Apple’s Services Growth Flywheel Continues To Strengthen

November 21, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Nov 16, 2023,05:19pm EST

Apple’s Services segment was one of the brightest spots in a relatively in-line earnings report at the beginning of November, topping an $85 billion run rate as growth jumped back to the high double-digits after a string of single-digit growth. Services demonstrated that its growth flywheel continues to strengthen with multiple outlets of opportunity in sight — from AI, to further growth in the installed base, to price hikes across different Services bundles.

Services Growth Outpaces iPhone, Apple

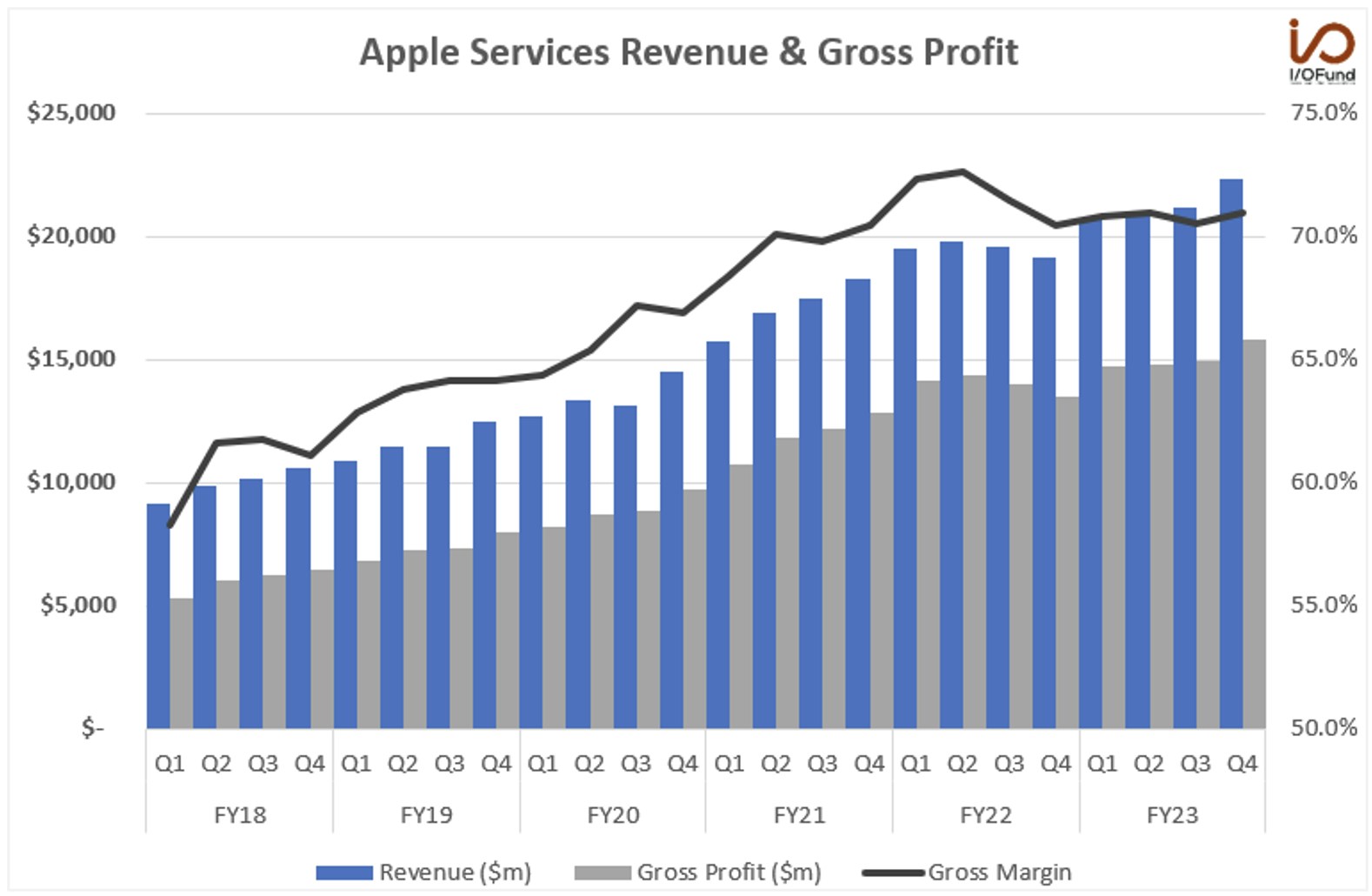

Since fiscal 2018, Services has become increasingly important to both the top and bottom lines for Apple. The segment has seen its share of revenue rise from under 15% five years ago to 22.2% at the end of September. Since then, Services has seen its annual run rate increase from ~$40 billion to over $85 billion, on track to surpass a $100 billion run rate potentially as early as the second half FY24.

FY21 was a breakout year for Services – the segment recorded greater than 24% YoY growth and generated more than $10 billion in gross profit each quarter, as its gross margin neared 70%. Gross margin has continued to stay above the 70% range, rising as high as 72.6% in Q2 FY22.

Source: I/O Fund

FY23 ending in September saw a full year growth rate of 7.1% YoY for $85.2 billion outpacing both iPhone and company-wide growth, with Q4 being the strongest quarter of the fiscal year with a growth rate of 16.3% YoY. The I/O Fund recently covered Apple’s earnings report more in-depth following fiscal Q4 here.

Since FY18, Apple has grown revenue at a 7.6% CAGR, meanwhile, Apple’s company-wide gross profit has grown at a 10.1% CAGR over the same period with profits partly impacted by Services’ rising contribution and expanding margin.

Compared to Apple, Services is seeing revenue and gross profit grow at much quicker rates – more than 9 percentage points higher for both metrics. Since FY18, Services revenue has grown at a 16.5% CAGR, outpacing Apple’s 7.6% growth rate as well as the iPhone’s 4.0% CAGR, due to the unevenness in revenue in between upgrade cycles – iPhone delivered YoY revenue declines in FY19, FY20, and FY23.

Services’ gross profit has expanded at a 20.1% CAGR, rising around 150% since FY18, from $24.2 billion to $60.3 billion as gross margin has expanded 10 percentage points, from 60.8% to 70.8%. This strong revenue and gross profit growth over the past five years has seen Services gain importance to Apple’s margins and its bottom line.

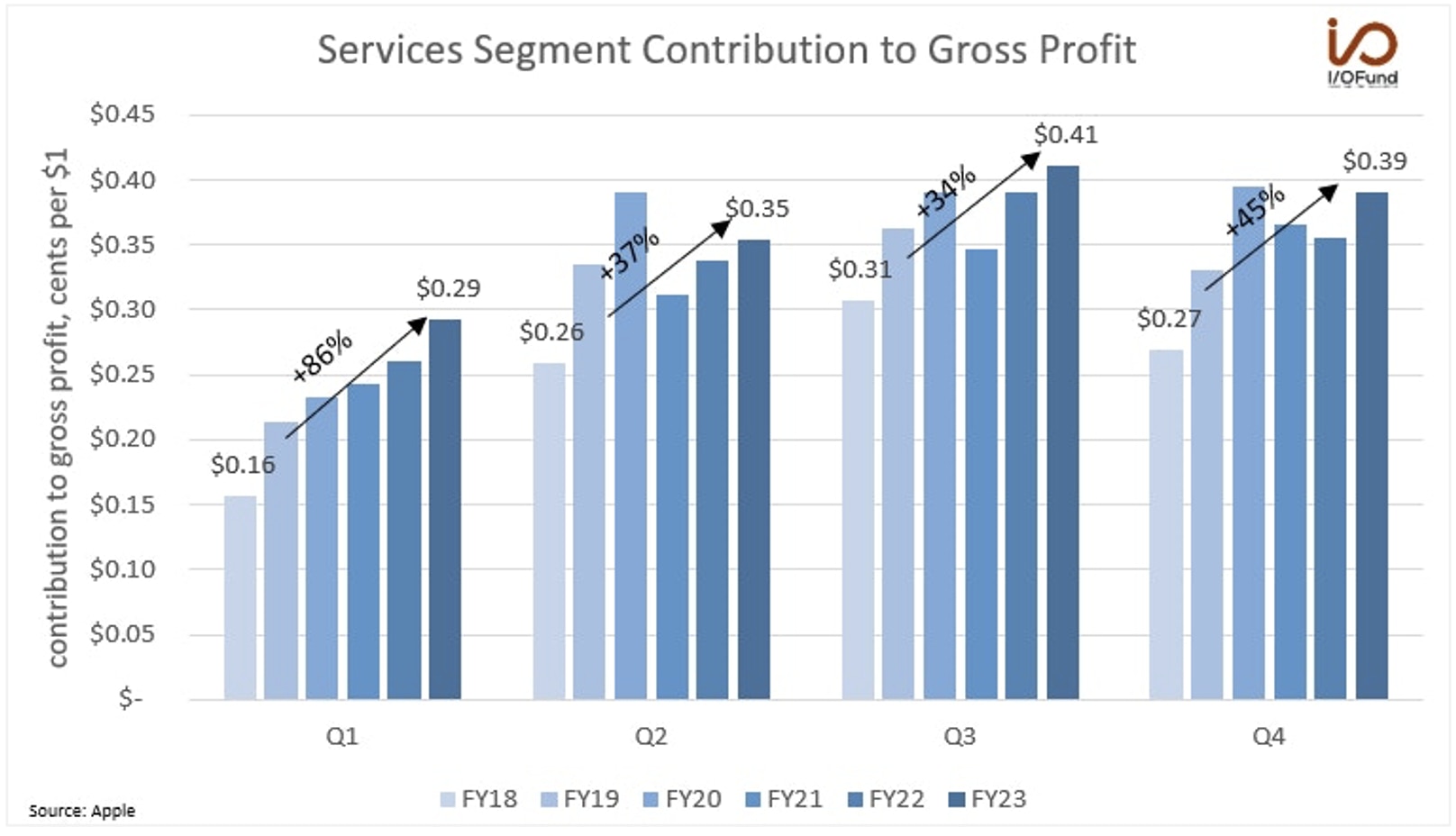

Source: Apple

In FY18, Services contributed 23.7% of Apple’s gross profit, whereas today, Services contributes 36% of gross profit.

The breakdown looks like this:

As Services’ share of revenue rose from 15% to 22.2%, it helped pull Apple’s gross margin ~580 bp higher in just five years. Product gross margin – iPhone, Mac, iPad, etc. – increased just 210 bp, meaning this expansion in gross margin is primarily coming from Services.

FY21 was a breakout year for Apple’s gross margin, expanding from 38% to more than 42% because of that growth in Services. Apple is guiding for gross margin to expand further in fiscal Q1 next year, to the 45% to 46% range – an expansion of 200 to 300 bp YoY, with Services’ growth rate forecast to be in the high-teens again.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Services Seeing Multiple Growth Outlets

Services growth has been broad based, with new revenue records across a range of different offerings, and the segment has multiple growth outlets to lever in the future, from growth in paid subscribers, AI, and price hikes.

CEO Tim Cook explained on Apple’s Q4 earnings call that the Services segment “achieved all-time revenue records across App Store, advertising, AppleCare, iCloud, payment services, and video, as well as the September quarter revenue record in Apple Music.” CFO Luca Maestri added that Services “reached all-time revenue records in the Americas, Europe and rest of Asia-Pacific and a September quarter record in Greater China.”

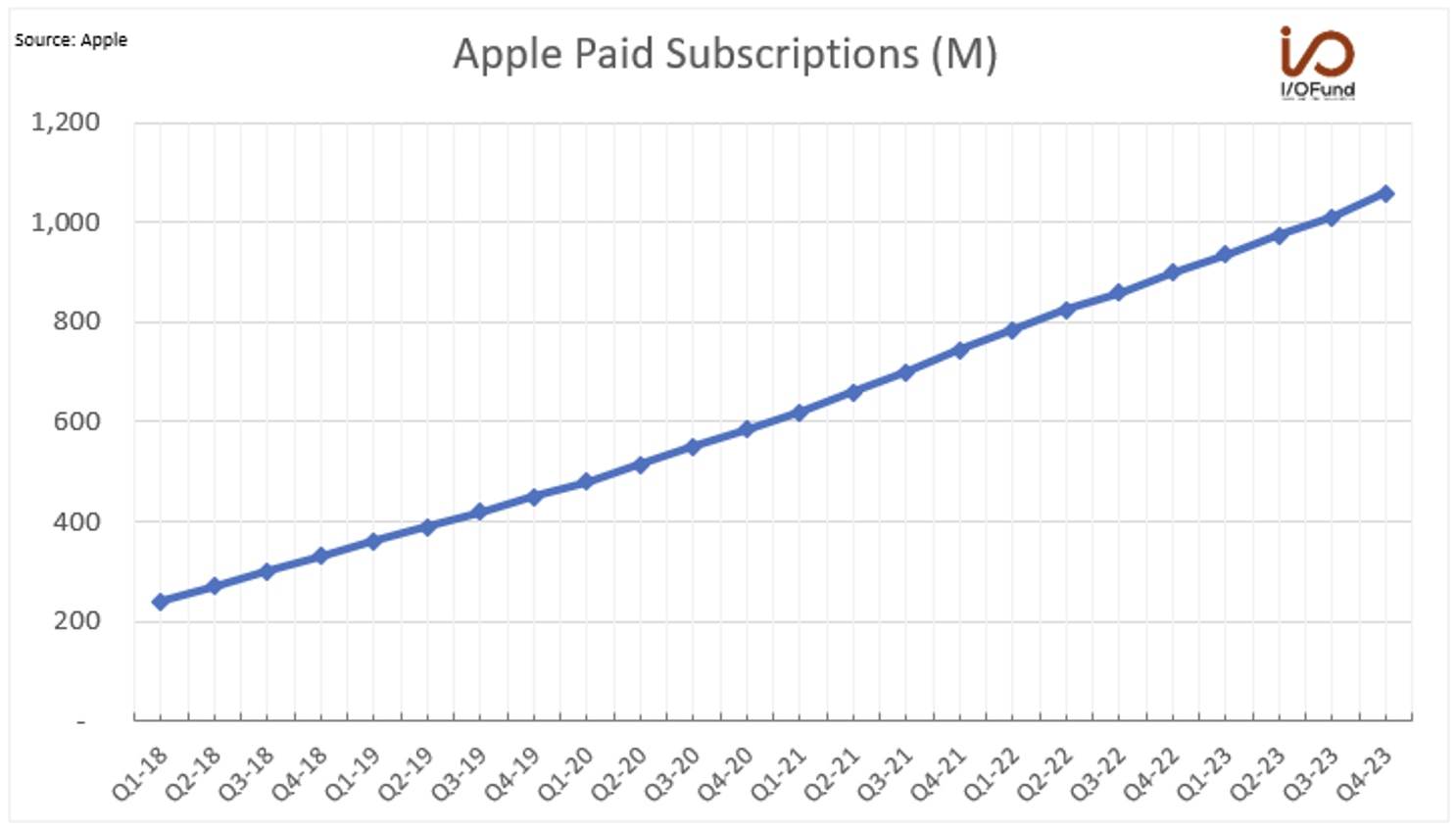

What is driving these record levels across multiple Services offerings and in every geography worldwide is solid growth in active devices and strong growth in paid subscriptions. Paid subscriptions have risen at more than 27% annually over the past five years to 1 billion by the end of FY23.

Source: APPLE

Apple has surpassed 2 billion installed devices, and “continues to grow at a nice pace and establishes a solid foundation for the future expansion of the ecosystem.” Thus, the organic growth flywheel for Services remains soundly intact – growth in installed devices driving growth in paid and transacting accounts at a higher degree.

At the start of FY18, Apple reported that it had an installed active device base of 1.3 billion devices, meaning it had a ratio of about 0.18 paid subscriptions per 1 active device. Since then, installed devices have grown more than +50% to over 2 billion, while paid subscriptions have grown nearly +360% to almost 1.1 billion, or a ratio of about 0.5 paid subscriptions per active device.

Reaching new all-time highs in its installed device base signals further growth lies ahead for Services, especially as the ratio of paid subscriptions per active device continues to rise. Other outlets of growth arise from Apple’s recent price hikes and potential monetization opportunities from AI.

Additional Levers

Apple recently enacted some price hikes for News+, Arcade, and its One bundles, with the hikes ranging from $2/mo to $5/mo. As a whole, the price hikes could generate an additional ~$5 billion in annual revenue with just a 15% attach rate to Apple’s more than 1 billion paid subscriptions — however, the price hikes could incur a small amount of churn, among more price-sensitive consumers.

In terms of AI, Apple is not releasing any details about projects in development, though it is rumored that some of the AI products Apple is working on would improve Siri and Messages’ capabilities, or add features to Keynote, Pages, and Apple Music. Apple’s large language model ‘Apple GPT’ is reportedly under development, but a commercialization route is still undetermined. The next-generation of Apple’s software, iOS 18, macOS 15, and watchOS 11, are poised to bring AI features to Apple’s devices next year, as it works to catch up in the generative AI deployment race against OpenAI and Google.

For any of its AI products, there are three routes that could boost Services revenue – adding AI features for free in an aim to boost engagement across offerings, charging a subscription fee for AI features, or increasing prices of current bundles that incorporate AI. For example, if Apple charged for a stand-alone AI subscription at a $2.99/mo price point, it could rake in ~$10.8 billion in annual revenue at a 15% attach rate to its more than 2 billion active devices; boosting the prices of all of its subscription bundles by $0.99/mo could also add more than $10 billion annually.

In a previous Forbes article “AI Could Be Apple’s Next Chapter,” my firm pointed out that: “although Apple is tight-lipped about the progress of its AI projects, the so-called Apple GPT chatbot is rumored to be more powerful than Open AI’s GPT 3.5 model, according to The Verge. Apple is spending millions of dollars a day training the large language model Ajax on more than 200 billion parameters.”

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

iPhone Demand Uncertain, China Risks Remain

Analysts have expressed concern over the holiday launch trajectory of Apple’s new iPhone 15, hinting that supply shortages, lower levels of consumer spending, and shorter wait times suggest weaker demand. The iPhone remains Apple's main source of revenue, and a conservative fiscal Q1 guide from the company along with heightened concerns over iPhone 15 demand add to risks that iPhone revenue growth in the near-term will remain depressed, after growing just +2.6% YoY in Q4.

Other concerns arise from Apple’s concentration in China, in regard to its iPhone supply base. Bank of America warned that Apple’s iPhone “supplier base remains largely in China,” which could “create many headwinds including around production, demand, [and] competition,” given that it is “hard to move all elements out of China.”

Services remains strong and a segment to watch, but we need the iPhone to participate and come in strong too, with a lingering risk to watch around China. Without the iPhone participating, Services is not enough to carry Apple’s stock alone, especially given its current valuation trading at levels hard to sustain.

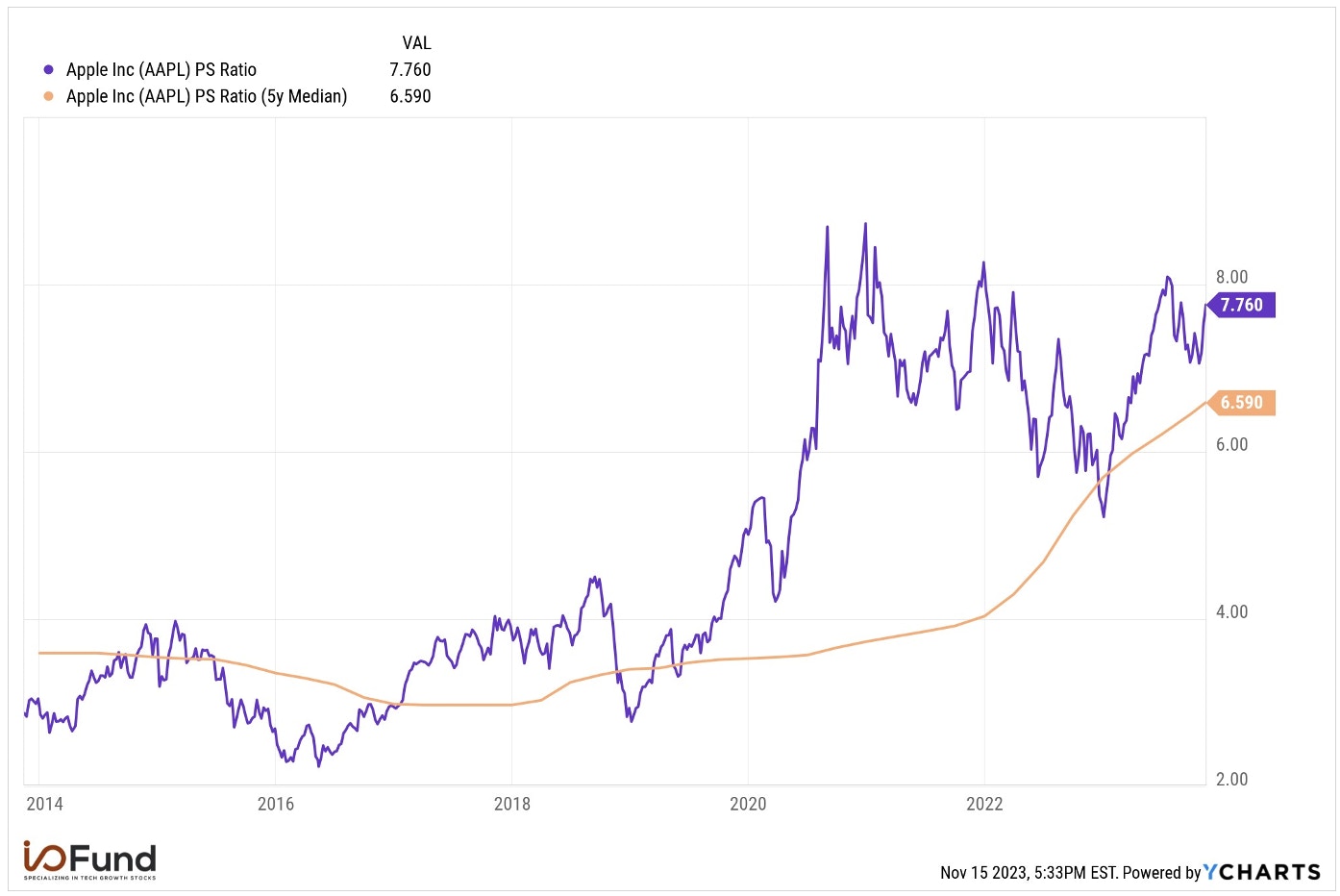

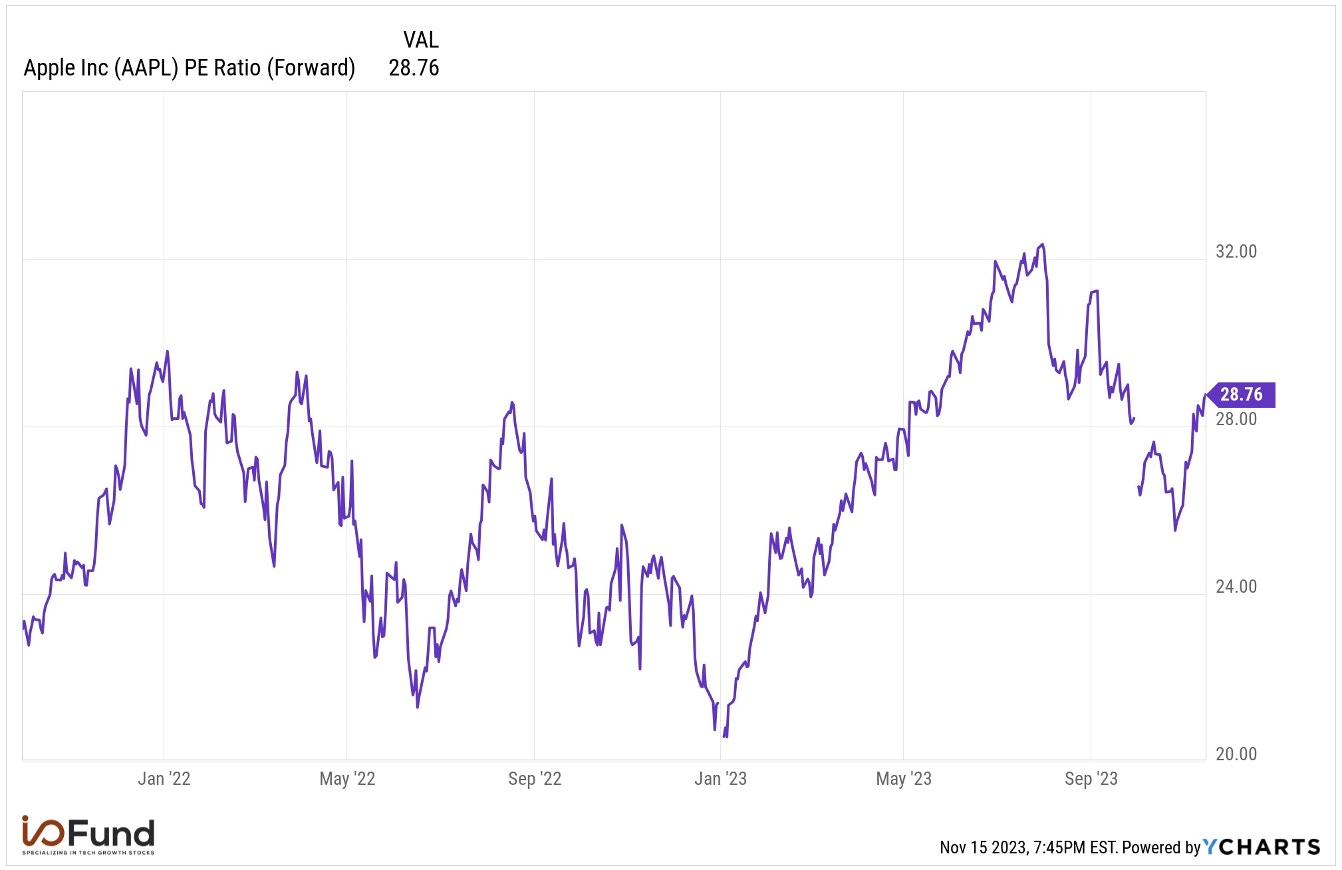

Source: YCHARTS

Apple is currently trading at a 7.76x P/S ratio, above its 5-year median P/S ratio of 6.59x, with the 8.0x a level that Apple has struggled to hold on to since spiking to it in 2020. Apple is also trading at a nearly 28.8x forward P/E ratio, again another valuation level that it has struggled to hold on to – since late 2021, Apple has generally pulled back to below 24x forward P/E after trading above the 28 range.

Source: YCHARTS

However, another risk to watch is Alphabet’s antitrust trial, as it could have direct implications for Apple in the event of a negative ruling. Alphabet’s multi-billion dollar payments to Apple for Google to be the primary search engine on Safari across Apple’s devices is at the center of the trial, and that payment is rumored to be ~$19 billion this year – a key witness mentioned during the trial that Google is paying Apple 36% of search advertising revenue it generates via Safari. Should the scale of those payments constitute monopolization of the search market, Apple could be set to lose on a lucrative Services revenue stream.

Conclusion

Services is rapidly becoming one of Apple’s most important top-line segments, and arguably is the most important for Apple’s bottom-line, given its outsized role in boosting Apple’s gross margin. Organic growth has been a strong driver of Services’ +16.5% 5-year revenue CAGR and its +20.1% 5-year gross profit CAGR, both of which outpace Apple’s growth rates by more than 9 percentage points.

Should Services continue to grow in the teens for the next five years, such as at a 14% 5-year CAGR through FY28, it would be generating approximately $164 billion in revenue, or slightly more than 30% of Apple’s projected $538.6 billion in revenue. Price hikes, introduction of AI features, or finding ways to increase engagement and boost the ratio of paid subscriptions per active device all support this long-term revenue growth outlook for the segment.

Damien Robbins, Equity Analyst at the I/O Fund, contributed to this article.

The I/O Fund was early to AI with a 45% allocation in 2023. For more in-depth research from Beth, including 15-page+ deep dives on the 10 stock positions the I/O Fund owns, subscribe here.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb

The AI Networking Stock That Beat Nvidia by 7X YTD for Returns of 135% YTD

AI networking stock Lumentum is among the key I/O Fund winners in 2026. We allocated heavily to LITE in January—a month before Nvidia backed the company. While most investors couldn’t stomach taking a

Bloom Energy — Our 2026 Top Pick Was the Best Performing Stock in April

April was the best month in six years for the Nasdaq-100. The single best-performing large-cap stock wasn't Nvidia, Microsoft, or Meta. It was Bloom Energy, up roughly 109% in one month. As you'll rec

Inside Nvidia’s $4B Optical Strategy—and Why CPO Changes Everything

Within the AI investment theme, there is nowhere that the supply chain shifts faster than in networking, leading companies to gain content on new platforms or lose incremental share. The reason is str