Semiconductor Stocks: Q2 Sector Overview

July 18, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jul 13, 2023,07:05pm EDT

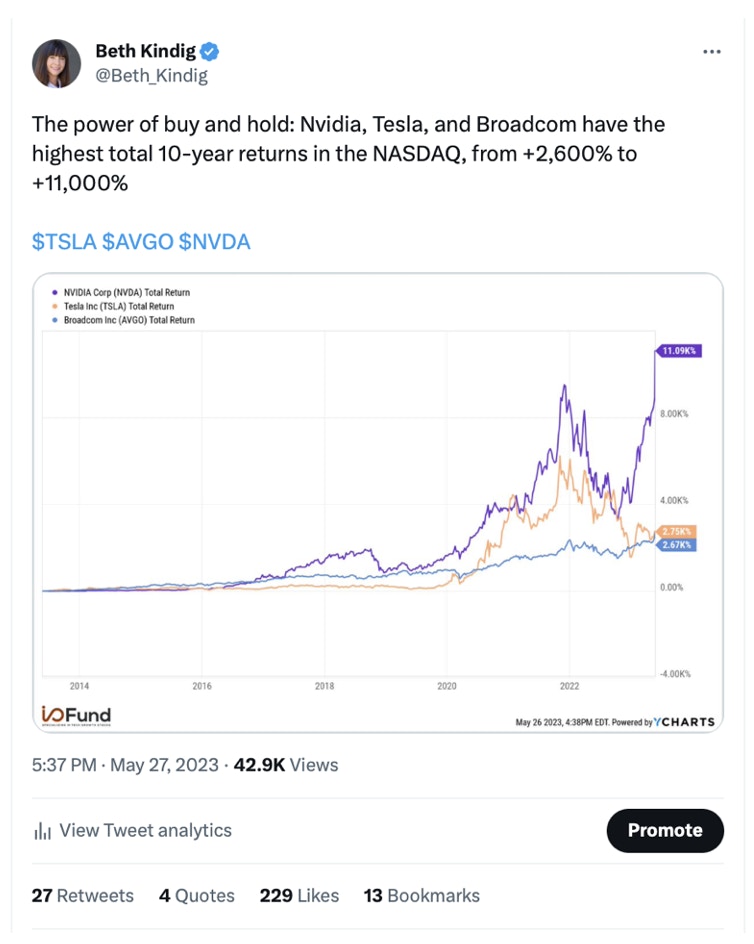

Semiconductors are the common denominator across the burgeoning technology trends of the next decade. Artificial Intelligence, 5G, high-performance computing, Internet-of-Things, gaming, electric vehicles, and robotics, among others, all require semiconductors to power them. These trends make semiconductor stocks an ideal investment and perhaps the most important space for tech investors to monitor.

For years now, we have published on semiconductors as leaders in tech– even when cloud, e-commerce, connected TV and others were more favored. In fact, we have been pointing out quite clearly that semiconductors are the sector that has provided the most returns in the past decade.

Source: Beth Kindig

Below, we update our semiconductor sector analysis to look at which companies have performed well in the most recent quarter, and also which companies stand out on a forward-basis with revenue growth estimates, profits, cash flows, earnings surprises, and we also look into management insights.

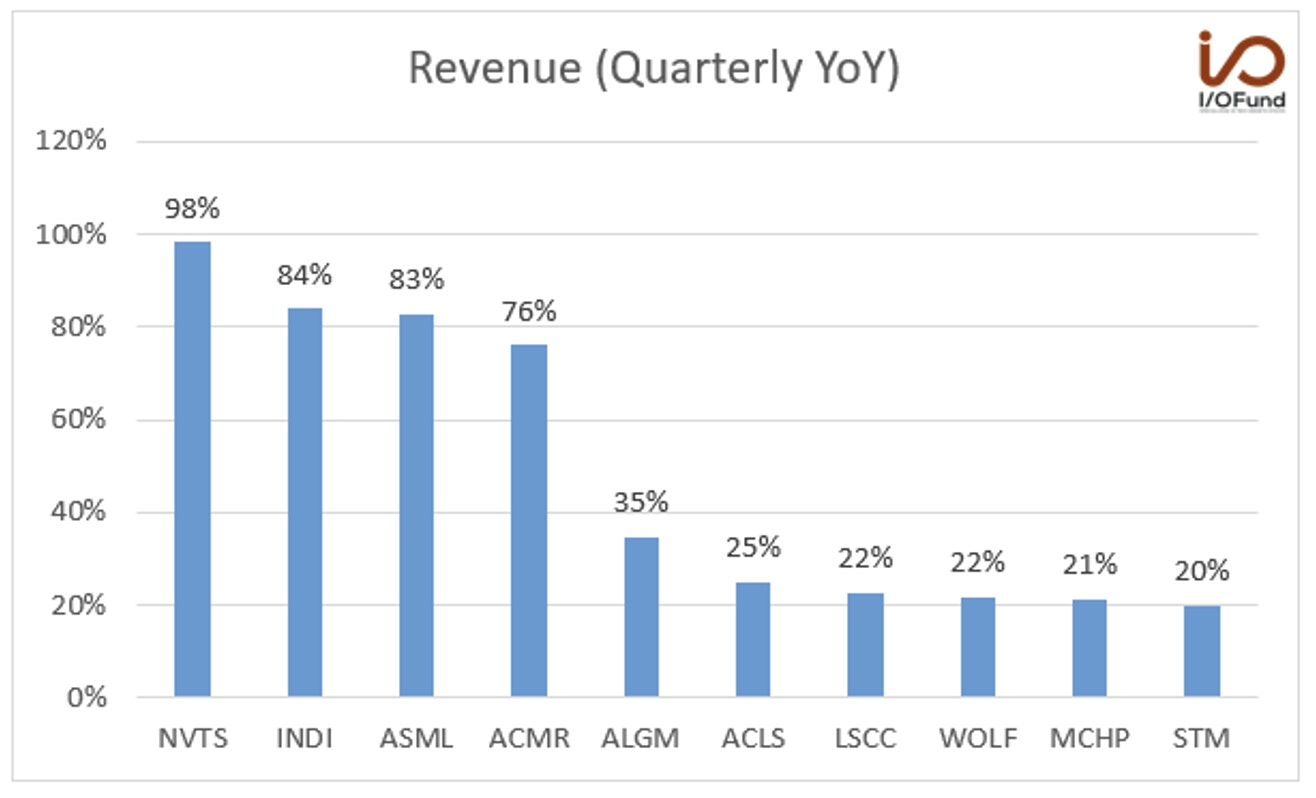

Top Semiconductor Stocks with the highest revenue growth rates in Q1

Source: YCHARTS

Navitas Semiconductor had the highest revenue growth among semiconductor stocks in the recent quarter. The company’s revenue grew by 98% YoY to $13.4 million. Management’s revenue guidance for next quarter is $16 million to $17 million, representing YoY growth of 92% at the mid-point.

Ron Shelton, CFO of the company, said in the earnings call, “Our guidance is based on robust strength in EV, solar, appliance/industrial, and the beginnings of a recovery in the mobile and consumer market, all further evidenced by a more than 50% increase in backlog during the quarter.”

The company acquired GeneSiC Semiconductor in August last year and helped to diversify into the fast-growing Silicon Carbide market. Navitas has a strong pipeline of $760 million with $432 million of this recognized by fiscal year 2026.

Analysts expect revenue in the next quarter to grow 92% YoY to $16.51 million and robust revenue growth close to or over 100% on a YoY basis for the next several quarters. The risk to consider is that the bottom line is weak. Analysts don’t expect Navitas to be profitable on an adjusted basis until Q1 2025 and GAAP profitable roughly around 2027.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

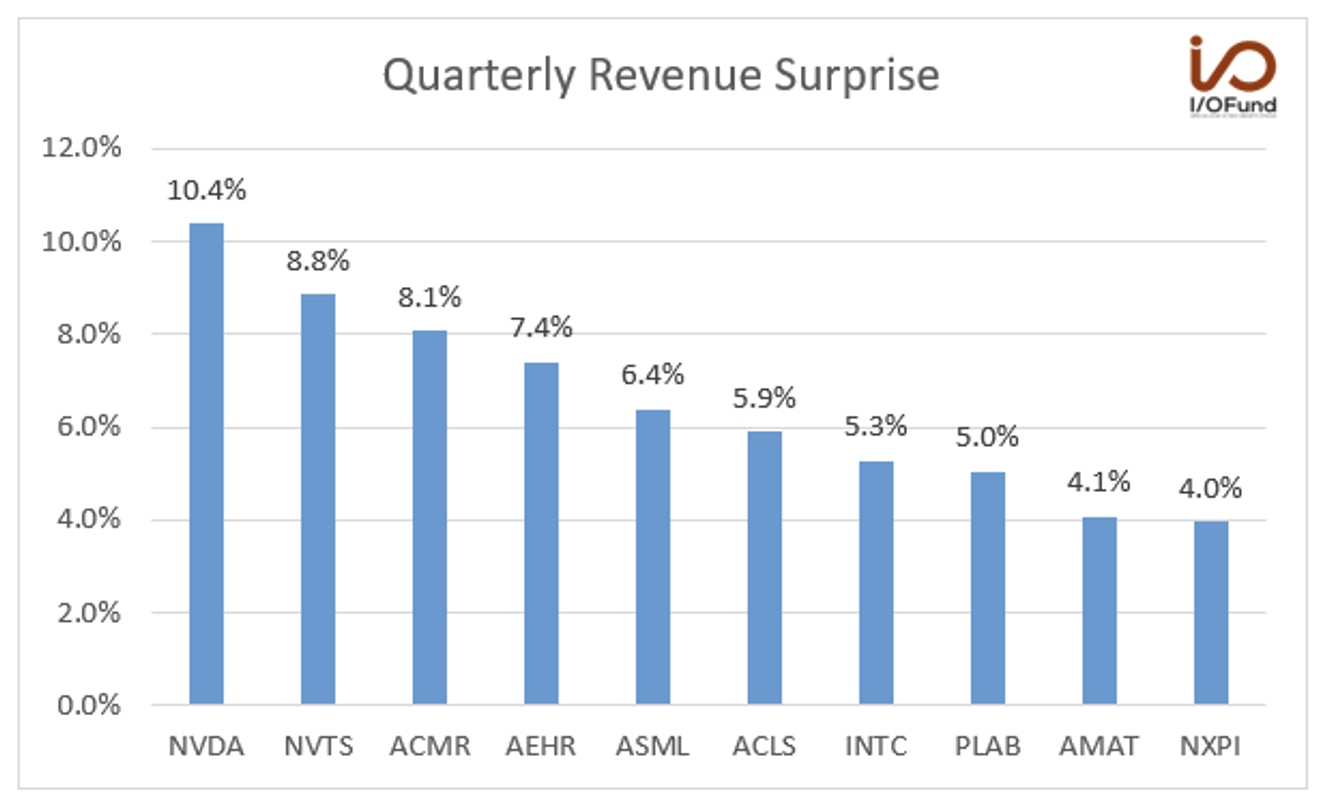

Semi Stocks Q1 Revenue Surprise

Source: YCHARTS

Nvidia crushed analysts’ revenue estimates by 10.4%. The company’s revenue declined by (13%) YoY and is up 19% QoQ to $7.19 billion.

The strong sequential growth was led by record data center revenue, primarily helped by accelerated computing. The company’s CFO, Colette Kress, said in the earnings call, “Generative AI drove significant upside in demand for our products, creating opportunities and broad-based global growth across our markets.” Gaming and professional visualization segments also witnessed improvement from the inventory correction.

If Nvidia is adding roughly $4 billion in revenue, primarily driven by the data center, then Q2’s data center growth will accelerate to an incredible 100% growth rate, up from $3.8 billion in the year ago quarter. It also means the data center will roughly double from the first quarter (sequentially) as the segment was $4.28B in the current quarter.

Put another way, this means Nvidia’s data center segment in the upcoming quarter will be as large as the company’s entire revenue this quarter – if we assume $7.75B in the data center compared to $7.2B total revenue this quarter.

We have highlighted in the past that AI will add $15 trillion to GDP compared to mobile’s $4.4 trillion. Mobile brought us three FAANGs: Apple, Google, and Facebook. It has been my stance for years that AI will bring us a new set of FAANGs, one of which will be Nvidia.

The company’s revenue guidance for the next quarter is $11 billion, representing YoY growth of 64% at the midpoint. The Q2 guidance was 53% higher than consensus. The historic beat in estimates is driven by data center revenue doubling from $4.28 billion in revenue in Q1 to $8 billion in revenue in Q2.

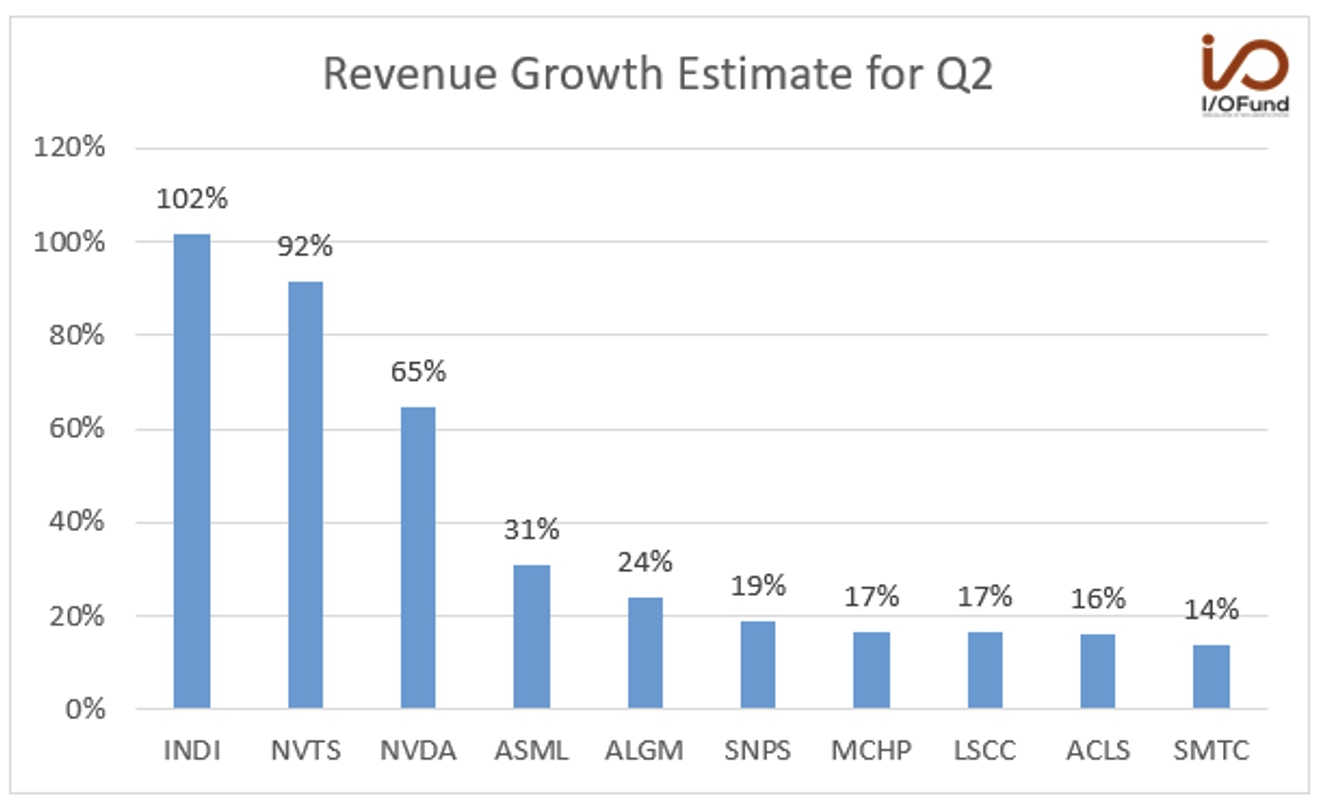

Semiconductor Stocks Q2 Revenue Growth Estimates

Source: YCHARTS

Indie Semiconductor has the highest expected revenue growth rate for Q2. The company’s recent quarter revenue grew by 84% YoY to $40.5 million. The company has guided for 102% YoY revenue growth in the next quarter.

Analysts expect revenue to grow 102% YoY to $51.97 million. The company is benefiting from growth trends in advanced-driver assistance systems (ADAS) and electric vehicles. indie has a large Serviceable Addressable Market (SAM) of $56 billion by 2028. The company is on track to be profitable on an adjusted basis this year.

Donald McClymont, indie’s co-founder and CEO, said, “Our growth trajectory reflects continued design win momentum spanning ADAS, vehicle electrification and user experience applications. At the same time, our deeper R&D investments and targeted acquisitions are beginning to contribute, enabling us to sharply outpace our peer group. Accordingly, today we are even better positioned to capitalize on the 2025 Autotech market opportunity of $42 billion.”

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

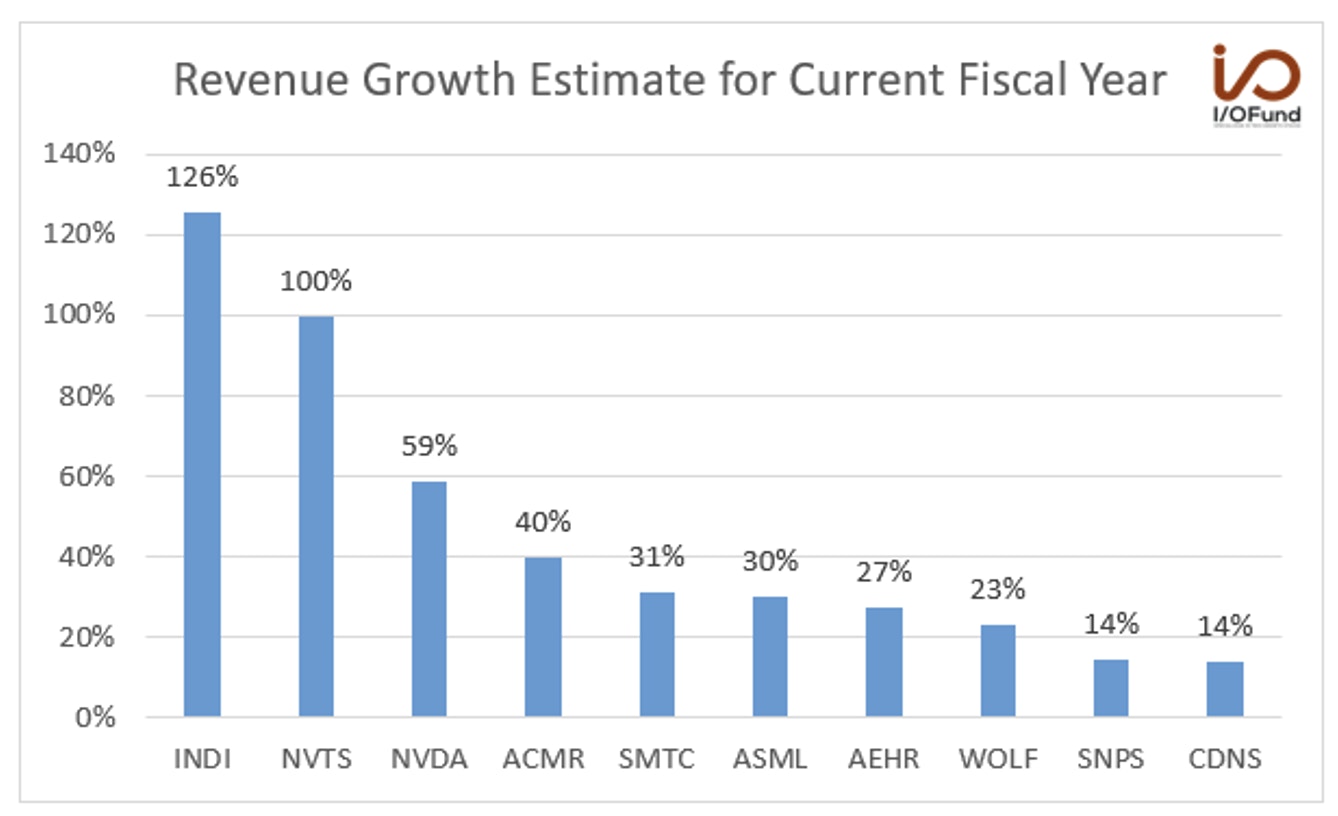

Revenue Growth Estimates for Current Fiscal Year: Navitas and indie Semiconductor

Source: YCHARTS

For the current fiscal year, analysts expect indie Semiconductor to have the highest revenue growth estimate among the semiconductor stocks. It is followed by Navitas Semiconductor, which analysts expect to grow 100%. Among more established players, Nvidia leads and is expected to grow by 59%.

Semiconductor equipment provider ACM Research ranks fourth and is expected to grow 40% in the current fiscal year. The company’s revenue in the recent quarter grew by 76% YoY to $74.3 million. The management’s FY23 revenue guidance is in the range of $515 million to $585 million, representing YoY growth of 41% at the midpoint.

Needham Analyst Quinn Bolton mentioned in his note, “As the fastest growing SemiCap stock in our coverage with ~$400MM in cash and very little debt, we believe a 12.5x multiple is more than fair. The stock is currently receiving little attention from investors due to its high-exposure to China. However, we believe this ACMR sentiment will change over time as its growth proves too difficult to ignore.”

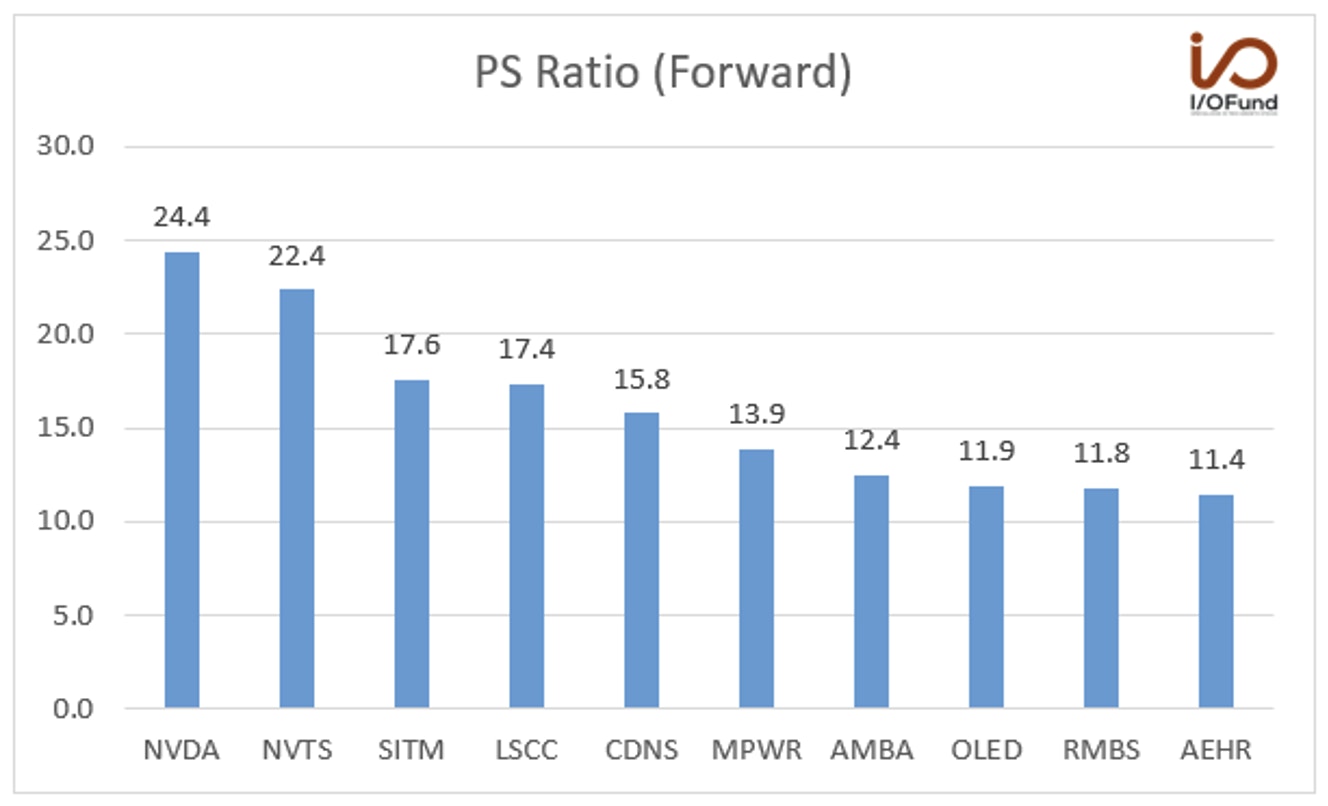

Semiconductor Top Line Valuations

Source: YCHARTS

Nvidia has the highest forward P/S ratio of 24.4 among the semiconductor stocks. The company has commanded a premium valuation due to its unrivaled position on GPUs. It is followed by Navitas, which has a forward P/S ratio of 22.4.

Per our analysis, Navitas is expected to have strong revenue growth in the next several quarters.

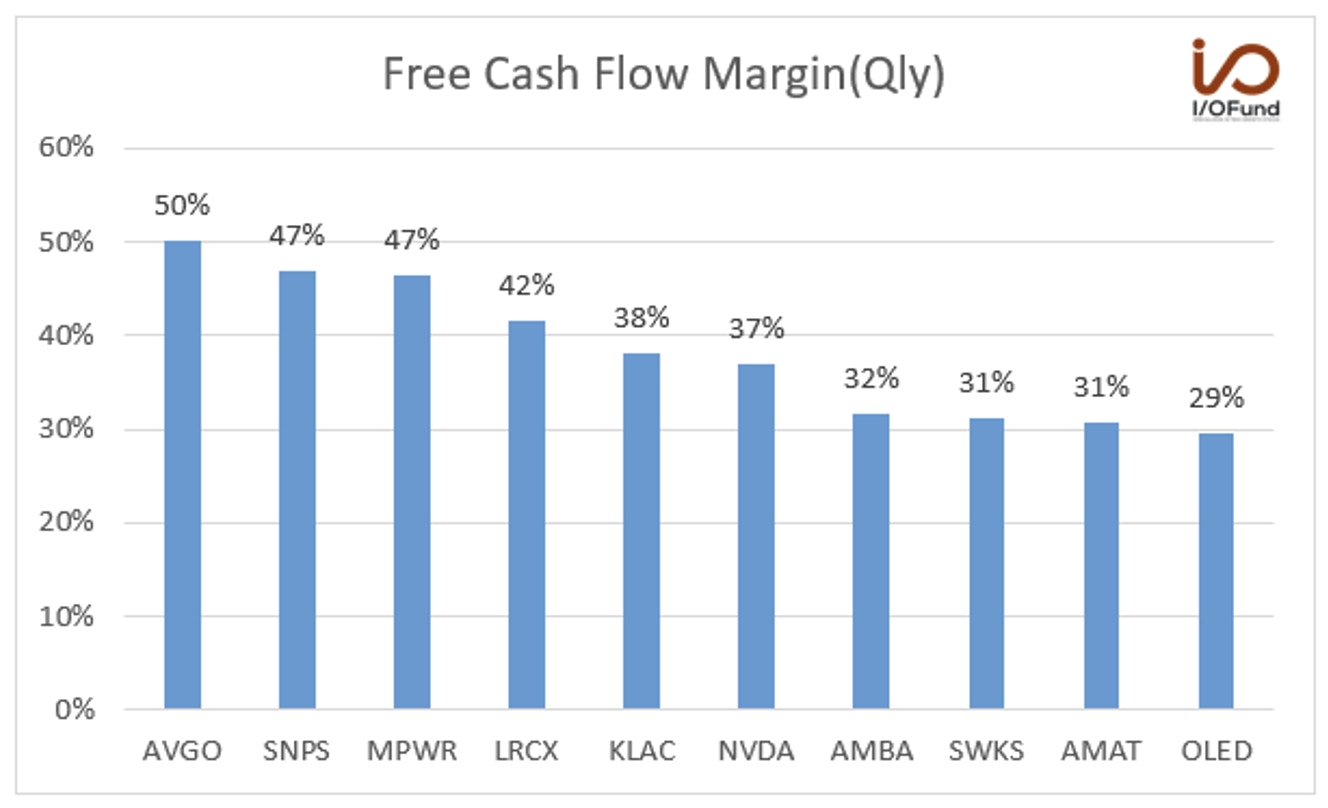

Free Cash Flow Margin

Source: YCHARTS

The majority of semiconductor stocks have positive free cash flow margins. Among the semiconductor stocks we track, 16 companies have more than 20% free cash flow margin. During times of macro uncertainty, stocks with strong free cash flows are considered a safer bet.

Broadcom leads the semiconductor sector with a free cash flow margin of 50%, followed by 47% for Synopsys and 47% for Monolithic Power Systems. Broadcom’s free cash flow in the recent quarter grew by 5% YoY to $4.4 billion. The management also expects cash flows to be strong in the next quarter.

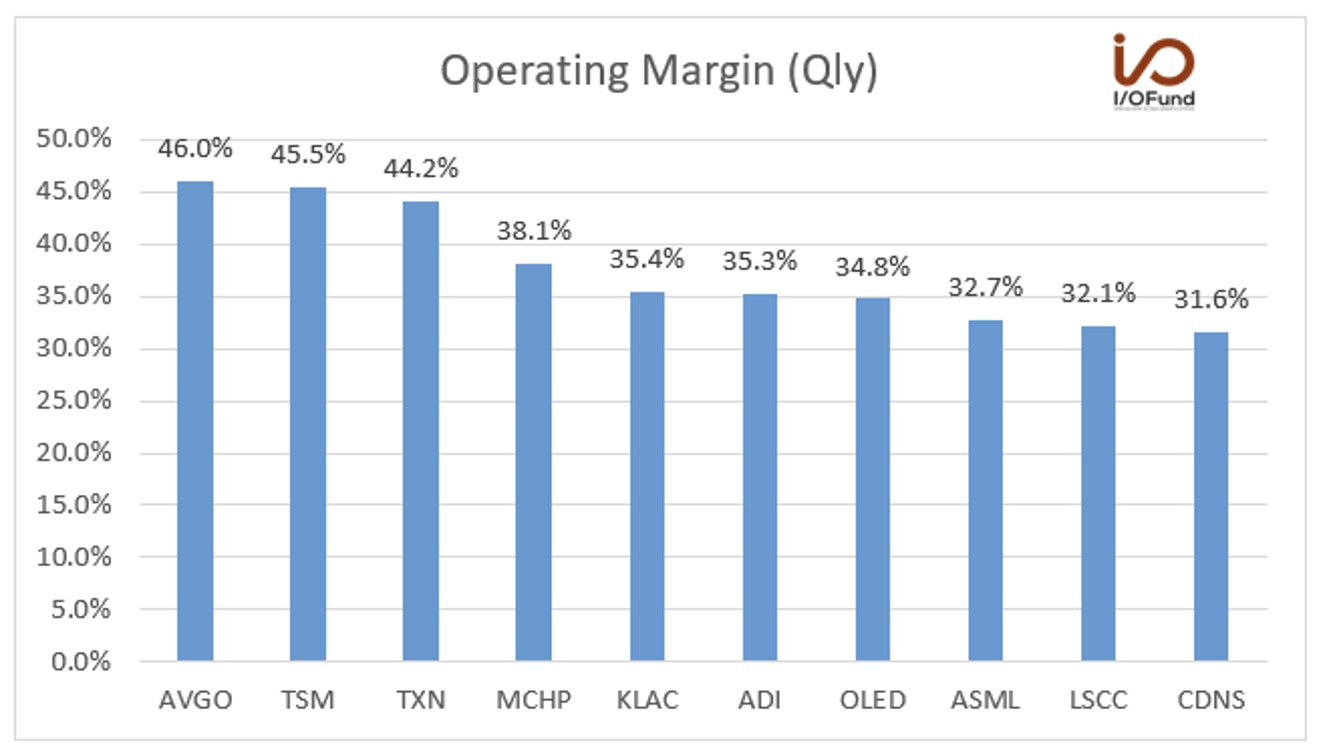

Operating Margin

Source: YCHARTS

Broadcom leads the semiconductor stocks with an operating margin of 46%, followed by 45.5% for Taiwan Semiconductor Manufacturing and 44.2% for Texas Instruments.

TSM’s operating margin of 45.5% was higher than management’s guidance of 41.5% to 43.5%. The company’s cost control efforts led to a reduction in operating expenses.

Wendell Huang, CFO of the company, said in the earnings call, “Total operating expenses accounted for 10.8% of net revenue, which is lower than the 12% implied in our first quarter guidance mainly due to stringent expense control and lower employee profit sharing”. Management guidance for Q2 is 39.5% to 41.5%.

Due to its leadership position in manufacturing advanced chips, TSM is able to negotiate better prices with its customers. Cost improvements also help the company to maintain strong margins.

Conclusion:

Nvidia is a well-known semiconductor stock at the moment, yet there are others in the semiconductor space that are outperforming, as well. Broadcom and Taiwan Semiconductor continue to be defensive stocks with strong bottom lines. Navitas and indie Semiconductor are high beta stocks that are putting up nearly triple digit growth (notably, their margins are in the red until they reach scale).

Recommended Reading:

More To Explore

Newsletter

TSM Stock and the AI Bubble: 40%+ AI Accelerator Growth Fuels the Valuation Debate

Taiwan Semiconductor (NYSE: TSM) recently announced fiscal Q3 earnings, stating its longer-term AI revenue outlook is stronger than anticipated. The company reported record Q3 revenue of $33.1 billion

Micron Stock Up 120% YTD: What the HBM Memory Leader Plans for 2026

Micron’s stock is up 120% YTD – or 3X more YTD than AI heavyweight Nvidia. Recently, the high-bandwidth memory content that Micron supplies has increased 3.5X between GPU generations, leading to a qui

Palantir Stock Forecast 2025: Can PLTR Justify Its High Valuation?

Palantir leads the AI software pack in terms of strong earnings reports this past quarter as the company achieved significant milestones, the most impressive being US commercial revenue grew 93% YoY a

CoreWeave Stock Soars 200% Since IPO — Can It Defy the Odds?

CoreWeave saw muted price action following the latest earnings report; yet the soft price action is rare for the AI darling. The company went public in March and has stood out as the premier IPO among

Meta Stock Emerges as a Strong Mag 7 AI Leader

The AI frenzy has investors fixated on revenue growth as proof of returns on AI spending that can be as high as $100 billion per year, depending on the company. Yet, Meta is proving that a stronger si

Updated Nvidia Stock Price Target - AI “Bubble” Narrative Ignores Re-Acceleration in Big Tech Capex

In the analysis below, my firm crunched the hard data on Q2 capex numbers and what is coming down the pipe for Q3. If you are an AI investor like we are, this is an analysis you will not want to miss

Oracle Soars After Earnings – Is ORCL Stock Still a Buy?

The market is clearly excited about this report, and for good reason. Remaining performance obligations (RPO) grew 359% YoY with cloud RPO growing “nearly 500%” on top of 83% growth last year. Another

Nvidia Stock Forecast: The Path to $6 Trillion

Two years ago, the April 2023 quarter delivered a historic 18% beat, followed by an even bigger 30% beat in July 2023. Compare that to the most recent quarter ending July 2025 — just a 4% beat, the sm

Bitcoin Bull Market Guide: When to Hold, Trim, or Re-Enter (Webinar)

Our track record including a more recent 600% move in Bitcoin is not the product of hype but of a systematic framework—one built on technical analysis, on-chain metrics, and a close watch on global li

Reddit Stock Blows the Doors Off - Can it Last?

Reddit’s stock has surged 62% in one month, easily placing the company’s earnings report as one of the best to come out of the tech sector this quarter. The world’s leading forum site has only 416 mil