Nvidia Stock: How We Plan To Position For Q2 Earnings

August 29, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Aug 23, 2023,12:30pm EDT

You’re probably well aware that last quarter, Nvidia guided fiscal Q2 at $11 billion, which is 53% higher than analyst expectations of $7.2 billion. The stock was up 25% after hours, adding $200 billion to its market cap in the matter of a day. During the earnings call, the stock went from being up 15% after hours to being up 25% after hours when the CFO confirmed H2 would also be strong with visibility on supply.

In addition to covering Nvidia’s AI angle many times since 2018, the I/O Fund holds an outsized Nvidia position at 17% allocation. Going into this year, we broke all of our portfolio management rules by holding a position that was over 10%. From there, we’ve talked consistently about a H2 2023 Semi Rebound to our premium members in webinars and analysis. I was also interviewed by Tier 1 media in August of 2022, and January of 2023about this very high conviction. As you know, Nvidia would later beat in May.

Source: BETH KINDIG

Well, it’s the day of Q2 earnings, so let’s cut to the chase … what should Nvidia investors do now?

Below, we will review why it’s likely Nvidia beats and sees expanding margins, and secondly, we will review our plans for our outsized position. My firm is unique in that we do not simply offer blanket buy recommendations, rather we disclose our trades in real-time to our premium members. Please also note our disclosure below that we cannot guarantee a stock’s performance, but we can tell you how the firm is managing our money.

As a reminder, Super Micro had a sizable beat with management doubling fiscal year guidance three months later from 20% to 40%, yet the market reacted harshly. Therefore, it is the practice of our firm to have an active portfolio stance by combining fundamentals and technicals for risk management.

Nvidia Stock: Will a Beat Be Enough?

It’s not a stretch to say that anticipation within the investment community is on par with the series finale of Game of Thrones. Everyone in the market will be watching this earnings report come market close.

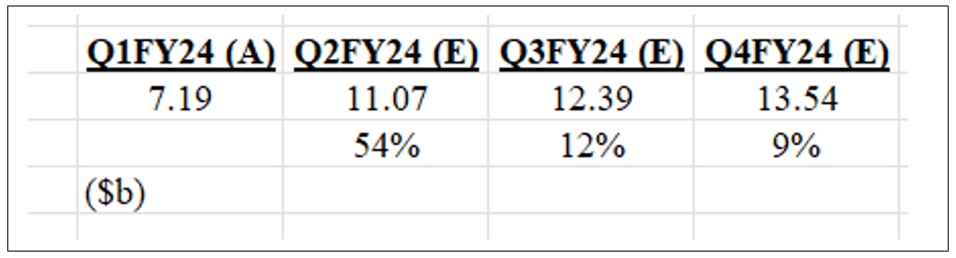

In its Q1 announcement, Nvidia provided a first glimpse into the financial impact AI will have on its businesses with Q2 sales guidance of $11.07b. The sequential increase of +54% vs Q1 surprised the market. We expect Nvidia to only provide guidance into Q3. Although just one quarter, it will be an important data point for the market to assess the appropriate growth rate for the remainder of FY2024 and FY25.

Q2 SALES + Q3 GUIDANCE

Meeting or beating Q2 sales guidance and providing Q3 sales guidance better than consensus will be very important drivers behind Nvidia’s short-term stock performance.

During the earnings call, this was one of the comments that contributed to strong price action after hours:

“Vivek Arya:

Thanks for the question. Could I just wanted to clarify does visibility mean data center sales can continue to grow sequentially in Q3 and Q4 or do they sustain at Q2 levels? […]

Colette Kress:

Yeah, Vivek. Thanks for the question. Let me see if I can add a little bit more color. We believe that the supply that we will have for the second half of the year will be substantially larger than H1. So, we are expecting not only the demand that we just saw in this last quarter, the demand that we have in Q2 for our forecast, but also planning on seeing something in the second half of the year. We just have to be careful here. But we are not here to guide on the second half of that. Yes, we do plan a substantial increase in the second half compared to the first half.

On 6/14/23, Collette Kress, Nvidia CFO held a Q&A at the Jefferies Investor Conference . In particular, there is one question on all investors’ minds.

Question

“You guys gave guidance for the July quarter, which beat everybody’s expectations and 50% sequential growth. And I think there is a concern from investors that this is kind of a one-time spike that will come back down. I know you only guide one quarter at a time. But what do you say to investors who have a concern that it’s a one-time spike? And can you just talk in general terms, what is the visibility typically like with the data center and hyperscale companies?”

Colette Kress

“Yes. What we have seen is certainly an astounding amount of interest worldwide globally from many different types of customer sets […] We have better visibility than what we have seen before and our ability to focus right now on procuring the supply.

As we indicated in our earnings, we have procured the supply to the demand that’s been put in front of us and that visibility that we see. […] So our guidance for Q2 is really building upon years and years of working of the industry on accelerated computing and solutions such as AI. And we continue to see demand and demand visibility for the full year as well that we believe will sustain as we finish in Q2.”

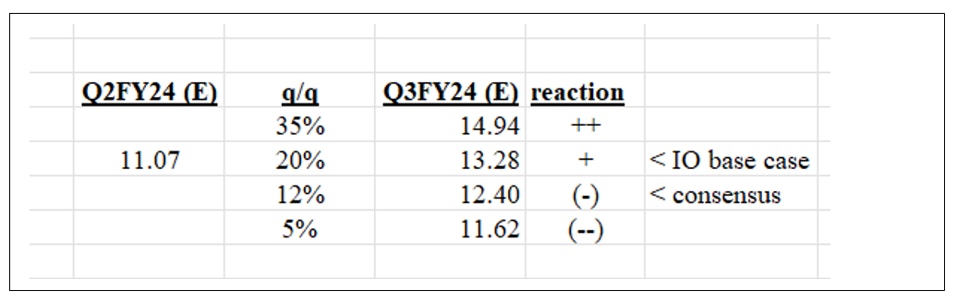

Comparing her response to consensus sales estimates for the remainder of FY24, we come away with a couple of observations.

Source: I/O FUND

- For Q2, consensus is in line with Nvidia’s guidance. There’s a chance that Nvidia will exceed their own forecasts

- If Nvidia has indeed procured the supply needed to meet demand, we believe that consensus Q2/Q3 growth estimates of +12% is too conservative.

However, the magnitude of the Q3 guidance will be very important given heightened expectations. Assuming Nvidia meets its Q2 guidance, we’ve put together a simple scenario analysis to parameterize the different outcomes we anticipate based on Nvidia’s potential Q3 guidance. +/- indicates anticipated stock positive or negative price performance on the next trading day based on that scenario.

Source: I/O FUND

We’re optimistic that continued strength in AI related demand and stabilization in gaming will allow Nvidia to meet if not exceed their Q2 guidance. According to the Financial Times, “multiple sources close to Nvidia and its manufacturer, Taiwan Semiconductor Manufacturing Company, the chipmaker will ship about 550,000 of its latest H100 chips globally in 2023, primarily to US tech companies. Nvidia declined to comment.”

At $40,000 per H100, that equals $22 billion in H100 sales alone, and when you add the A100 and other data center sales at a current run rate of $14 billion, the data center segment could report a total of $36 billion in 2023. When you equal this out across the upcoming quarters, it looks something like this:

Q1: $3.5B A100s, $750M H100s = already reported, $4.2B

Q2: $3B A100s, $5B H100s = $8B data center, guided

Q3: $2B to $3.5B A100s, $7B H100s = $9B to $10.5B data center

Q4: $2B to $3.5B A100s, $10B H100s = $12B to $13.5B data center

H100s are priced differently depending on where they are sourced. The Information has the H100s at $20,000 yet sourced an analyst that believes we could see over 1M H100s sold in 2023. This arrives at $35 billion in sales. Given these variables, and credible sources, it appears $30 to $40 billion is the range going into Q2 earnings that analysts want to see for full year data center revenue.

We believe the market will react negatively if Nvidia provides Q3 guidance that is in-line with consensus or lower than 12%. On the flip side, Nvidia will likely need to provide guidance of at least greater than 20% for a significant positive reaction. This is because consensus will likely need to make upward revisions to their earnings for the remainder of FY2024 and FY2025. This is critical to support the current valuation.

Our base case assumption is that Nvidia’s Q3 guidance will estimate q/q growth of at least +20%. Remember, H100 was only introduced to the market toward the end of the last calendar year. Q1FY24 was the very first quarter where Nvidia is beginning to see the impact of AI and demand for the H100. Ultimately, we believe Nvidia will close out the year with data center revenue that is 50% higher than Q2.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Q2 + Q3 MARGIN GUIDANCE

At the same conference, in response to a question of how much of revenue growth is pricing vs units, CFO Kress answered

Question

“I know that you have fielded this question probably 1,000 times since you reported there is kind of this view that all of your growth is driven by ASPs and maybe not as much by units. And how should investors think about the ASP growth versus the unit growth in the quarter past and the quarter outlook?”

Colette Kress

“No. We truly are seeing demand and need across such a wide group of folks. And that’s not just based based on selling a brand new architecture and ramping a new architecture, Hopper architecture. We are still shipping our existing prior architecture. But no, this is not about ASPs, this really is about just the growth that we are seeing in focusing on AI and accelerated computing. I believe more of it is just about sheer volume of companies that are really interested in taking this next step and really leveraging generative AI for all the work that they do. That’s really what it’s about.”

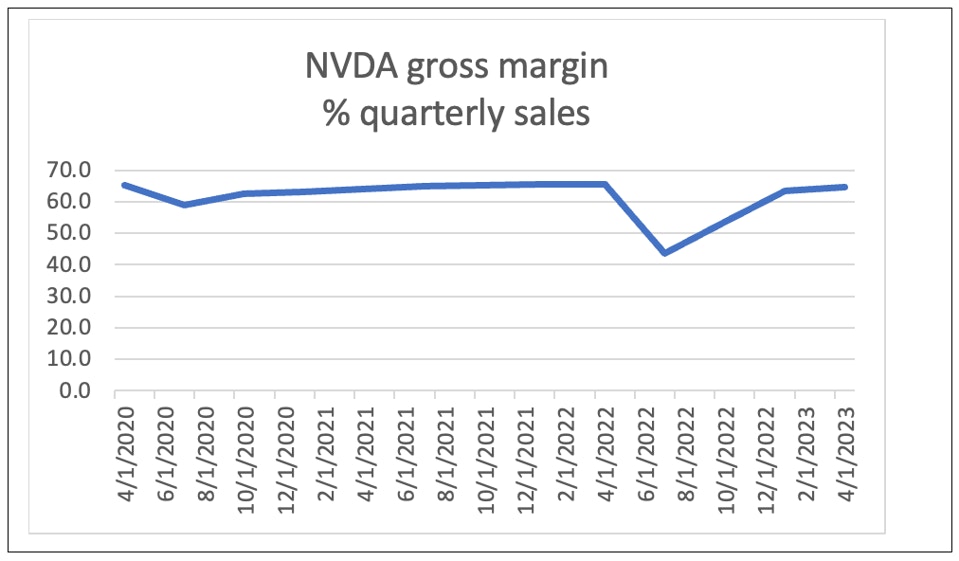

CFO Kress’s answer is important because it indicates further potential for margins to expand not just from pricing. On a three-year basis, Nvidia has just returned to its prior peak of about 65% gross margins (reported). Given the positive pricing and unit demand dynamics, the new normal is perhaps between 65% and 70% gross margins:

Source: I/O FUND

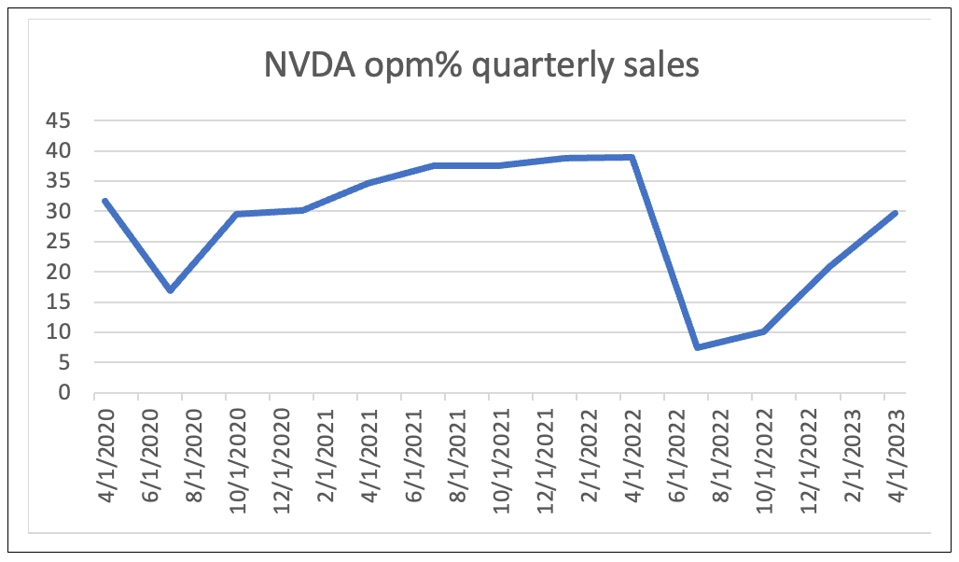

Operating Margin

Given CFO Kress’s comments that it’s both pricing and units, this suggests that there is upside to reported operating margins that still have yet to return to the prior 3-yr peak.

Source: I/O FUND

Net margin

A similar below-peak picture can be seen in reported net margins.

Source: I/O FUND

We likely won’t get answers to all these medium term questions in Q2, but it will help us to assess what the margin potential is in the upcoming quarters.

Outlook for Gaming for FY2024

Gaming is still an important segment and contributed 31% to Q1FY24 sales and has been impacted by the weaker consumer. It appears that gaming bottom in Q1. Although gaming sales were down 38% y/y, they were positive 22% q/q. Critically, in the Q1 call Nvidia stated “We believe the channel inventory correction is behind us.

A resumption of growth in gaming is important for the overall sales and profitability and is probably not quite reflected in consensus estimates. It provides another lever for Nvidia to exceed their Q2 sales guidance and Q3 consensus sales estimates. So, we will look for continued signs of improvement and what growth rate is sustainable.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Longer-Term View:

For more information on Nvidia’s Bull thesis, reference “Nvidia Will Still Surpass Apple’s Valuation” and also “Why Nvidia will Surpass Apple’s Valuation.”

Visually, you can see how Nvidia breaks down the $1 trillion opportunity. This was taken from the October 2022 investor presentation.

Source: NVIDIA

How We Plan to Manage our Position

By Knox Ridley, Portfolio Manager

With the cash we raised throughout 2022, NVDA was the primary target of deploying some of this cash once our analysis signaled a bottom was in place. The below is a real-time trade notification we sent to our stock research members on the October 13th.

Source: I/O FUND

The above alert was one out of nine alerts we sent out from 2021 – 2022 to buy NVDA below $200. However, since February of 2023, we have been systematically taking gains at key levels based on technical and macro warnings, while still holding it as our top position today.

In our last free Nvidia report, we identified the $405-$395 region as strong support. This was the buy zone we set up in advance, and were able to grab shares around the $410 region after it bounced from $403. Also, in our last report, we stressed the importance of last quarter’s earnings gap. For those that are not familiar, I’m referring to the rather large gap between closing price before their report and the opening price after the report.

Source: I/O FUND

Gaps are very important markers within price trends, and have many uses. For our purpose, the question we need to answer – is this gap a breakaway gap (the halfway point in a trend), or is it an exhaustion gap (the final bullish push before rolling over)?

There are two general Elliott Wave counts I’m using that represent both of these gap possibilities.

- Blue – this count has the 2022 bear market as the first leg in a large degree correction. That would make 2023 the corrective leg, with the final drop on the horizon, which would likely retest the October lows.

- Red – this count has us in a 4th wave correction within a larger 5 wave uptrend. This would make this current dip a buying opportunity as we push towards the $560-$590 region next.

Source: I/O FUND

The lowest I would allow this correction to go and still keep the red count valid would be the $340 region. If we break below $340, then the odds shift that the gap from Nvidia’s last earnings call was in fact an exhaustion gap. Our next move would be to set up downward targets to accumulate Nvidia for the long haul.

Micro Analysis

Another point worth mentioning is that the structure of the final leg in a corrective pattern (the C wave) is always a 5 wave drop. Furthermore, these patterns are fractal, so a small 5 wave patterns will morph into a larger one, which turns into an even bigger one. So, if we analyze the structure of the initial drop, we can get clues on what is playing out.

Source: I/O FUND

This pattern appears to be an overlapping and corrective pattern, not a 5-wave pattern. If price can definitely break above the July high at $480, then the odds will shift heavily towards the red count as we push to new highs. The only chance the blue count will have is if we break $405 to make afresh low. If this happens, and it is followed by a 3 wave correction, then the odds will shift towards the blue count, allowing investors ample time to better risk manage this position.

If you own Nvidia stock, or are looking to own NVDA, we encourage you to attend our weekly premium webinars, held every Thursday at 4:30 pm EST. Next week, we will discuss NVDA, as well as a handful of other AI plays – what our targets are, where we plan to buy as well as take gains.

Recommended Reading:

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i