I/O Fund’s Preview of 7 Semiconductor Stocks Ahead of Q4 Earnings

January 21, 2022

Royston Roche

Equity Analyst

It is the first of the series of earnings previews for Q4. We chose Lam Research, AMD, Teradyne, Nvidia, Texas Instruments, Broadcom, and Qualcomm for the Semiconductor sector. To understand valuations across semis and how the sector is positioned moving into earnings, please reference our analysis, “I/O Fund’s Semiconductor Q4 2021 Earnings Preview.”

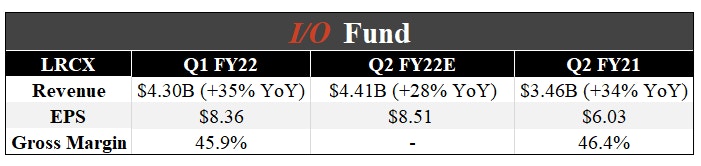

Lam Research – Earnings on January 26th

Source: YCharts and Earnings reports

According to the analysts’ consensus estimates, revenue is expected to grow 28% YoY for the next quarter. In the last earnings call, the management mentioned that early indication suggests that Wafer Fab Equipment will show another year of growth in the calendar year 2022. It will be interesting to hear their comments on WFE in the next earnings call, particularly since the analysts forecast its revenue growth to slow down for the next two fiscal years. Revenue is expected to grow 4% in the FY23 and FY24, down from 21% for FY22.

Wells Fargo in its recent report says that the chip-equipment makers will remain volatile in the upcoming earnings season. Analyst Joe Quatrochi said that trading in semiconductor capital equipment stocks, "could remain relatively volatile" over the near term as share prices are likely to be affected by any changes that companies make to their quarterly earnings and sales outlook.

With regard to Lam Research, he says that the ongoing supply chain issues and the company ramping up production at a new facility in Malaysia are having a negative impact on the company’s gross margins.

Barclays analyst Blayne Curtis raised the firm's price target to $750 from $625 and keeps an Overweight rating on the shares. The analyst sees "positive outlooks providing some relief" for the semiconductor group but still struggles with "just how much upside is left as cyclicality still looms for many names."

Mizuho analyst Vijay Rakesh raised the firm's price target to $770 from $700 and keeps a Buy rating on the shares. The analyst gave his outlook across semis and automotive technologies and his top sectors in 2022 are memory, wafer fab equipment, data center, 5G and electric vehicles.

Please note, the I/O Fund may or may not agree with the financial analysts mentioned above yet we objectively report what the Street is saying. You may view our previous analysis on the company below:

I/O Fund’s Preview of 7 Semiconductor Stocks Ahead of Q3 Earnings

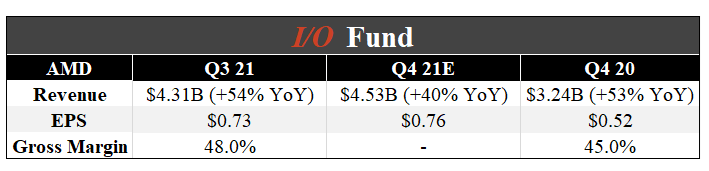

Advanced Micro Devices Inc – Earnings on February 1st

Source: YCharts and Earnings reports

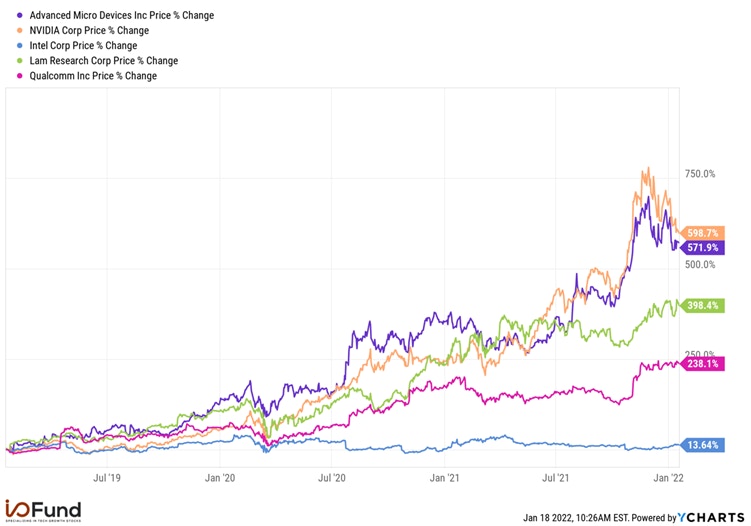

AMD’s stock rose around 570% in the past three years. The company’s strong revenue growth is due to its superior products have also boosted its share price.

The company’s revenue grew more than 50% YoY in the last five quarters. The analysts’ consensus estimates suggest revenue to grow 40% YoY in the next quarter to $4.53 billion. The company’s data center revenue more than doubled in the last quarter and it will be interesting to hear the management’s comments on this in the next earnings call.

Source: YCharts

Wells Fargo analyst Aaron Rakers has an overweight rating and a $180 price target. He believes that the company will likely continue to take market share over the next five years while growing its total addressable market, which could boost earnings to $6 per share by 2025. “With an expectation that the PC CPU market will sustain a structurally higher post-COVID TAM (est. a ~$40B TAM), an estimated mid/high-single digit CAGR in AMD's data center TAM [CPU + GPU], and with the inclusion of a ~$8.5B incremental TAM via Xilinx, we estimate that AMD now addresses a $100B-110B+ TAM (vs. $79B TAM outlined at March '20 Analyst Day)".

KeyBanc analyst John Vinh has an overweight rating and price target of $155. In his words, "One of the most compelling data center growth stories, given its exposure to cloud and continued market share gains,". He further added, "We view AMD as one of the most compelling server growth stories in the semiconductor industry, given its outsized exposure to CSPs vs. enterprise. Additionally, we expect AMD to significantly outpace cloud industry growth in 2022 of high teens, as we expect continued market share gains."

Please note, the I/O Fund may or may not agree with the financial analysts mentioned above yet we objectively report what the Street is saying. You may view our previous analysis on the company below:

AMD Stock is Approaching a 20 Year Roadblock – Will History Repeat?

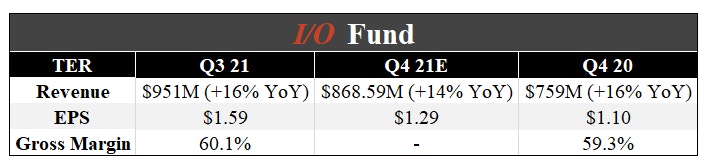

Teradyne Inc – Earnings on January 26th

Source: YCharts and Earnings Reports

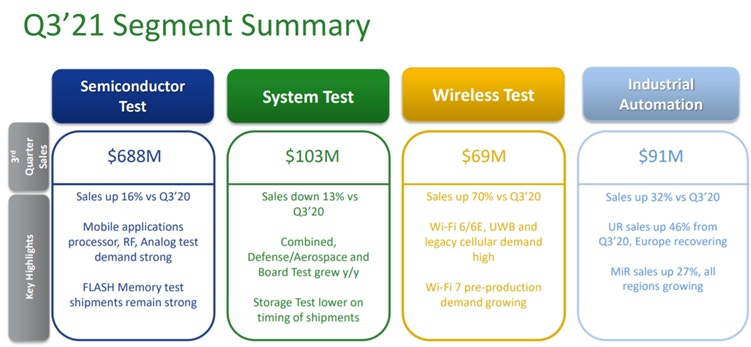

Teradyne’s revenue grew 16% YoY in Q3 and the consensus estimates suggest revenue to grow 14% YoY in the next quarter. Industrial automation currently constitutes roughly 10% of the total revenue. According to the management this could be one of the growth areas for the company’s future as the penetration is low.

The company’s outlook for 2022 and the medium-term earnings outlook update is expected in the next earnings call. This is particularly important as analysts expect slower revenue growth of 9% for 2022 and 2023.

Source: Investor Presentation

Deutsche Bank analyst Sidney Ho has raised the price target to $170 from $150. The analyst is more optimistic about long term demand drivers, rising capital intensity, and the regional push for semiconductor manufacturing capabilities entering 2022. This should lead to wafer fab equipment spending sustaining at a high level. He believes semiconductor capital equipment stocks can justify trading at multiples above historical averages.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Piper Sandler analyst Weston Twigg has a price target of $173. The analyst has a positive view on the company's fundamentals given its Arm test opportunities, memory market share gains, and continued robotics growth. He expects Teradyne's annual robotics revenue to exceed $1B by 2025 on "strong post-pandemic automation trends." Twigg views the company as a "compelling robotics automation play, coupled with good multi-year core test market tailwinds."

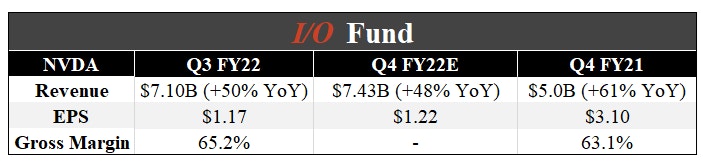

NVIDIA Corporation - Tentative Earnings date is February 24th

Source: YCharts and Earnings Reports

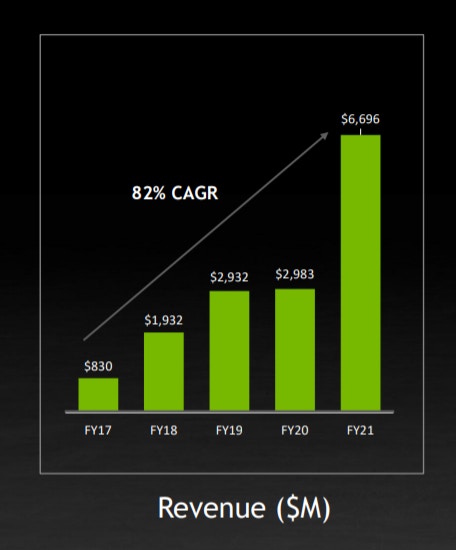

Nvidia’s revenue grew over 50% YoY for the past six quarters. Analysts expect revenue to grow 48% YoY in the next quarter to $7.43 billion. Growth has been particularly strong in the data center, which grew at a compounded annual growth rate of 82% from FY17 to FY21.

Source: Investor Presentation

Citi analyst Atif Malik opened a "Positive Catalyst Watch" on shares of Nvidia post the Consumer Electronics Show. Management commented on the "strong" holiday gaming season, "solid" data center demand trends and gaming/networking foundry supply improvements in the second half of the year. The analyst views Nvidia's January quarter earnings, launch of a new data center and potentially gaming 5nm products at a conference in March as positive catalysts for the stock.

BofA analyst Vivek Arya reiterates a Buy rating on Nvidia with a $375 price target after hosting an investor call with the company's CFO, Colette Kress. The analyst "heard confidence around momentum" heading into 2022 across gaming, data center and "nascent omniverse/autos opportunities." Capacity remains a bottleneck, with demand outpacing supply throughout 2021, especially in gaming, though management noted they are working hard on securing supply and they expect constraints to ease in the second half of 2022. The analyst calls Nvidia a "top compute pick" and continues to believe the company is best positioned to "address several of the most important, multi-decade secular growth opportunities."

Please note, the I/O Fund may or may not agree with the financial analysts mentioned above yet we objectively report what the Street is saying. You may view our previous analysis on Nvidia below:

Throwback: Nvidia will Surpass Apple’s Valuation in 4.5 Years

The Key To Unlocking The Metaverse Is Nvidia’s Omniverse

Holding Nvidia Stock Will Pay Off Due to Two Impenetrable Moats

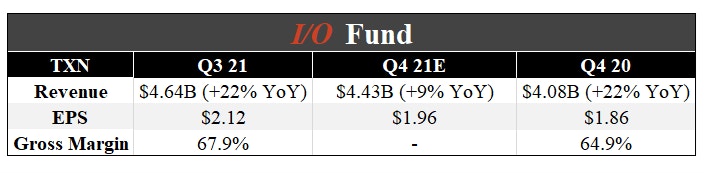

Texas Instruments Inc – Earnings on January 25th

Source: YCharts and Earnings Reports

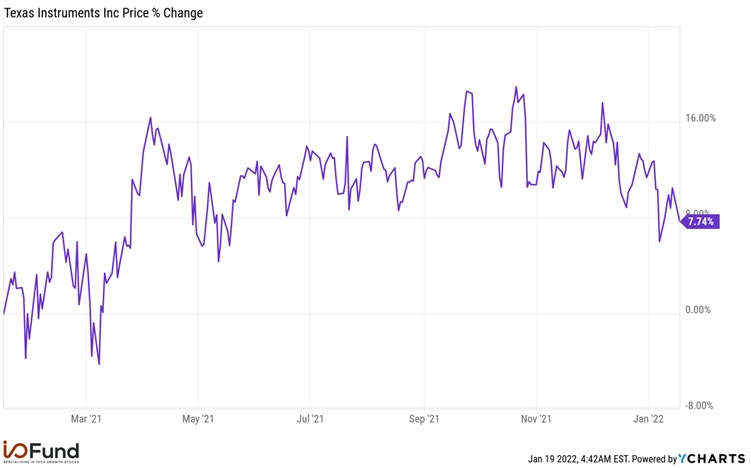

Texas Instruments revenue is expected to slow down drastically from 22% YoY growth in Q3 to 9% growth in the next quarter. The company has been steadily increasing its dividend payments over the years and has a decent dividend yield of 2.31%. At the time of writing, the stock has returned about 8% in the past year.

Source: YCharts

Barclays analyst Blayne Curtis raised the firm's price target to $180 from $170 and keeps an Underweight rating on the shares. The analyst sees "positive outlooks providing some relief" for the semiconductor group but still struggles with "just how much upside is left as cyclicality still looms for many names."

The company was downgraded by Citi. Analyst Christopher Danely lowered his rating to neutral and cut his price target to $187 from $220. In his words, "We estimate the new fab and higher depreciation will negatively impact gross margins by roughly 1%-3% in 2022 and our C22 EPS estimate is 6% below consensus.”

Broadcom Inc – Tentative Earnings date is March 4th

Source: YCharts and Earnings Reports

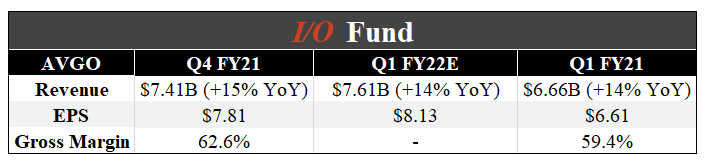

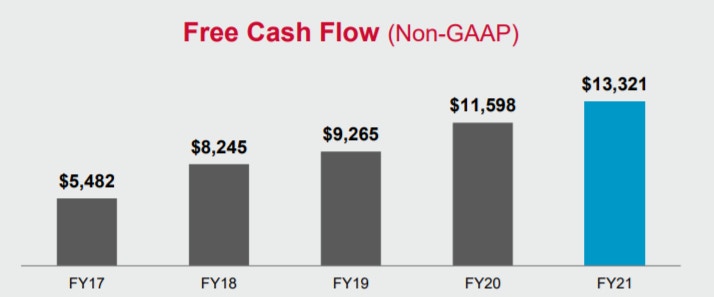

Broadcom’s revenue grew 15% YoY in Q4 FY21 and the consensus analysts estimate suggest revenue to grow 14% in the next quarter. The company has good free cash flows and for the fiscal year 2021, it constituted 49% of the total revenue. The current dividend yield is 2.58% and the quarterly dividend was increased by 14% to $4.10. One risk to watch is Apple planning to make chip components in-house. The company’s shares rose about 30% in the past year.

Source: Investor Presentation

Piper Sandler analyst Harsh Kumar raised the price target to $750 from $680 and keeps an Overweight rating on the shares. For 2022, the analyst favors "larger, more profitable, cash generating names that have a clear growth path ahead of them based on end-markets." Kumar sees cloud, enterprise, 5G infrastructure, electric vehicles, and connectivity as the primary areas of focus. He's cautious on the automotive end-market more broadly and PCs.

Bank of America analyst Vivek Arya, who rates Broadcom buy with a $750 price target and Skyworks neutral with a $190 price target, notes that both companies have significant exposure to Apple (AAPL), with 20% for Broadcom and 59% for Skyworks, but industry checks suggest the impact is "overblown in the near to medium term." Apple's hiring could be for its plans to develop its own 5G modem, which would hurt Qualcomm and not Broadcom or Skyworks.

Read our past coverage on the stock below:

I/O Fund’s Preview of 7 Semiconductor Stocks Ahead of Q3 Earnings

Will Dividend Stocks Become the Inflation Trade?

Qualcomm Inc – Tentative earnings date is February 3rd

Source: YCharts and Earnings Reports

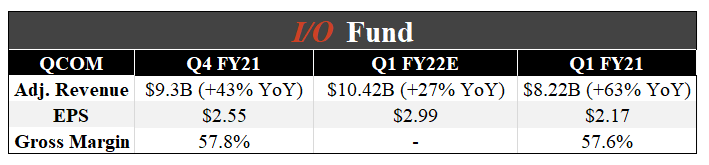

The company’s adjusted revenue grew 43% YoY in the Q4 FY21 and the analysts’ consensus estimate suggests revenue to grow 27% in the next quarter. However, growth will slow down to around 8% in the FY23 and FY24, down from about 19% revenue growth in the FY22.

The management expects future growth from automotive and the Internet of Things as the company looks for opportunities beyond the smartphone business. The company expects its addressable market to grow from the current $100 billion to $700 billion in the next decade.

KeyBanc analyst John Vinh raised the price target to $210 from $185 and keeps an Overweight rating. The analyst notes that at its analyst event, Qualcomm derisked concerns about Apple (AAPL), indicating its share of the 2023 iPhone would decline to 20% and would exit fiscal 2024 at a low-single digit percentage of QCT revenues, yet expects handsets to still grow at the industry three-year CAGR of 12%, as Android is expected to grow faster and offset. Qualcomm pointed out it has secured multiyear chip agreements over the next two years with all handset OEMs, Vinh adds. The analyst also highlights that auto revenues are expected to grow to $3.5B, anchored by key wins at General Motors and BMW.

Deutsche Bank analyst Ross Seymore raised the firm's price target to $210 from $190 and keeps a Buy rating. “It laid out an impressive roadmap of accelerated and diversified growth, further bolstered by a wide array of customer testimonials," The company's "impressive" financial targets are "significantly de-risking" by removing 80% of Apple in fiscal 2024, albeit with no certainty that the business will indeed be lost by that much that soon, according to the analyst.

The I/O Fund is a team of analysts that share their research publicly as they build a portfolio of 20 stocks. Our team has record results for a retail Fund and we also have four-digit gains on some of our free newsletter coverage. You can learn more about our premium service by clicking here or sign up for our free newsletter here.

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

More To Explore

Newsletter

AI Stocks in 2025: What Every Investor Should Know

The market evolves quickly, and nowhere is that more apparent than in AI stocks, which continue to lead in both innovation and returns. At the I/O Fund, our deep coverage of AI stocks, combined with a

Nuclear Power Emerging as a Clean AI Data Center Energy Source

Data center power demand is forecast to surge over the next decade, with some estimates seeing demand increasing 3x by 2030. Inference is expected to be a primary driver with power demand growth proje

AMD vs Nvidia: The AI Stock That Could Win by 2028

Last week, AMD offered more details on the release of their groundbreaking GPUs with little fanfare in the markets – which is par for the course as AMD has a history of being forgotten about until the

This AI Stock is Set to Surge from Inference Demand

Up until now, the AI conversation has been dominated by training and compute, yet inference is showing signs of exploding growth. Microsoft and Google recently highlighted 5x to 9x YoY growth in AI to

Taiwan Semiconductor Stock: AI Growth Amid Geopolitical Risk

Despite their leadership, AI stocks like Taiwan Semiconductor and Nvidia are flat year-to-date and trading at similar levels as June 2024. Clearly, the AI trade is not as straightforward as it might s

Historic Market Uncertainty Meets $7 Trillion Debt Wall: What Comes Next for the S&P 500

We are seeing mounting evidence that this bounce may be the start of a new push to all-time highs, such as improved breadth, better than expected earnings plus the size of this bounce. However, one ca

Nvidia Stock Faces a Choppy Q2, But Tailwinds Build for H2 Acceleration

Nvidia’s streak of blockbuster earnings has turned investor expectations into a high-stakes game— anything short of perfection risks disappointment. As the company gears up to report fiscal Q1 results

Microsoft Stock Surges After Q3 2025 Earnings: What Separates Azure from AWS, Google Cloud

Microsoft stock jumped after Q3 2025 earnings as Azure emerged as the only major cloud platform to accelerate growth this quarter — a rare feat amid macro pressures. Azure’s 35% constant currency grow

Why Bitcoin’s Bull Run May Be Nearing a Top Despite Pro-Crypto Tailwinds

Since calling the Bitcoin bottom near $16,000 in late 2022, the I/O Fund has maintained a disciplined, contrarian approach — issuing 13 buy alerts before Bitcoin surged above $100,000. Now, signs sugg

2025 Market Outlook: Why Stocks and Bonds Are Signaling More Volatility

As the S&P 500 reaches a key bounce target, troubling signs in bonds and consumer behavior suggest this market rally may be on thin ice. I/O Fund’s Knox Ridley explains why volatility may intensify an