Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

June 12, 2026

Beth Kindig

Lead Tech Analyst

- Neoclouds are seeing massive hyperscaler demand as companies race to scale AI infrastructure, resulting in rapid revenue and backlog growth.

- Leaders like CoreWeave and Nebius enable this through access to the latest Nvidia GPU’s while also optimizing compute utilization.

- However, the bearish argument behind hyperscaler demand lies in their desire to offload their capex spending and shift costs to the operating expense line.

- CoreWeave’s and Nebius’ growth is far from profitable, as they seek to capture AI demand with limited cash flow and soaring debt loads in an increasingly tough macro backdrop.

- Circular financing, demonstrated by Nvidia’s investments and financial backstopping, is another key item to monitor closely

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices soar, differentiating themselves through quick access to the latest GPU compute and GPU utilization advantages that allow hyperscalers to rapidly add efficient compute capacity.

Notably, CoreWeave and Nebius have each secured 3.5 GWs of contracted power capacity; while these power footprints are key considering power is a hindrance to data center expansion, the vast majority of their contracted power capacity has yet to come online. CoreWeave is targeting 1.7 GW of active power by the end of 2026, while Nebius is targeting 800 MW to 1 GW of connected power.

In turn, they are quickly working to convert their contracted power to active power, and thus convert large backlogs into revenue. Yet doing so is extremely expensive, and neoclouds do not have the same cash nor operating cash flow profiles of Big Tech. This is leading neoclouds to employ unique and circular financing structures, raising some red flags.

In this analysis, I dive into the two public neoclouds that are riding Nvidia equity, hyperscaler contracts, and GPU-backed debt to fund the buildout, and what it means for the durability of the surge.

Microsoft and Meta’s $120B+ Bet on Neoclouds

The size of hyperscaler-neocloud partnerships compared to their current revenue is astounding. Microsoft has struck the most neocloud deals, with approximately $60 billion worth of commitments between CoreWeave, Nebius, and other private players such as Nscale. Meanwhile, Meta has committed $35.2 billion to CoreWeave in total after its recent $21 billion expansion, and an up to $27 billion deal with Nebius for a total commitment of up to $62.2 billion. Along with Meta, OpenAI is one of CoreWeave’s two largest customers, while CoreWeave also has a multi-year compute agreement with Anthropic.

Alone, Microsoft and Meta’s total commitments extend up to $122.2 billion – for perspective, that is ~90% of the TTM revenue of AWS being allocated towards neoclouds over long-term capacity deals. When factoring in hyperscaler-backed deals from OpenAI and Anthropic (although exact deal value is unknown), total potential commitments surpass $145 billion.

Keep in mind, CoreWeave’s FY2026 estimated revenue is $12.6B and Nebius FY26 revenue is expected to be $3.4B - therefore, these partnerships are leading to commitments that are an order of magnitude higher than current sales.

The reason hyperscalers are willing to allocate this capital to a relatively new business model in the neoclouds is three-fold – quick access to leading GPU generations, optimized compute utilization, and the added benefit of not having to recognize capex on the balance sheet – we look at each of these drivers below.

Neocloud Advantage is Offering Quick Access to GPUs

At its root, neocloud demand is a product of hyperscalers' insatiable demand for compute capacity. However, neoclouds can often add compute capacity much faster than hyperscalers can through internal builds, offering a key value proposition for Big Tech. As hyperscalers spend hundreds of billions a year on AI compute, minimizing the lag between data center expenses and revenue generation is critical to maximizing their return on investment.

Supporting the argument around neocloud’s advantage lying within time to deployment, commercial real estate giant JLL notes, “Neoclouds can deploy high-density GPU infrastructure within months compared to multi-year builds for hyperscale data centers, providing crucial time-to-market advantages for businesses needing rapid AI development.”

mid

In CoreWeave’s S-1 Registration filing, it lists “Faster access to the latest AI infrastructure advancements” as one of its key benefits to customers. Specifically, CoreWeave says “we were among the first to deliver NVIDIA H100, H200, and GH200 clusters into production at AI scale, and the first cloud provider to make NVIDIA GB200 NVL72-based instances generally available. We are able to deploy the newest chips in our infrastructure and provide the compute capacity to customers in as little as two weeks from receipt.”

Nebius makes a similar statement in its Annual Report, noting its “consistent track record of being one of the first to deploy the latest generation of NVIDIA GPU chips.”

CoreWeave and Nebius' relationship with Nvidia is key to acquiring the latest GPUs ahead of others. Nvidia recently invested $2 billion in both CoreWeave and Nebius. Under these partnerships, CoreWeave and Nebius will each look to deploy more than 5 GW of data center capacity by 2030.

CoreWeave recently demonstrated its ability to offer quick access to the latest chips and newest architectures to hit the market once again, being the first to have a Vera Rubin system up and running at the start of June. This provides evidence that partnering with CoreWeave and Nebius can help hyperscalers access as much of the latest GPU compute as possible in short order.

Beyond Hardware: Neocloud Platforms Offering Higher GPU Utilization

Aside from raw compute access, CoreWeave and other neoclouds layer on software and additional capabilities that improve GPU utilization – a key value add for hyperscalers.

For example, CoreWeave Kubernetes Service (CKS) helps coordinate the allocation of workloads across thousands of GPUs, while its SUNK service helps optimize GPU utilization by allowing training and inference workloads to run on the same cluster. CoreWeave Tensorizer enables high-speed model loading, reducing GPU idle time.

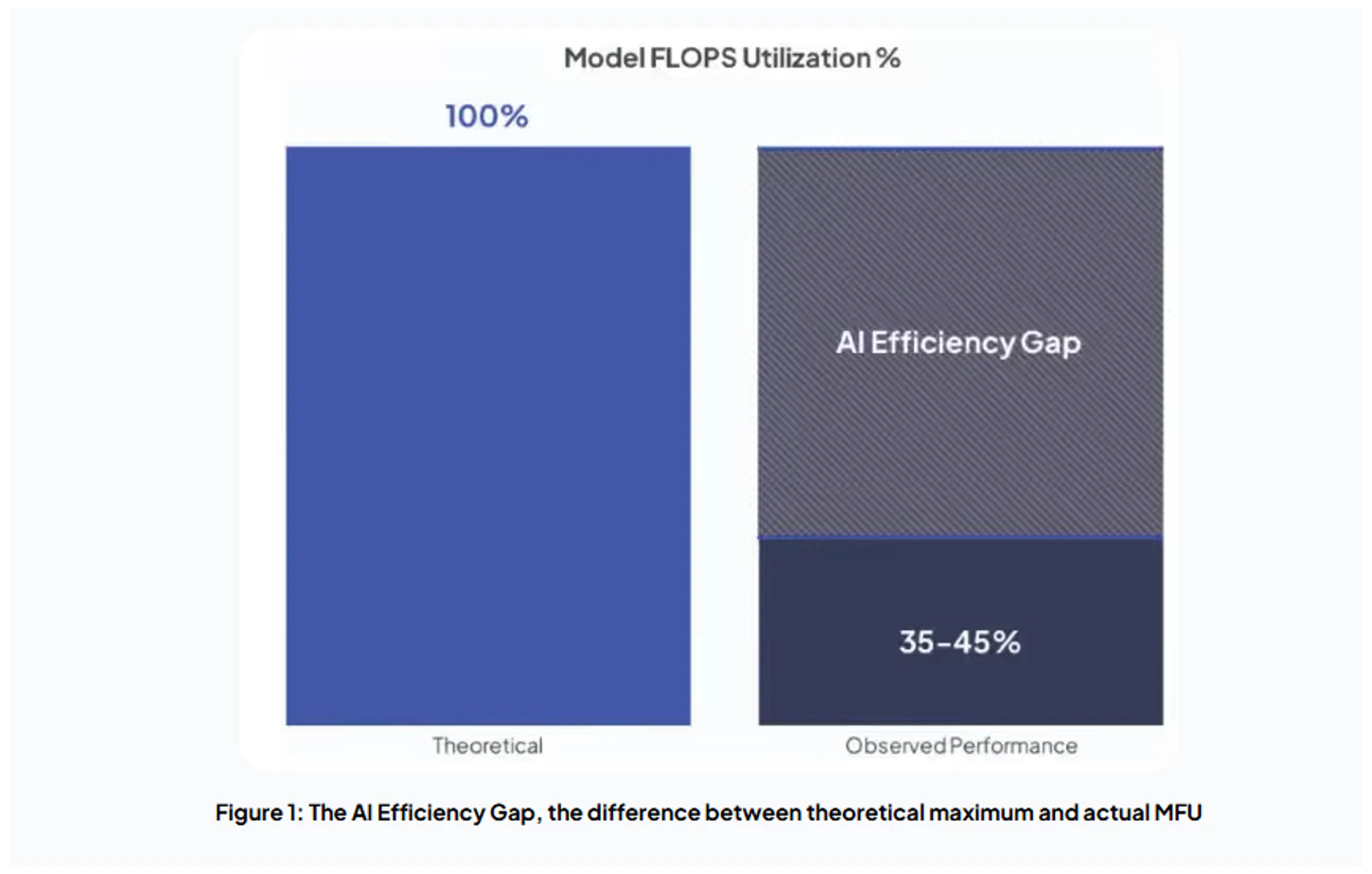

Combining these software and optimization capabilities with rapid fault detection and remediation services, CoreWeave believes it can offer higher GPU utilization rates than hyperscalers, based on the model FLOPs utilization (MFU) metric. The “MFU gap” is a metric that describes the gap between compute capacity and usage, which today often ranges between 30% to 40%.

The MFU gap can become quite costly as it represents a more realistic way to measure the performance of GPUs -- rather than only taking into account if a GPU is sitting idle or not. According to Trainy AI: “GPU Utilization is only measuring whether a kernel is executing at a given time. It has no indication of whether your kernel is using all cores available, or parallelizing the workload to the GPU’s maximum capability.”

Chart comparing theoretical model FLOPS utilization (100%) with observed performance (35%–45%), illustrating a significant efficiency gap in AI workloads. Source: CoreWeave

When going public, CoreWeave published its MFU rate at 35% to 45%, stating it is 20% higher than competitors, which means other AI data centers had MFU rates more in the 30% range. However, in a March 2025 blog post, CoreWeave noted that it was achieving an MFU of >50% on Hopper GPUs. This ability to stand up next-generation GPU hardware in short fashion combined with improved utilization rates is where the neoclouds’ advantage lies.

Behind the Balance Sheet: Why Hyperscalers Are Leasing Neocloud Capacity

By leasing compute capacity from neoclouds, hyperscalers shift their cost timeline from being a large upfront capex outflow to an operational expense outflow spread over long-term contracts. The need to spread costs is becoming increasingly evident due to the massive spending hyperscalers are engaged in.

Although this is the “bear” case on why hyperscalers work with neoclouds—contrasting this with the rationale behind GPU access and utilization is key because one could argue that hyperscalers are quite capable of software optimizations and GPU utilization on their own (in fact, they are the longstanding incumbent here with deep expertise in cloud operations and workload optimizations).

Take Meta for example. Analysts are currently expecting the company to generate $136 billion in cash from operations in 2026. With its stated capex guidance of $125 billion to $145 billion, the company could easily be free cash flow negative during the year. However, as noted, Meta also has up to $62.2 billion in neocloud agreements. If Meta built the equivalent value of capacity itself, the firm would recognize that spending as balance sheet capex, weighing further on its already pressured free cash flow.

On the other hand, neocloud agreements add nothing to Meta’s capex, as the costs are recognized as operating expenses over the life of the contracts. Notably, Meta’s contracts with CoreWeave and Nebius extend through 2031-2032, meaning that opex payments could average less than $10 billion annually.

Looking at Microsoft, we can see a similar situation. In calendar year 2026, the company is guiding for capex of $190 billion, while analyst forecast $200 billion in cash from operations over the same period. If these figures materialize, the company would consume 95% of its OCF on capex. The $60 billion in neocloud agreements, recognized as operating expenses over many years, expands its capacity while keeping that spend off its cash flow statement.

As hyperscalers offload their capex, neoclouds are the ones taking that capex on—resulting in their massive funding needs.

Circular Financing: Nvidia’s Role as an Investor, Supplier, and Demand Backstop

Both Nebius and CoreWeave lend some of their advantage to Nvidia, as it is this partnership with the GPU leader that offers them that ability to be among the first providers to stand up and deploy next-gen platforms such as Blackwell Ultra and now Rubin.

Having Nvidia as a partner also could play a role in helping CoreWeave and Nebius secure funding at much better terms, extending presence and support beyond the hyperscalers to another investment-grade firm with a strong balance sheet and cash flows. Nvidia’s LTM free cash flow was $119 billion, the second highest of any company in the world, only behind Apple. The downside, however, is that Nvidia’s relationship with the two is one of the most identifiable instances of circular financing.

This stems from the multi-billion-dollar investments that Nvidia has made in CoreWeave and Nebius. Notably, Nvidia’s latest $2 billion investments in each company were not its first. Nvidia’s Q1 2025 13F filing revealed a CoreWeave stake worth $896.7 million at the time, while its Q4 2025 13F revealed a $33 million stake in Nebius. Thus, the investment relationship between Nvidia and these firms extends well beyond one year.

Furthermore, in the case of CoreWeave, Nvidia has also provided a significant financial backstop against unsold GPU capacity. Under the agreement with an initial value of $6.3 billion, “in instances where [CoreWeave’s] datacenter capacity is not fully utilized by its own customers, NVIDIA is obligated to purchase the residual unsold capacity through April 13, 2032.” In other words, Nvidia is committed to purchasing unsold GPU capacity if CoreWeave is unable to find another buyer. With an initial value of $6.3 billion, there is the potential that the arrangement could become larger over time.

As Nvidia makes these investments, CoreWeave and Nebius are going right back to Nvidia to purchase large volumes of GPUs - a clear representation of circular financing. By providing a relatively small amount of equity funding, Nvidia secures relationships with these neoclouds that intend to purchase tens of billions' worth of GPUs.

Nvidia could see long-term benefits by supporting CoreWeave and Nebius through their ramp-up phases where cash flow is deeply negative. If the firms can eventually become self-sustainable, Nvidia would have two large-scale customers that it can continue selling its latest systems to for years to come. However, for the neoclouds, the concern is whether they have to continually raise cash into the foreseeable future to build new infrastructure and when that would level out, as revenue lags capex 2:1.

How Neoclouds Are Funding AI Expansion: Debt, Equity, and Circular Financing

Both CoreWeave and Nebius are eyeing rapid ramps in active power – CoreWeave currently has 1GW of its 3.5GW contracted power pipeline active, but it aims to convert the majority of that over to active capacity by the end of 2027, while Nebius similarly has 3.5GW of contracted power and a goal of reaching up to 1GW of connected (active or can be activated upon GPU installation) by the end of 2026.

However, as with all AI buildouts right now, the keywords are “active power” as energy constraints are intensifying across the board.

CoreWeave’s Balance Sheet Challenged, Debt Quickly Rising

CoreWeave’s balance sheet is in a difficult position, as the company looks to rapidly expand its active power footprint at a rate that is not supported by its cash balance and its operating cash flow.

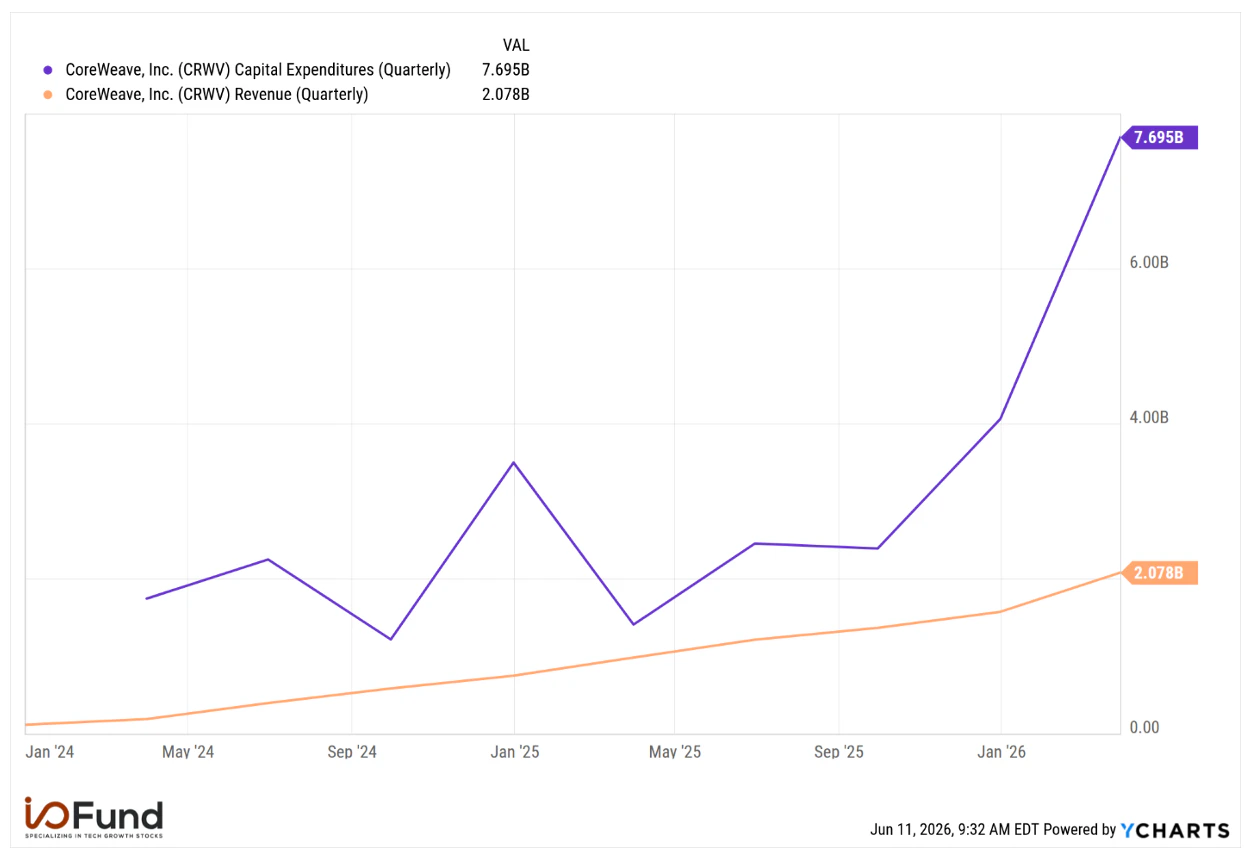

Revenue of $2.08 billion rose by 112% YoY in its latest quarter. However, operating cash flows (OCF) came in at $2.98 billion, compared to capex of $7.7 billion, leading to free cash flow of -$4.71 billion. This mismatch led to the firm’s cash balance falling by $890 million, or 28.3% QoQ to $2.27 billion. Meanwhile, debt increased by nearly $3.5 billion, or 16.1% QoQ to $24.86 billion – this is set to rise further in Q2 as CoreWeave just announced a $3.5 billion senior note raise on June 11.

Chart showing CoreWeave’s quarterly capex rising sharply to approximately $7.7 billion, while revenue reached around $2.07 billion over the same period. Source: YCharts

For the full-year, CoreWeave expects to spend $31 billion to $35 billion on capex, or $33 billion at the midpoint. This implies capex spending for the remainder of the year of $25.3 billion. Analysts currently estimate that the company will generate $8.68 billion in operating cash flow in 2026, or just $5.7 billion for the rest of the year. Given CoreWeave’s $2.27 billion cash balance, this creates a huge funding gap of $17.33 billion. In practice, CoreWeave is likely to raise more than this to avoid further decreasing its already somewhat thin cash cushion.

CoreWeave has used equity issuance in the past as a funding source, but debt issuance far outweighs this. Looking at its first five earnings reports since going public, its total equity issuance is only $3.5 billion, while debt issuance was more than 5X higher at $18.81 billion. Thus, a further increase in debt is likely to be the primary way that CoreWeave continues to fund its capex plans while already having a net cash position of -$22.6 billion. Looking into its unique funding structures shows that debt will continue to be a key lever that the firm pulls.

Nebius: Stronger Balance Sheet but Ongoing Funding Needs

Nebius is comparatively in a much better position, with $9.37 billion in cash to $8.45 billion in debt, for a net cash balance of $920 million. Revenue rose 684% YoY to $339 million in its latest quarter, while operating cash flow was $2.26 billion, rising by 170.7% QoQ due to significant customer prepayments. Capex came in at $2.47 billion, resulting in FCF of -$214.9 million.

However, Nebius is also looking to rapidly expand its active power footprint, with the firm’s midpoint capex guidance for the full year at $22.5 billion. This implies $20 billion in spending over the remainder of the year. Including the company’s cash and contractual commitments of approximately $6.9 billion, Nebius currently needs to draw $6.3 billion in additional funding to support the midpoint of its capex forecast.

Like CoreWeave, Nebius has also leaned heavily on debt rather than equity issuance to fund itself, although to a lesser extent. Since Q4 2024, Nebius’ total equity issuance was approximately $3.92 billion when including the $2 billion in pre-funded warrants Nvidia recently purchased. Over the same period, its debt issuance was $8.32 billion. In its latest earnings call, Nebius noted asset backed financing, corporate debt, and equity issuance as options for raising capital.

Notably, Nebius’ undeployed 25 million share at-the-market equity program could go a long way toward bridging its 2026 funding gap. At a $200 share price (around 10% below the stock’s current level), fully utilizing this program would generate gross proceeds of $5 billion while diluting shareholders by approximately 8%. However, given past trends, asset backed and corporate debt are likely to be the primary path forward.

Overall, this breakdown of CoreWeave and Nebius’ funding requirements for 2026 is just one stage of a much larger push to convert its contracted power into active power. After all this spending, CoreWeave aims to have just under 50% (1.7 GW) of its contracted power active. Meanwhile, Nebius hitting the upper bound of its connected power target would account for less than 30% of its contracted power, which includes power that is either active or can be activated once GPUs are installed.

In turn, the companies will continue to need to find more and more funding to scale until CFO converges with capex. With the spread between these figures still very wide, the likely result is further increases in debt loads and/or shareholder dilution over several years.

GPU-Backed Debt: Inside CoreWeave’s Funding Engine for AI Infrastructure

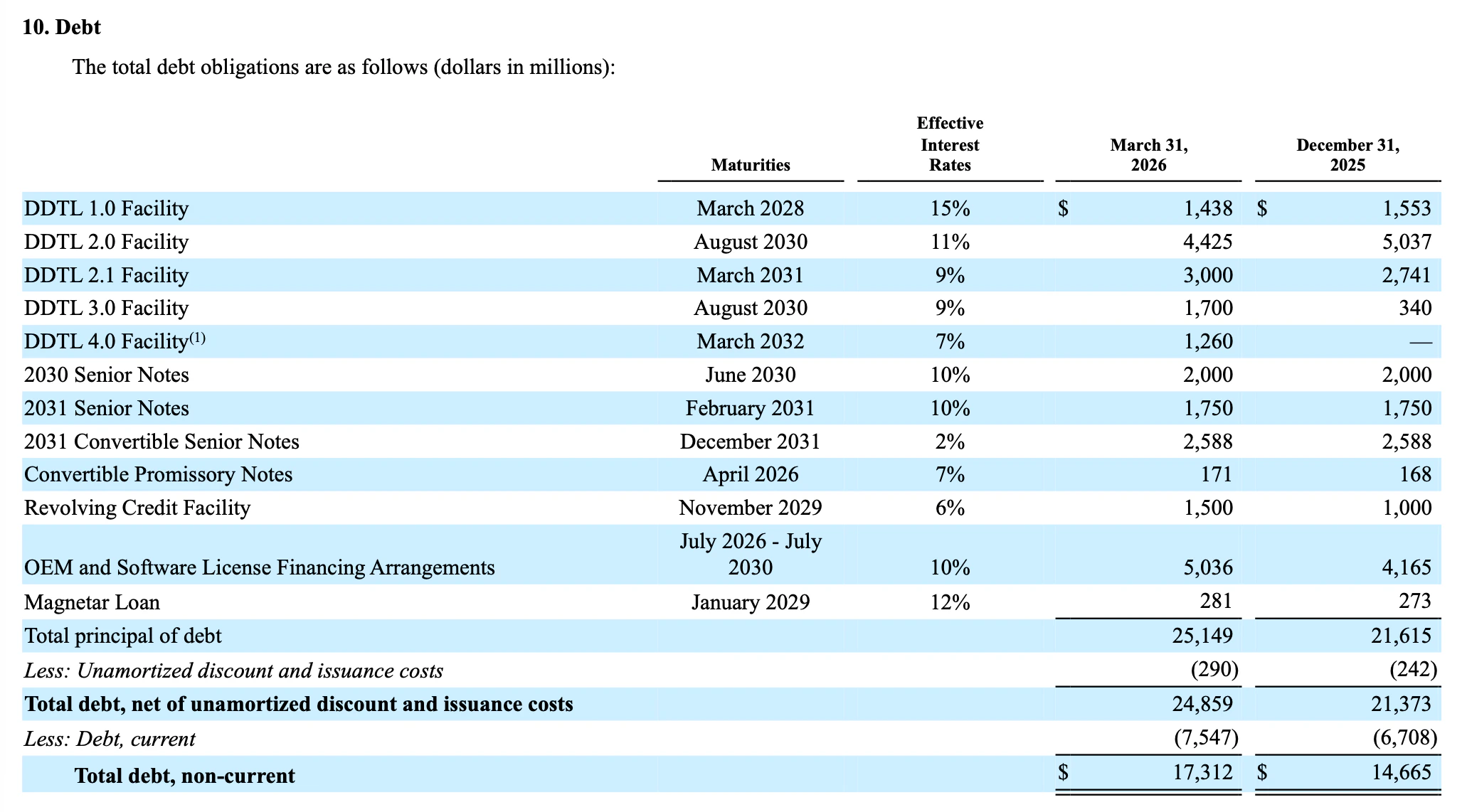

CoreWeave relies heavily on GPU-backed delayed draw term loans (DDTLs), having closed six separate facilities. Under DDTLs, CoreWeave draws down funds intermittently as it uses them to pay for different stages of data center buildouts.

Notably, the company’s $8.5 billion DDTL 4.0, closed in March, was the first of its kind to receive an investment-grade credit rating. As of Q1 2026, CoreWeave had only drawn $1.26 billion worth of DDTL 4.0. This is the only portion of the $8.5 billion that currently shows up in CoreWeave’s total debt. Thus, as the firm draws down more of DDTL 4.0 over time, its debt will also increase.

Table showing CoreWeave’s debt structure with total debt of approximately $25.1 billion, including multiple delayed draw term loan (DDTL) facilities and senior notes. Notably, the DDTL 4.0 facility totals $8.5 billion, but only $1.26 billion has been drawn, indicating significant future debt expansion as capital is deployed. Source: CoreWeave

CoreWeave notes that the investment-grade rating is “supported by a long-term customer contract with an investment-grade AI enterprise," which is presumably tied to Meta’s latest contract. Essentially, the contract that CoreWeave has signed with the investment-grade customer, as well as the value of the GPUs it buys, are collateral for the debt. This is why the facility can achieve an investment-grade credit rating despite CoreWeave itself having a poor balance sheet, allowing for much more favorable interest rates that CoreWeave could not otherwise receive.

Still, CoreWeave's ability to receive better interest rates than peers relies on backing from investment grade customer contracts. Notably, DDTL 5.0, closed in May (and is thus not included in the table above), was backed by two non-investment-grade customer contracts. This resulted in the facility not receiving an investment grade rating and thus having a higher interest rate.

Interest Rate Pressure: A Growing Risk to Profitability

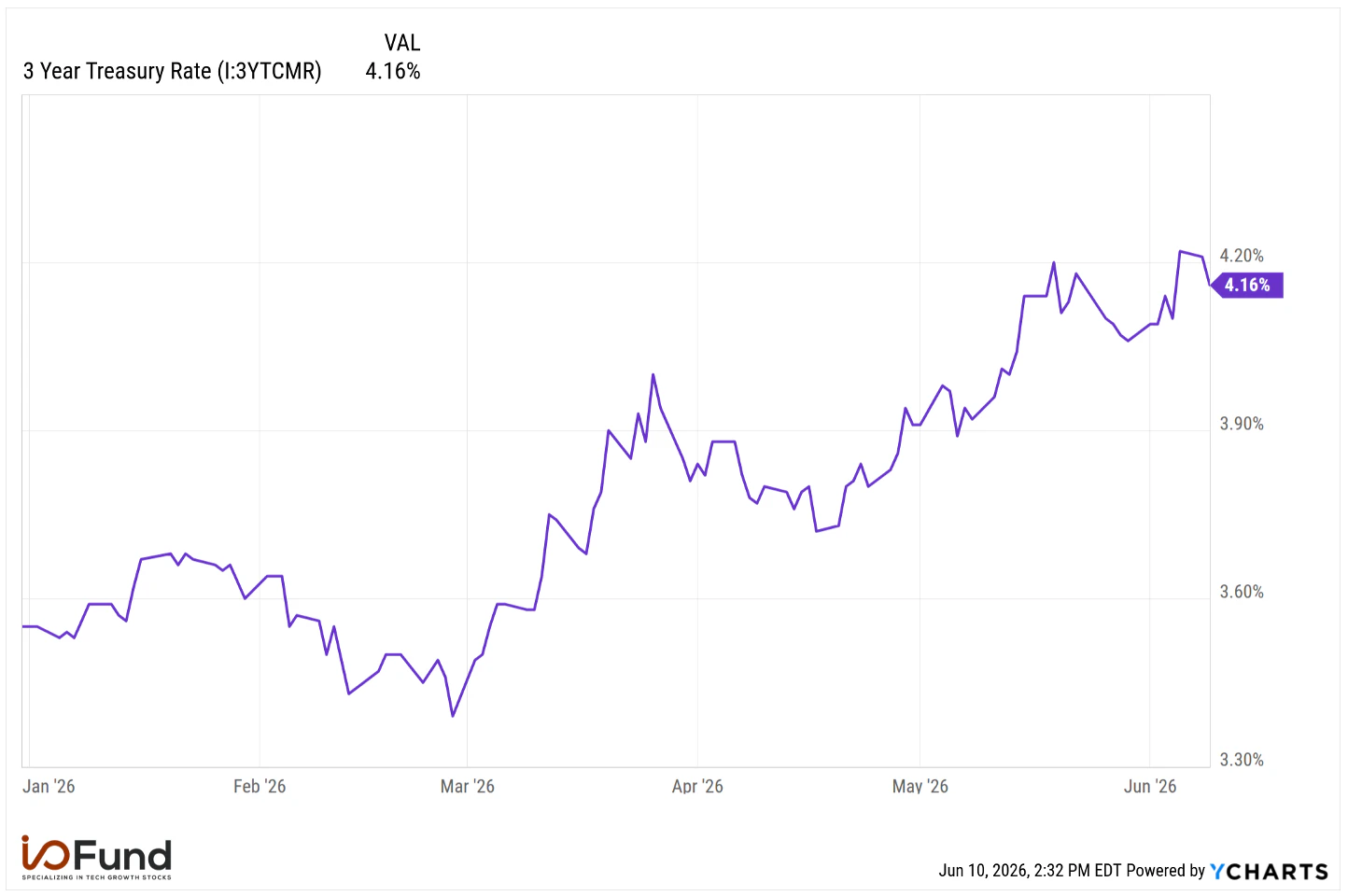

Increases in general rates apply further upward pressure on the rates that CoreWeave and other neoclouds can receive in future funding rounds. The fixed rate tranche of DDTL 4.0 is tied to U.S. Treasuries with an average weighted maturity of 3.14 years, plus a 2% premium. This portion of the yield curve has seen rates rise significantly since the beginning of the year from less than 3.6% to nearly 4.2%.

Chart showing the 3-year U.S. Treasury rate rising from below 3.6% in early 2026 to approximately 4.16% by June, reflecting a sharp increase in short- to mid-term interest rates. Source: YCharts.

Notably, CoreWeave’s interest payments are already elevated, coming in at $536 million in Q1. This equates to 25.8% of its $2.08 billion in revenue, and 46.3% of its $1.157 billion in adjusted EBITDA. The company is guiding for midpoint revenue of $2.525 billion next quarter, and midpoint interest expense of $690 million—which would push its interest to revenue ratio up to 27.3%. With this, interest expense is expected to become an even more relevant line item while already putting significant pressure on profitability.

The Neocloud Race: Balancing Surging AI Demand With Rising Debt and Circular Risk

Overall, neoclouds clearly have significant growth momentum, with revenues and backlogs spiking, while attracting interest from investment-grade hyperscalers such as Microsoft and Meta, and AI labs including OpenAI and Anthropic. Access to leading Nvidia systems, and GPU utilization advantages make neoclouds an option for hyperscalers looking to quickly scale AI compute capacity.

At the same time, the mismatch between operating cash flow and capex is causing debt levels to rise rapidly, which is a dynamic that is unlikely to change in the near term. Elevated interest rates remain an external risk, while circular financing raises questions around the degree to which neocloud growth depends on Nvidia’s capital support, and the extent to which Nvidia’s GPU demand is increasingly tied to the neocloud model.

As Q2 wraps up, I/O Fund is preparing to identify the next wave of AI winners in our upcoming Top 15 AI Stocks for Q3 2026 report, with coverage across AI networking, memory, energy, custom silicon, and the infrastructure bottlenecks driving the next leg of the trade.

Premium Members will also receive upcoming thematic reports on the latest shifts in AI networking and a new catalyst we believe could become one of the more important opportunities in the second half of the year.

We publish more than 100 paywalled articles each year on AI stocks, supported by an actively managed portfolio and real-time trade alerts.

Don’t miss out on the AI trade 👉 Join I/O Fund Premium today.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund own shares in NVDA at the time of writing and may own stocks pictured in the charts.

Leo Miller, AI and Semiconductor Investment Writer at I/O Fund, contributed to this analysis. Leo Miller owns shares of NVDA and META.

👉🏻 Share with a Fellow Investor

Help someone else benefit from this insight.

Recommended Reading:

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per