Alphabet Stock: Search Giant Is Just Getting Started

August 16, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Aug 10, 2023,07:15 am EDT

Given the macro headwinds, not many investors expected the magnitude of the Nasdaq-100’s rally through the first six months of 2023. Going into this year, we were positioned for bottom-line focused investment themes that we felt would be able to deliver earnings growth due to secular demand for its products, and in some cases, be able to reduce costs to maintain profitability.

Big Tech versus Tech Sector earnings

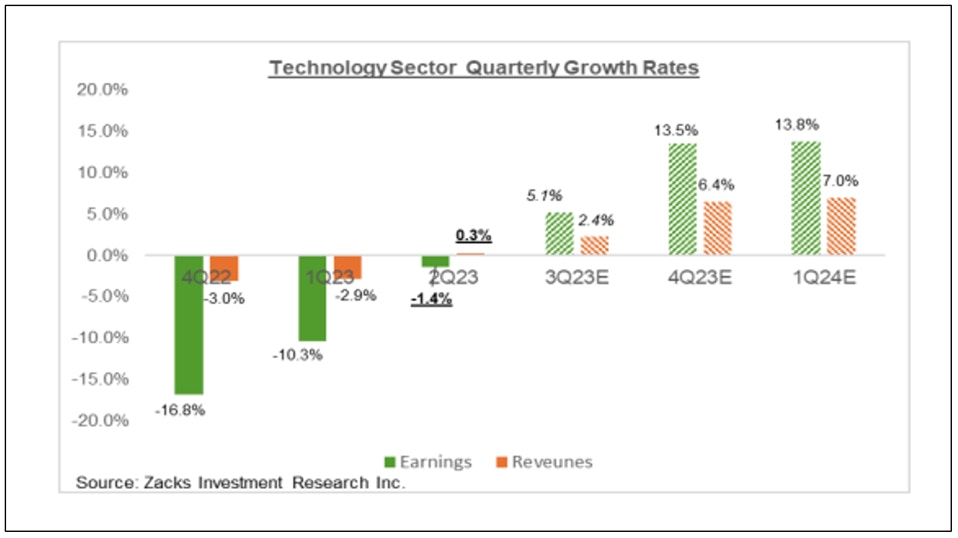

Below is an analysis of consensus earnings estimates from Zack’s on Q2 Technology Sector earnings trends through July 26 plus expectations for the next three calendar quarters.

For the past three quarters, sales and earnings have declined on a year-over-year basis. However, there appears to be stabilization as year-over-year comps get easier and the market is estimating a modest resumption of growth in Q3 and an acceleration in Q4 to Q124.

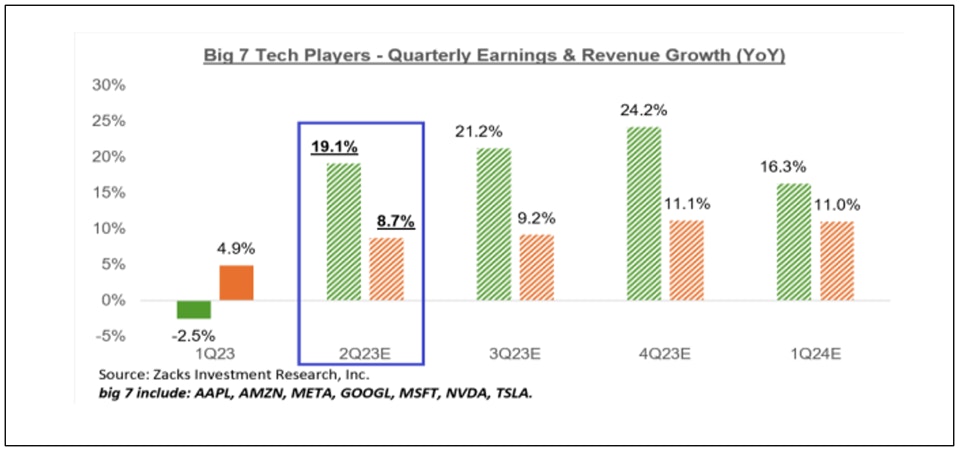

Meanwhile, Zack’s looked at the earnings picture for the “Big 7 Tech Players” - Microsoft, Alphabet, Meta, Nvidia, Apple, Tesla and Amazon. The earnings profile for the Big 7 is estimated to be more robust compared to the overall technology sector.

In addition to a better earnings profile, Big Tech prices and valuations have benefited from other factors that investors are seeking

- Focus on their AI capability and having the financial resources to make the required investments so that they make a positive contribution to future earnings.

- Company size (i.e. large cap) and the ability to manage margins in the face of macro headwinds by meaningfully reducing costs but not at the expense of critical high ROI investments.

- Credit quality - following Fitch Ratings’ downgrade of U.S. government debt to AA+. Big Tech Credit worthiness is on par if not greater than US debt. For example, Alphabet has the same AA+ rating.

Amongst the Big 7, we believe Alphabet stands out for several reasons:

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Year of Execution - Alphabet

Beginning in mid-2022, IO Fund began to transition allocation toward larger cap tech stocks because we felt they are in a better position to navigate a macro downturn. Big Tech has levers at its disposal to manage its margins by rightsizing its cost base. Importantly, at the same time they have the financial strength to make the investments required to capitalize on the AI opportunity and take market share from its weaker competitors. The medium-term bull case is that once revenue begins to meaningfully reaccelerate helped by its AI offerings, the combination of optimizing its cost structure and efficiencies garnered from technology investments leads to expanding margins. This is similar to Meta and its “Year of Efficiency”.

At the moment we prefer Alphabet (GOOGL) over Meta (META). We see a similar story playing out for Alphabet and its “Year of Execution”. We believe it’s in an earlier stage than Meta in its self-help process and its core business areas are just now showing signs of stabilization. Alphabet’s margins are beginning to rebound and have now returned to the percentage they were at in Q1 2022. Meanwhile 1) Resilience in Search, 2) stabilization in YouTube Ads, 3) Market share and profitability gains in Cloud and 4) Growth in Other Google (i.e. YouTube subscription) make us optimistic that revenue will accelerate and there is upside to margins for the remainder of the year.

In the recent Q223 earnings call, management commented on the QoQ strength in margins: “A quick comment on the sequential improvement in operating margins in the second quarter. There are two factors to note. First, the benefit from an acceleration in search advertising revenue growth in the second quarter. Second, the vast majority of the charges related to our workforce reduction and optimization of our global office space were taken in Q1.”

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Search moat is strong

For all the hoopla surrounding ChatGPT and the belief that it will provide MSFT an opportunity to take share from Alphabet’s core search business, it has yet to happen according to Search Engine. According to their analysis, Microsoft is losing market share. It peaked at 9.92% in October 2022 and is now at 7.14%. With its market position firmly entrenched, Alphabet has the audience to roll out its Search Generative Experience (SGE). On its own, the Search business has proved resilient because it provides advertisers an attractive ROI on their ad spend. Looking ahead, SGE will improve advertisers’ ROI and will likely provide Alphabet additional pricing power. This will also improve their retail vertical. Meanwhile, consumer interest will further strengthen Alphabet’s dominant market position in Search.

However, let’s not forget about anti-trust trial

One of the reason we’re very positive on the AI potential for Google’s businesses is that it is sitting on the world’s very best consumer data, which is not an exaggeration in the least bit. Its ability to lead in artificial intelligence and large language models should not be underestimated.

Therein lies the issue. Google undisputedly has the world’s best consumer data, but did this grow to become part and parcel with operating a monopoly? The Department of Justice has asserted anti-trust violations against Google with the trial beginning in September 2023.

We anticipate two outcomes. The antitrust outcome will be mild, and Google will be empowered to continue to dominate. Or, the outcome will require the ad properties to be broken up, leading to a weaker stance for Google. This could benefit smaller ad-tech players, which we have identified and are monitoring closely.

The I/O Fund Analyst Team contributed to this analysis

Recommended Reading:

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per