Roku And Pinterest: Ad-Tech Earnings Review

August 25, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Aug 20, 2020,11:32pm EDT

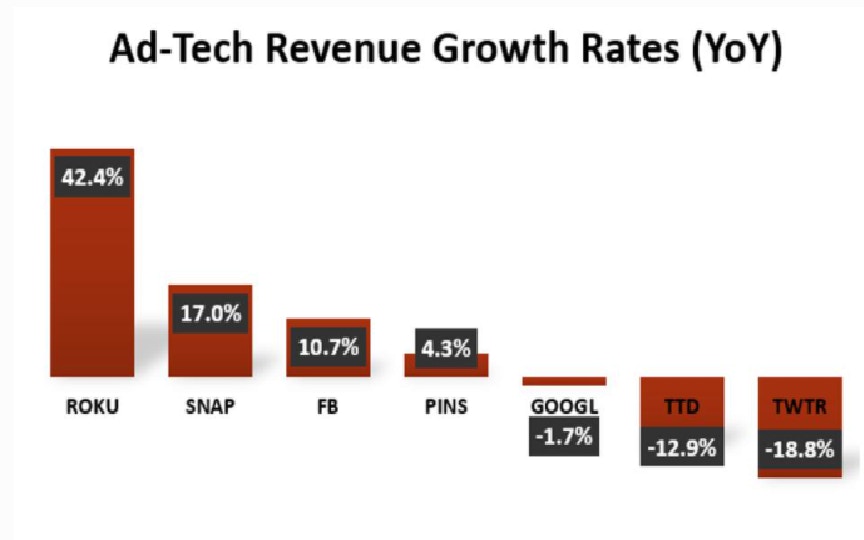

On August 5th, Roku announced very strong Q2 results led by outstanding account growth. Total revenue grew 42% YoY to $356 million, representing a beat of 7% above consensus estimates. This was by far the strongest Q2 sales growth across ad-tech as Roku’s competitors each posted significant revenue growth decelerations.

This was a challenging quarter for the industry, as digital advertising spend is expected to decline 5% YoY. Roku outpaced its competitors by growing monetized video ad impressions 50% and expanding first time ad clients 40%. From H1 2019 to H1 2020, Roku’s retention rate among advertisers that spent $1 million or more in H1 2019 was a resilient 92%.

Deutsche Bank is estimating that US ad spend for connected TVs will double over the next few years from the current $8B spent annually. Roku is ideally positioned to be the main beneficiary of this trend as growth in the number of active accounts and streaming hours reinforce Roku’s role as an essential distribution partner for advertisers who want to scale rapidly. Further, Roku is depending on the hardware portion of its business less than ever, as consumer hardware has shrunk from 55% of Roku’s revenue at its IPO to less than 30% in Q2.

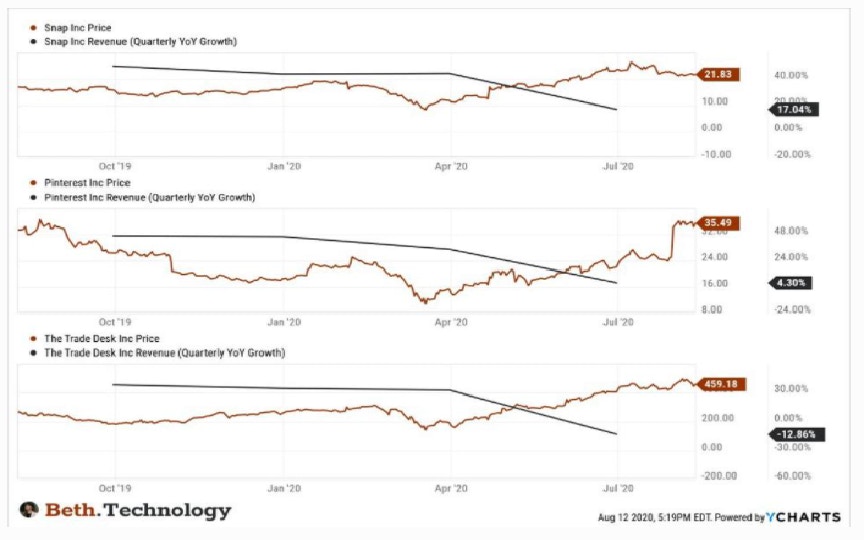

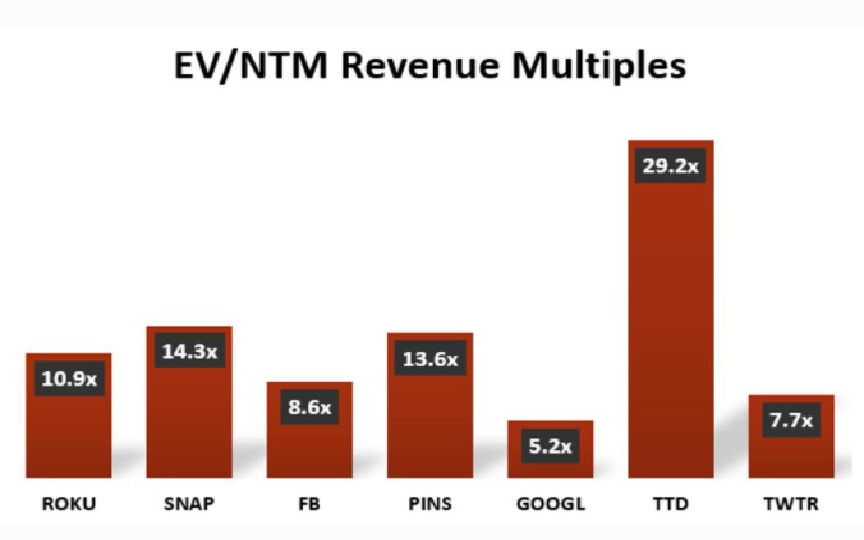

Despite posting the highest growth in the industry, Roku trades at the most attractive valuation in comparison to its peers. The Trade Desk, Snap Inc., and Pinterest have each seen their multiples expand 15%+ over the last year & trade at a premium to Roku. Their growth rates have declined significantly over the same time frame.

The Trade Desk, in particular, now trades at a 70% higher premium than it did a year ago while its growth rate has dropped from 38% to -12.9%. In comparison, Roku’s multiple has contracted from 12.8x to 11.4x despite posting consistent 40-55% growth. Roku is in an ideal position to continue to deliver sustained 30%+ growth as it has proven to be the most resilient ad-tech stock and will capitalize on growing ad spend for connected TVs.

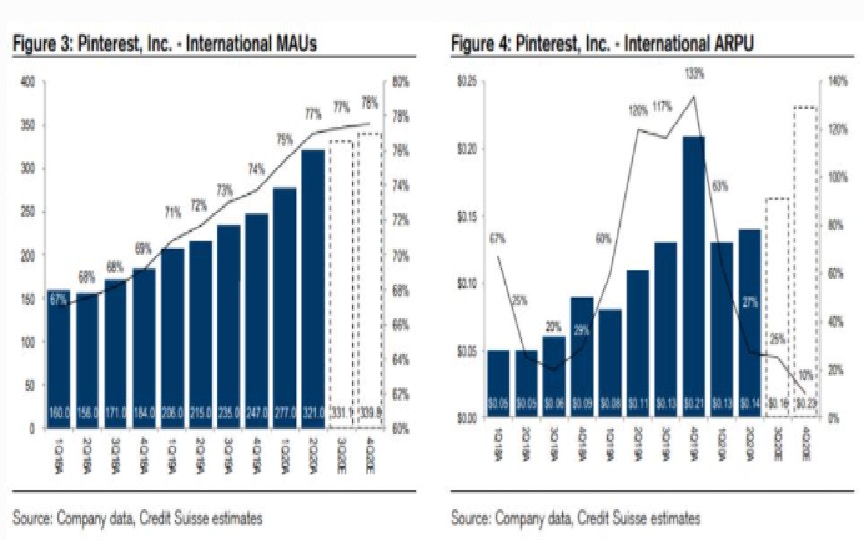

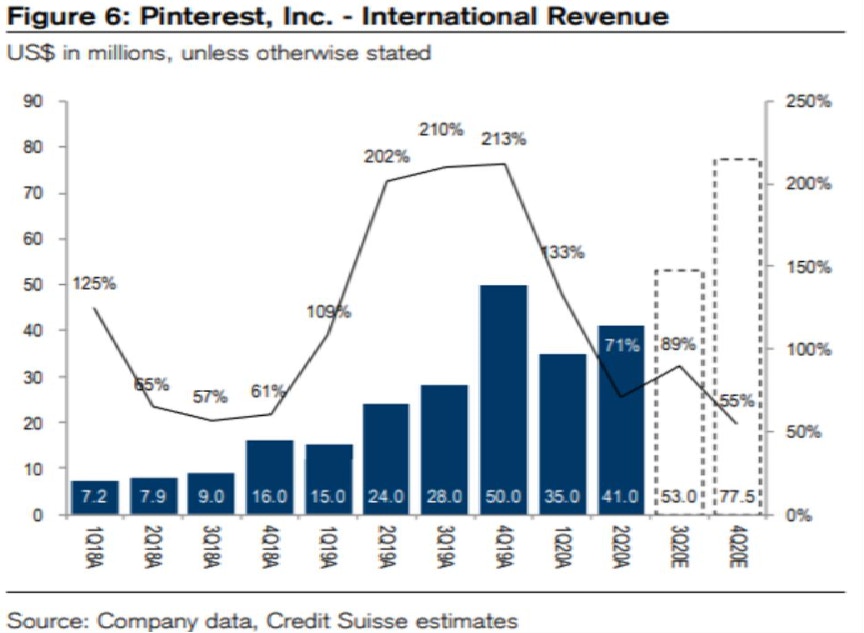

Pinterest reported better than expected Q2 results, beating consensus estimates by 9% on revenue and 7% on global monthly active users (MAUs). Most impressive was its international revenue growth, as the $42m number they announced came in 46% above estimates. Pinterest also reported 49% international MAU growth, blowing past estimates by 9%.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Pinterest saw broad based user growth in the US and international regions, so the key remains increasing its average revenue per user (ARPU), which dropped 21% globally to $0.70. In the US, the company’s ARPU was $2.50 (-11% YoY) while international ARPU was just $0.14. In comparison, Facebook’s global ARPU stands at $8.52. This represents a great opportunity for Pinterest to accelerate its growth, particularly by increasing monetization per-user internationally. Monetization for international regions should improve over time as the company expands its sales presence in under-capitalized markets.

Credit Suisse estimates Pinterest will report $0.23 International ARPU in Q4, representing a 64% improvement in international monetization from Q2. This would be the best quarter of international ARPU the company has ever reported, which coincides with estimates calling for a record quarter of international revenue.

Pinterest saw US revenue fall 3% YoY in Q2, but management guided for 35% growth in Q3 and noted that revenue in July accelerated 50% YoY. With the expected rebound from a weak Q2 in the US, Pinterest can reaccelerate its growth to 40%+ by capitalizing on its international monetization opportunity. Management addressed its plan for this opportunity in the conference call, clarifying that that they are investing in those markets by hiring aggressively and building out their sales team. If the company can execute on these initiatives to drive higher international ARPU, as analysts are forecasting, shares of Pinterest will benefit from the upcoming growth.

Clearly, ad-tech companies make solid investments especially for their tendency to have strong bottom line growth. This particular subsector usually has a clear path to profitability while other tech verticals must spend heavily on R&D. However, guiding for 30%+ revenue growth following single to double-digit negative growth carries risk as covid-19 has proven to drive unpredictable ad spend this year. Pinterest and The Trade Desk have set a high bar for themselves based off July results with this forward guidance.

As I covered previously, Apple’s changes to IDFA will likely put pressure on The Trade Desk as a third-party ad exchange without a first-party relationship. Pinterest also alluded to the decreased ability to measure conversions, yet thanks to their first-party relationship, this may be surmountable through their own measurement tools. These effects will begin to show up in Q4 after the release of iOS 14 in September.

More To Explore

Newsletter

Robinhood Stock: Spot Crypto Volumes May Lead to Incoming Volatility

Robinhood’s fundamental transformation over the past two years has been nothing short of remarkable. Crypto is driving strong revenue growth at 50% YoY in Q1, while TTM operating margin is approaching

AI Stocks in 2025: What Every Investor Should Know

The market evolves quickly, and nowhere is that more apparent than in AI stocks, which continue to lead in both innovation and returns. At the I/O Fund, our deep coverage of AI stocks, combined with a

Nuclear Power Emerging as a Clean AI Data Center Energy Source

Data center power demand is forecast to surge over the next decade, with some estimates seeing demand increasing 3x by 2030. Inference is expected to be a primary driver with power demand growth proje

AMD vs Nvidia: The AI Stock That Could Win by 2028

Last week, AMD offered more details on the release of their groundbreaking GPUs with little fanfare in the markets – which is par for the course as AMD has a history of being forgotten about until the

This AI Stock is Set to Surge from Inference Demand

Up until now, the AI conversation has been dominated by training and compute, yet inference is showing signs of exploding growth. Microsoft and Google recently highlighted 5x to 9x YoY growth in AI to

Taiwan Semiconductor Stock: AI Growth Amid Geopolitical Risk

Despite their leadership, AI stocks like Taiwan Semiconductor and Nvidia are flat year-to-date and trading at similar levels as June 2024. Clearly, the AI trade is not as straightforward as it might s

Historic Market Uncertainty Meets $7 Trillion Debt Wall: What Comes Next for the S&P 500

We are seeing mounting evidence that this bounce may be the start of a new push to all-time highs, such as improved breadth, better than expected earnings plus the size of this bounce. However, one ca

Nvidia Stock Faces a Choppy Q2, But Tailwinds Build for H2 Acceleration

Nvidia’s streak of blockbuster earnings has turned investor expectations into a high-stakes game— anything short of perfection risks disappointment. As the company gears up to report fiscal Q1 results

Microsoft Stock Surges After Q3 2025 Earnings: What Separates Azure from AWS, Google Cloud

Microsoft stock jumped after Q3 2025 earnings as Azure emerged as the only major cloud platform to accelerate growth this quarter — a rare feat amid macro pressures. Azure’s 35% constant currency grow

Why Bitcoin’s Bull Run May Be Nearing a Top Despite Pro-Crypto Tailwinds

Since calling the Bitcoin bottom near $16,000 in late 2022, the I/O Fund has maintained a disciplined, contrarian approach — issuing 13 buy alerts before Bitcoin surged above $100,000. Now, signs sugg