The Strongest Cybersecurity Stocks In Q3

December 04, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Nov 30, 2023,09:40pm EST

Cybersecurity stocks have performed well in 2023, rising about +26.5% YTD, with the security backdrop boosted by an increase in data breaches and ransomware. Quarterly spending has increased approximately +12.7% YoY to ~$37.6 billion through the first half of the year, although commentary from sector leaders Fortinet and Palo Alto raised some concerns about spend optimization, with billings forecasts from the two weaker than expected.

Despite beating on the top and bottom lines, Zscaler provided flat billings guidance while revenue growth is set to slow. CrowdStrike was GAAP profitable from operations for the first time ever as net new ARR reached a record, but billings and ARR growth both decelerated.

Cybersecurity Market Growth Slows in Q2

Zscaler and CrowdStrike reported their October quarters this week with both providing important commentary that the macro environment is tougher than usual. CrowdStrike’s management said that buyers still remain cautious since the “macroenvironment remains challenging with continued increased budget scrutiny.” Zscaler said that while the “global macro environment remains challenging, and customers continue to scrutinize large deals, … customer sentiment seems to be stabilizing.”

Looking back at the cybersecurity market through Q2 offers a bit of color on those broader trends impacting growth this year. The market registered a third straight quarterly deceleration in Q2, per Canalys estimates, as the global market recorded +11.6% YoY growth to $19.0 billion.

This marked a slight deceleration from the +12.5% growth in Q1 to $18.6 billion, and a sharper deceleration from the +15.8% growth rate seen in 2022, as the cybersecurity market topped $71 billion for the year.

Source: CANALYS

Growth in North America remained resilient at +12.6% YoY in Q2, the bellwether of the market considering it accounts for more than half of total spending. Latin America and EMEA growth remained in the double digits, though both decreased approximately 180 to 210 bp sequentially. APAC growth saw the largest slowdown, from +10.7% YoY in Q1 to +8.8% YoY in Q2.

Headwinds Remain in Play in Q3

Budget cuts, consolidation, and optimization are some of the trends at play in the cybersecurity market that are pulling 2023’s growth rates lower. Microsoft CEO Satya Nadella said in January during its fiscal Q2 earnings call that customers were “consolidating on our security stack, in order to reduce risk, complexity and cost.”

CrowdStrike CEO George Kurtz echoed Nadella’s view in the company’s Q1 earnings call in March that customers “want to reduce cost and headcount, reduce the number of point products and agents, reduce complexity and simplify operations.”

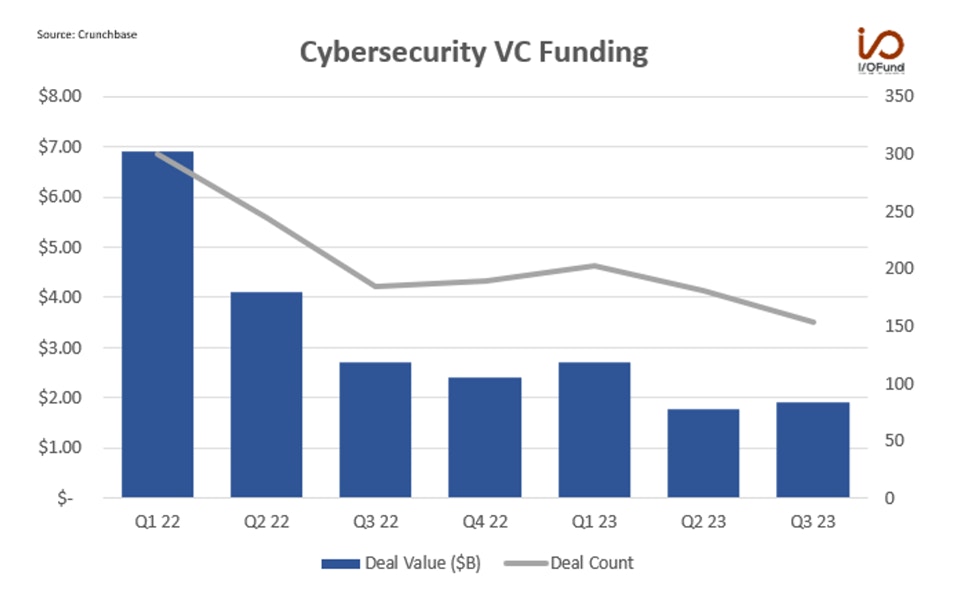

Venture capital funding deals and deal value also reflect this challenging environment persisting through Q3. According to Crunchbase, deal count declined just over (-15%) from Q2 to 153. Although deal value was marginally higher at $1.9 billion compared to ~$1.8 billion in Q2, it was about (-30%) lower YoY as large late-stage deals faded. VC funding has totaled just $6.4 billion YTD, on track to mark the lowest level of funding for cybersecurity startups since 2019, which totaled $8.8 billion.

Source: CRUNCHBASE

Despite such cost and complexity concerns, companies are still committed to protecting data and operations. It’s this point that will drive long-term growth of the industry in the face of these near-term headwinds: there will always be more data to protect.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

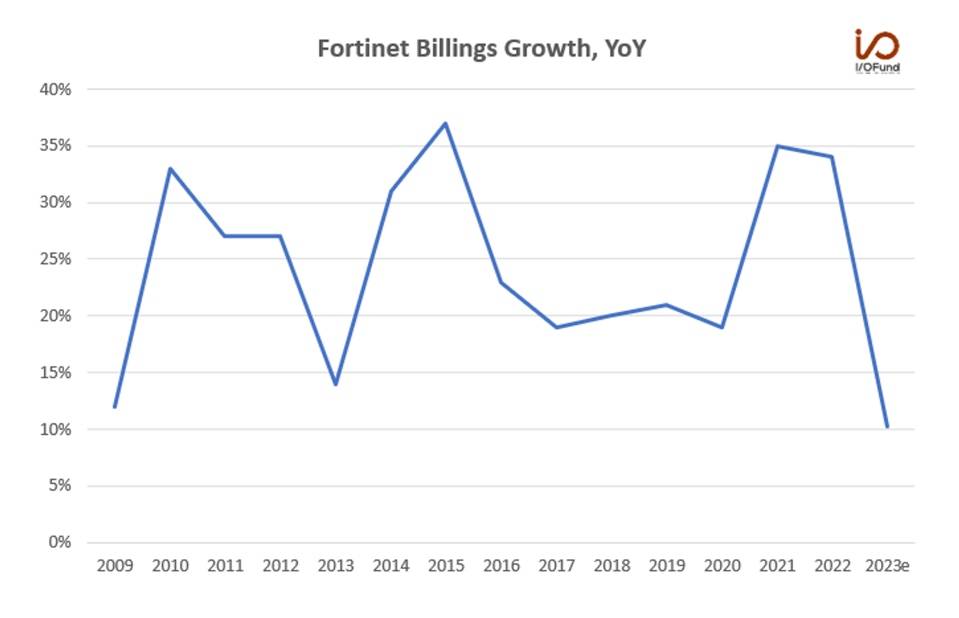

Fortinet: Q4 Guidance Soft, Billings to Decline YoY

Fortinet declined (-12.4%) following its Q3 earnings report for three key reasons: Q3 revenues marginally missed estimates, Q4 revenue guide was below consensus, and most importantly, Fortinet is projecting a YoY decline in net billings.

Fortinet reported revenues of $1.33 billion in Q3, which missed expectations by just $20 million. For Q4, Fortinet guided revenues $80 million lower at midpoint than the consensus estimate of $1.49 billion.

Q4 billings were projected to be between $1.56 to $1.70 billion, representing a YoY decline of ~(1%) to (9%). Management’s transition to SASE and security operations, and challenging network comps, are some of the factors behind the revenue slowdown with Fortinet seeing “modest” revenue growth for the next few quarters.

Source: I/O FUND

Fortinet’s billings slowdown and the lowered revenue forecast is a concern as 2023 would mark Fortinet’s slowest billings growth since its IPO in 2009. Growth is estimated at just +10.2% YoY at the $6.165 billion midpoint. It’s also a significant slowdown from the +34% and +35% billings growth seen in 2022 and 2021. Management said the growth slowdown in Q3 stemmed from “1 month shorter contract duration and importantly, lackluster appliance demand.”

A slowdown in product revenue growth is likely a driving factor behind the lowered revenue forecast for 2023. Product revenue is forecast to increase only +9% YoY to $1.935 billion – this is well below 2022’s +42% growth, 2021’s +37% growth, and its +23.7% average growth rate since 2009. CEO Ken Xie said that “the Secure Networking market is experiencing slower growth as product demand returns to normal levels following two years of elevated growth.” He added that “building and product revenue fell below our expectation” due to that slowdown in Secure Networking.

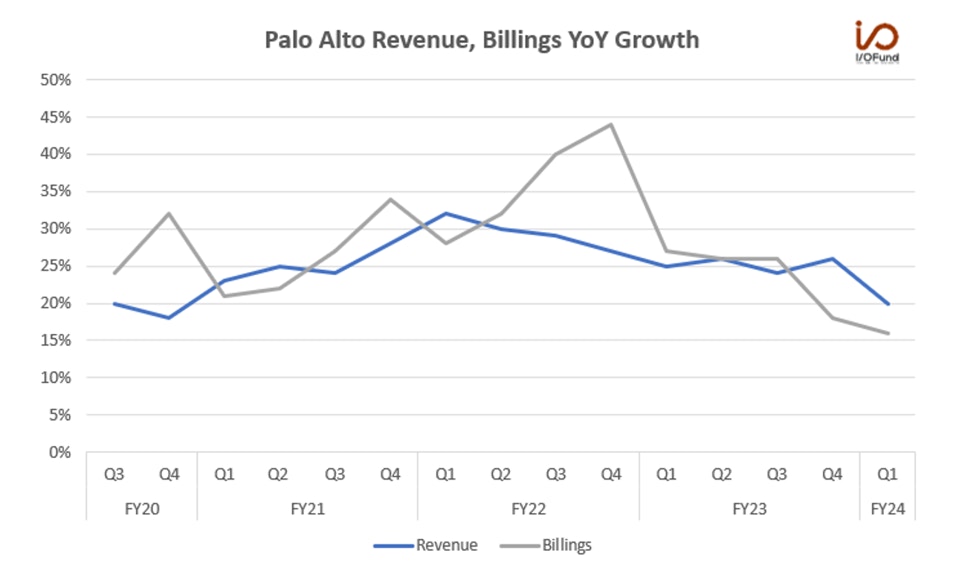

Palo Alto: Billings Weaker than Expected, Underlying Metrics Strong

Palo Alto shares fell (-5.4%) following its fiscal Q1 earnings report, but have since gained more than +14% to rise to new highs. The initial negative reaction stemmed from a lowered billings forecast as well as hints that revenue growth is slowing below 20%, but other underlying metrics remained strong.

Palo Alto reported +20% YoY revenue growth to $1.88 billion and +16% YoY billings growth to $2.02 billion, which came in below its prior outlook for $2.05 to $2.08 billion in the October quarter. This miss is amplifying concerns that revenue and billings growth is decelerating — revenue growth was at the lowest level since fiscal Q4 2020, while billings growth was at the lowest level in more than four years and marks a second quarter with growth below +20%.

Source: I/O FUND

For the full year, Palo Alto lowered its billing forecast to $10.7 to $10.8 billion, from a prior view of $10.9 to $11.0 billion. This correlates to YoY growth of +16% to +17%, roughly in line with the recent quarter’s +16% growth rate. Palo Alto cited volatility in contract duration, increased financing demand, and increased demand for deferred billings plans for the lowered forecast. CFO Dipak Golechha said that the company “saw the rising cost of money have an important and incremental impact on customer behavior in [fiscal] Q1.” Similar to Fortinet, Palo Alto saw minimal growth in product revenue, at just +3% YoY, with the majority of revenue growth driven by service revenue, +25% YoY.

Aside from that, Palo Alto had multiple underlying strengths in the report, especially with its next-gen offerings. Next-Gen Security ARR increased +53% YoY to $3.23 billion, and SASE ARR increased +60% YoY. Palo Alto saw very strong growth in multi-module customers, with +155% YoY growth in those adopting 5+ modules, and +59% YoY growth in those adopting 3+. XSIAM’s pipeline exceeded $1 billion, with more than $500 million of that pipeline added in Q1.

Zscaler: Billings Guide Unchanged, Revenue Growth May Slow

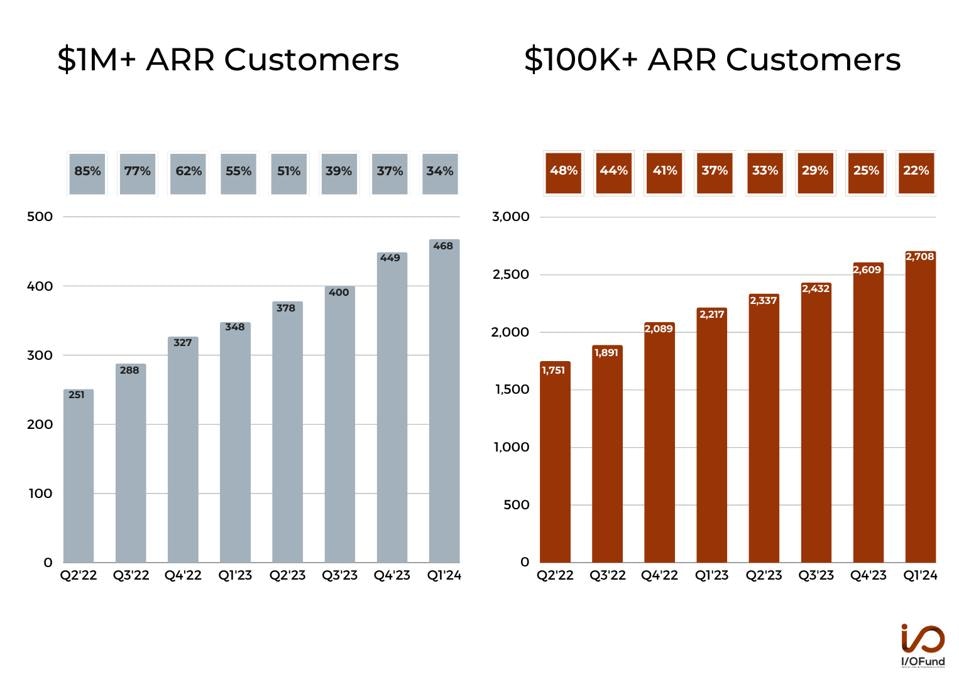

Zscaler maintained its billing guide for the full year, although revenue and EPS both came in ahead of expectations in its fiscal Q1. Large customer growth continued to slow, while fiscal Q2’s guide hinted at a possible deceleration in revenue growth.

Zscaler reported $497 million in revenue, +40% YoY, which handily beat expectations and the company’s guidance for +33% YoY growth to $473 million in revenue. While it did post +131% YoY growth in adjusted EPS to $0.67 and a surge in free cash flow, Zscaler remains unprofitable on a GAAP basis.

GAAP operating loss improved 33% YoY to ($46 million), while GAAP operating margin improved 10 percentage points to (9%). At its scale of more than $2 billion in annual revenue, it’s likely the market will want Zscaler to soon shift to operating profitability, which could be tough at the moment given that sales, marketing and R&D accounted for ~98.8% of gross profit in Q1. SBC also remained high at $129.1 million, or ~26% of revenue.

Billings growth remained strong, at +34% YoY to $456.6 million. However, Zscaler did not raise its full-year billings outlook as it tends to do, even if only by a few million; its outlook remained unchanged at +24% to +26% YoY growth, or $2.52 to $2.56 billion. That outlook suggests that billings growth will decelerate through the remainder of the fiscal year.

Fiscal Q2’s revenue guide also hinted at some early signs of revenue deceleration, with the $506 million guide pointing to YoY growth of approximately +30.5%. Fiscal 2024’s guide calls for +29.5% YoY growth at midpoint to $2.095 billion, again indicating that revenue growth in fiscal Q3 and Q4 is likely to slow to the mid to high-20% range.

Source: I/O FUND

Growth in large customers of over $1M in ARR has slowed significantly by 21 points over the past year, from 55% growth down to 34%. Growth in $100K+ ARR customers has also slowed from 37% to 22%.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

CrowdStrike: Net New ARR Rises to Record, But Billings Decelerate

CrowdStrike beat on the top and bottom lines and guided fiscal Q4 marginally above consensus. The report in itself was fairly strong, as net new ARR rose to a record and CrowdStrike recorded its first-ever quarter with positive operating income. However, ARR growth and billings growth both decelerated, similar to peers who are also seeing decelerating billings. Management added that “buyers are still cautious” as the “macroenvironment remains challenging with continued increased budget scrutiny.”

Source: I/O FUND

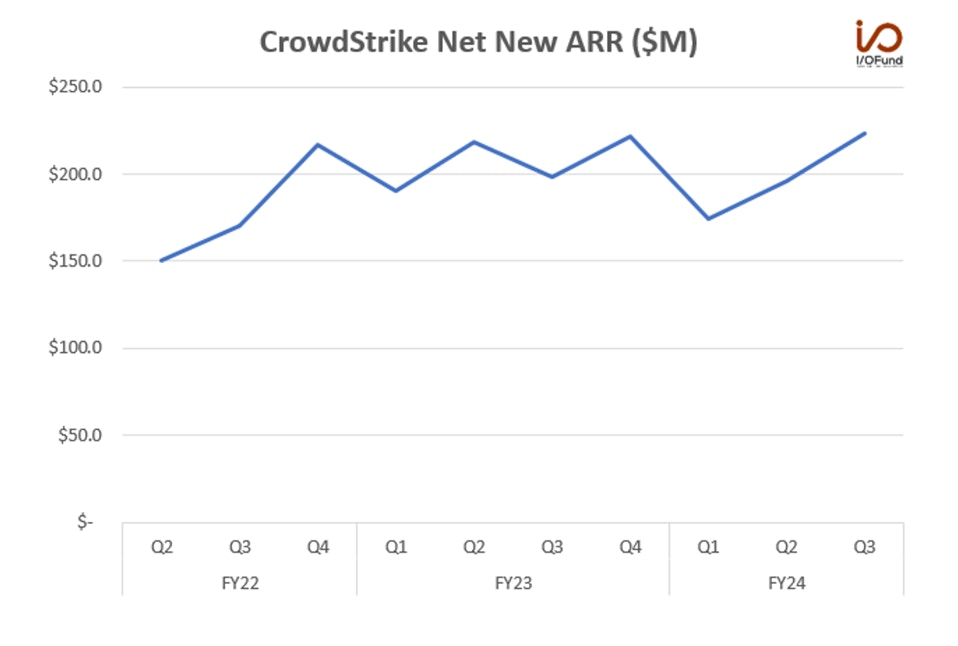

Net new ARR rebounded to a record $223.1 million, +12.6% YoY, a strong recovery from Q1 and setting the stage for another possible record to close out FY24. With this rebound in net new ARR, CrowdStrike’s ARR topped $3 billion for the first time, reaching $3.15 billion in fiscal Q3. CrowdStrike emphasized that it is the “fastest and only pure play cybersecurity software vendor in history” to surpass the $3 billion ARR milestone.

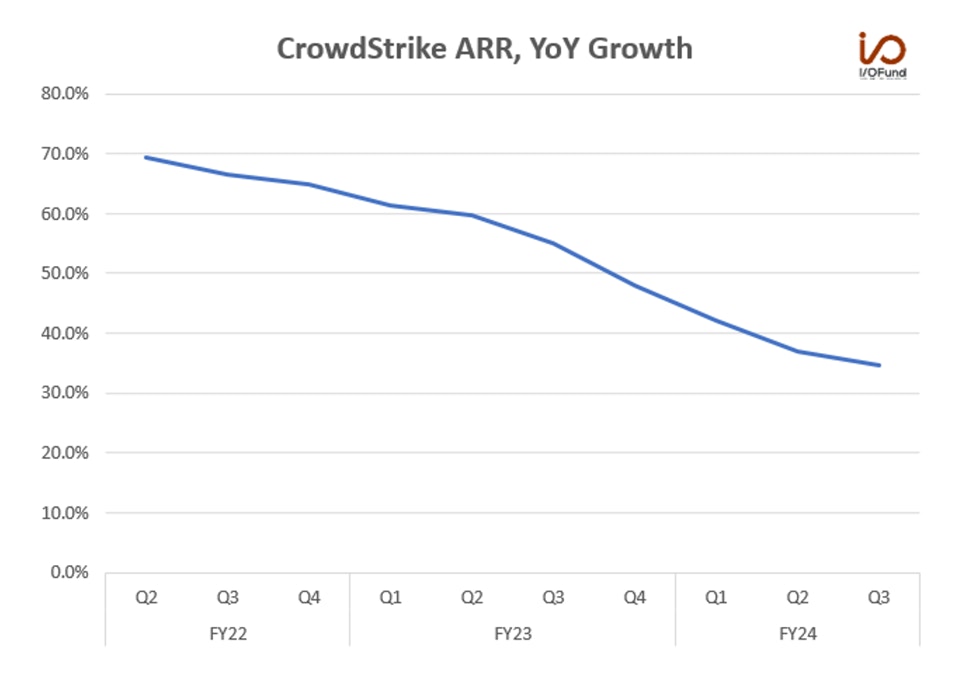

However, ARR growth is still decelerating, as is billings growth. ARR growth in fiscal Q3 was +34.6% YoY, a slight deceleration from Q2’s +36.9% YoY growth rate and a sharper deceleration from the +55% YoY growth rate from fiscal Q3 last year. What’s important is that CrowdStrike soon shows ARR bottoming and stabilizing, instead of decelerating further into the +20% range or even the high teens.

Source: I/O FUND

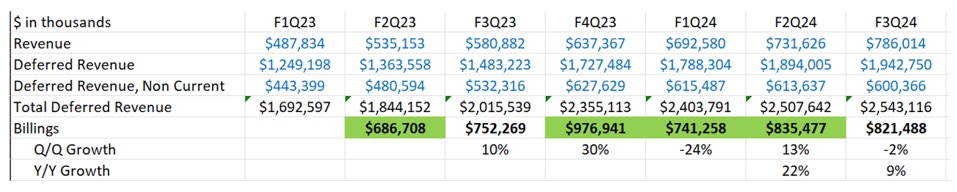

Billings also decelerated, matching what we’ve seen so far with CrowdStrike’s peers. Billings were calculated to have fallen (-2%) QoQ and +9% YoY to $821.5M for Q3, a significant slowdown from the +13% QoQ and +22% YoY growth rate recorded in the prior quarter. You can read more about billings and ARR in our CrowdStrike’s Q3 earnings recaphere.

Source: I/O FUND

Pictured Above: I/O Fund calculations for CrowdStrike’s billings growth/decline

CrowdStrike also recorded its first quarter to generate operating income, albeit at a razor-thin 0.4% operating margin. However, this shift to a positive margin benefited the bottom-line, allowing net margin to expand ~225 bp QoQ to ~3.4%. This marked CrowdStrike’s third straight quarter of GAAP profitability, with sequential growth in each of the three quarters. We had previously mentioned that while CrowdStrike had begun to post GAAP profitability, it was preferable that the company be GAAP profitable from operations rather than interest income – now, the next task is for CrowdStrike to show further growth in operating income.

Conclusion

Aside from Fortinet, the remaining cybersecurity stocks covered here have all rallied to new highs following earnings, despite each report having some weaknesses. Cybersecurity stocks are investor favorites due to an ever-growing need for cybersecurity solutions among enterprises and high cash flow generation metrics – all of the four reported free cash flow margins higher than 30%. Billings growth remains an important metric to track, given the decelerations seen this quarter and hints at more deceleration ahead. Yet, these key metrics are providing clues as to which companies will be strongest moving into 2024.

Damien Robbins, Equity Analyst at the I/O Fund, contributed to this article.

Recommended Reading:

More To Explore

Newsletter

Oracle Soars After Earnings – Is ORCL Stock Still a Buy?

The market is clearly excited about this report, and for good reason. Remaining performance obligations (RPO) grew 359% YoY with cloud RPO growing “nearly 500%” on top of 83% growth last year. Another

Nvidia Stock Forecast: The Path to $6 Trillion

Two years ago, the April 2023 quarter delivered a historic 18% beat, followed by an even bigger 30% beat in July 2023. Compare that to the most recent quarter ending July 2025 — just a 4% beat, the sm

Bitcoin Bull Market Guide: When to Hold, Trim, or Re-Enter (Webinar)

Our track record including a more recent 600% move in Bitcoin is not the product of hype but of a systematic framework—one built on technical analysis, on-chain metrics, and a close watch on global li

Reddit Stock Blows the Doors Off - Can it Last?

Reddit’s stock has surged 62% in one month, easily placing the company’s earnings report as one of the best to come out of the tech sector this quarter. The world’s leading forum site has only 416 mil

ServiceNow Q2 Earnings: Inside the AI Push Toward $1 Billion ACV by 2026

Last month, after ServiceNow reported second quarter results that exceeded expectations on multiple fronts, shares of NOW rose by 6%. The company is attempting to reposition itself beyond a provider o

Is Bitcoin’s Bull Run Nearing a Top? What the Herd Missed at $16,000 and is Missing Now

In late 2022, when Bitcoin was trading near $16,000, the I/O Fund issued a Strong Buy Alert. At the time, many of the market’s biggest crypto bulls were silent. Fast forward to today, Bitcoin is up ov

Is the S&P 500 Overdue for a Correction? 2025 Forecast & Buy Levels to Watch

In our last Broad Market Report titled, Historic Uncertainty Meets $7 Trillion Dollar Debt Wall: What Comes Next For The S&P 500, the S&P 500 was trading near 5800 and still well below its February hi

Google Stock Clears Major Hurdle, Yet One Serious Concern Remains

This week, Google cleared a major hurdle with Search accelerating from 10 points of growth last quarter to 12 points this quarter -- putting to rest many doubts that Search monetization is at risk giv

Can Oracle Become the Next $1 Trillion AI Stock?

When it comes to AI cloud leaders, Oracle is not often mentioned, yet the company is quickly positioning itself to lead among Microsoft, Amazon and Alphabet when it comes to cloud growth over the next

Robinhood Stock: Spot Crypto Volumes May Lead to Incoming Volatility

Robinhood’s fundamental transformation over the past two years has been nothing short of remarkable. Crypto is driving strong revenue growth at 50% YoY in Q1, while TTM operating margin is approaching