same lower price targets would hold in this scenario.

Green: If any renewed uptrend can break above $405, the odds will shift towards a move to all-time highs.

Netflix bottomed in May while the rest of the market went on to make a new low. More times than not, stocks that bottom first, tend to lead into the next uptrend. This is a show of strength worth monitoring.

We only have 3 waves down from the 2021 high. This may not seem significant, but it is. If this 3-wave move down turns into 5 waves down (red scenario), the odds that we push deep into the orange range are low before the next leg down.

The Relative Strength Index (RSI) has reclaimed a significant level. Note the blue arrow on the RSI around 57. This was the spot where price topped just before the waterfall moment happened in this bear market. The fact that the recent push higher has reclaimed this level is a show of strength and an early sign that green/orange is likely playing out.

Conclusion: The odds favor a push into the $340-$405 region. As long as the next dip holds $185, the more aggressive play would be to buy into that dip. A safer play would be to wait for the breakout above $250.

Knox Ridley, Portfolio Manager at the I/O Fund, contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de