Palantir Stock Surges From Artificial Intelligence Platform

February 20, 2024

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Feb 15, 2024,04:51 pm EST

Palantir’s Q4 earnings confirmed an acceleration in its US commercial business as it closed out its first GAAP profitable year. Shares are reflecting the optimism surrounding Palantir’s commercial segment and bottom line expansion, with shares up more than 47% YTD and nearly 280% since the start of 2023.

We noted in our stock newsletter in December that Palantir was “exhibiting multiple signs of acceleration heading into 2024 with an improved fundamental backdrop driven by increasing AI demand. Palantir’s Artificial Intelligence Platform (AIP) is driving a significant acceleration in its US commercial business, while underlying metrics and the bottom line are rapidly improving.”

Revenue acceleration stemming from the commercial business is the major story for Palantir through 2024 and into 2025, with revenue growth poised to accelerate from 17% last year to 20% this year and nearly 21% in 2025.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Strong Acceleration in US Commercial Is Driving Growth

In a deep dive at the time of Palantir’s direct listing, our firm said in 2020 that the “commercial sector is the growth story.” Palantir’s public offering was seen as a way to facilitate attracting and acquiring commercial clients before AI brought a wave of competition. The fruits of Palantir’s labor are beginning to pay off, with a newfound rapid acceleration in its US commercial business after AIP’s launch in Q2 was met with “unprecedented” demand. At its core, Palantir’s AIP is a comprehensive AI solution that lets customers lever Palantir’s AI and machine learning tools and harness the power of the latest large language models (LLMs) within Foundry and Gotham. Customers can deploy LLMs on their own private networks using their own private data, maximizing data security and improving efficiency by helping reduce data transfer and storage costs.

Although its US commercial segment accounts for less than 25% of quarterly revenue — it just surpassed a $500 million annual run rate in Q4 — it is now becoming the dominant factor behind the strong business momentum Palantir has seen over the past few quarters.

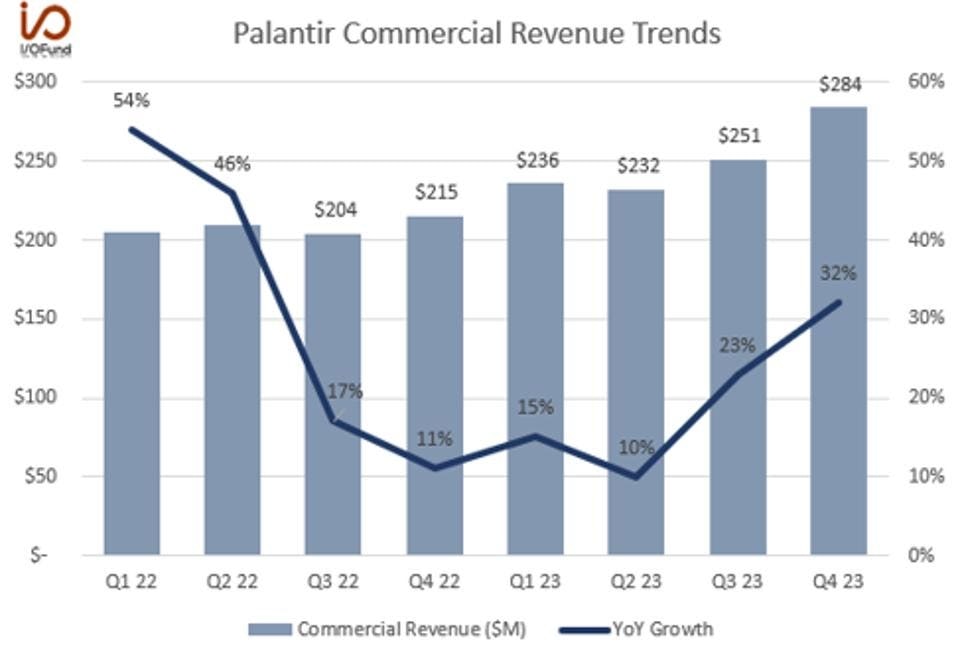

US commercial revenue rose 70% YoY to $131 million, a 37 percentage point acceleration from Q3 and a 58 percentage point acceleration from the year ago quarter. For the full year, US commercial revenue rose at more than double Palantir’s growth rate, increasing 36% YoY to $457 million.

The graph below illustrates just how strong the recent quarter was:

Source: PALANTIR

This acceleration in the US over the past two quarters is driving global commercial revenue higher. Palantir’s global commercial revenue accelerated by 22 percentage points, from 10% growth in Q2 to 32% in Q4. The segment topped a $1.1 billion annual run rate last quarter, up from a $920 million run rate two quarters ago.

Source: PALANTIR

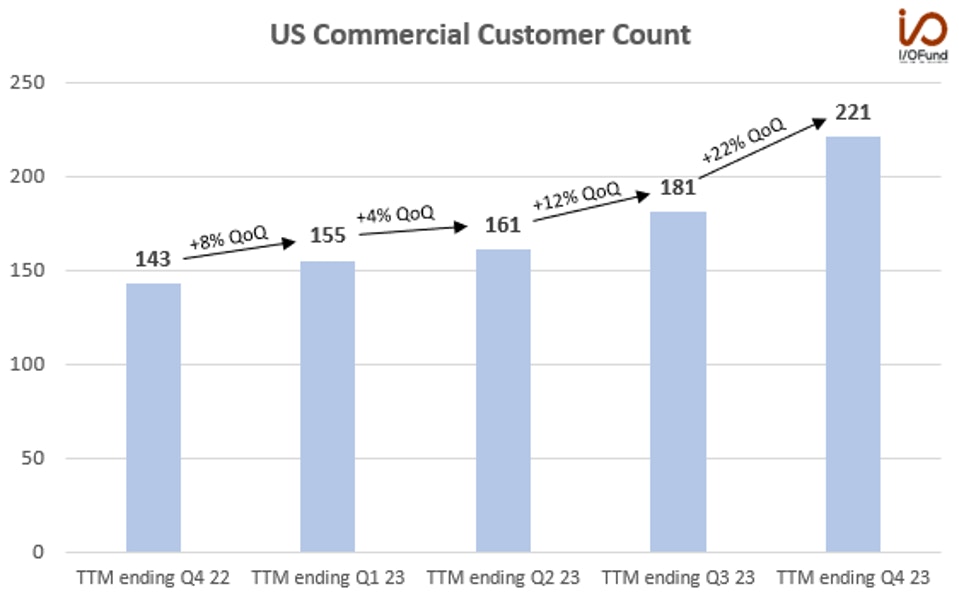

While the revenue acceleration was the main headline for the US commercial business, a closer look reveals that the segment also drove more than 90% of Palantir’s customer additions with very strong underlying metrics.

Palantir reported 55% YoY and 22% QoQ growth in US commercial customer count to 221 in the quarter, as customer growth continues to accelerate. Over the past two quarters, Palantir has added 60 net new US commercial customers with 40 customers added in Q4 alone. This is more than 3X higher than the previous period of just 18 net new US commercial customers from Q4 2022 to Q2 2023.

Source: PALANTIR

Global commercial customers increased 44% YoY and 14% QoQ to 375 customers – representing 45 net new customer additions in the quarter. This means the US commercial segment drove more than 90% of Palantir’s net new customer additions in Q4. That compares to below 63% of net new customer additions in Q3 and just 20% in Q2.

This growth was “meaningfully driven by AIP” with Palantir saying that “demand is off the charts” for its new product. AIP is “propelling growth both through new customer acquisitions and expansions with existing customers,” with evidence of AIP bootcamps “helping to significantly compress sales cycles and accelerate the rate of new customer acquisition.”

Palantir had set a goal in October to hit 500 AIP bootcamps to drive top of funnel growth, and it has already surpassed that target, completing 560 bootcamps in just four months.

CRO Ryan Taylor commented on how this translates through to growth in the US commercial segment, with “70% year-over-year growth in revenue in Q4, 55% growth in customer count year-over-year, and a 107% growth in TCV closed on an adjusted basis […] Either it's — first, it's bootcamps that are quickly converting to paying customers or its expansion of existing customers or it's customers where maybe we've been engaged for a while and introduction of AIP, that whole process has been accelerated. We're seeing that across the board, and yet at the same time, we barely touched that addressable market.”

Engaging customers via bootcamps to then translating that engagement into new customer deals or expanded deals sets the foundation for sustained revenue growth at a higher rate, more so if it can drive its net retention rate higher.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

A Note on Net Retention Rate

Palantir reported a company-wide NRR of 108% in Q4, but noted that it “does not yet fully capture the acceleration in our US commercial business” since customers acquired over the last twelve months are not reflected in the calculation. A majority of the net new customer additions have come in the last two quarters, suggesting US commercial NRR will be higher than 108% come the end of FY24 when this customer cohort is reflected. For context, Palantir reported an NRR of 150% at the end of FY21 in US commercial, but that likely fell significantly when growth slowed to a crawl at the end of FY22.

If AIP can continue to drive a high level of customer acquisition and expansion through FY24, this can help drive and maintain the revenue acceleration we’re seeing in the segment through FY25 and into FY26.

Valuation Remains a Risk Despite Strong Improvement in Fundamentals

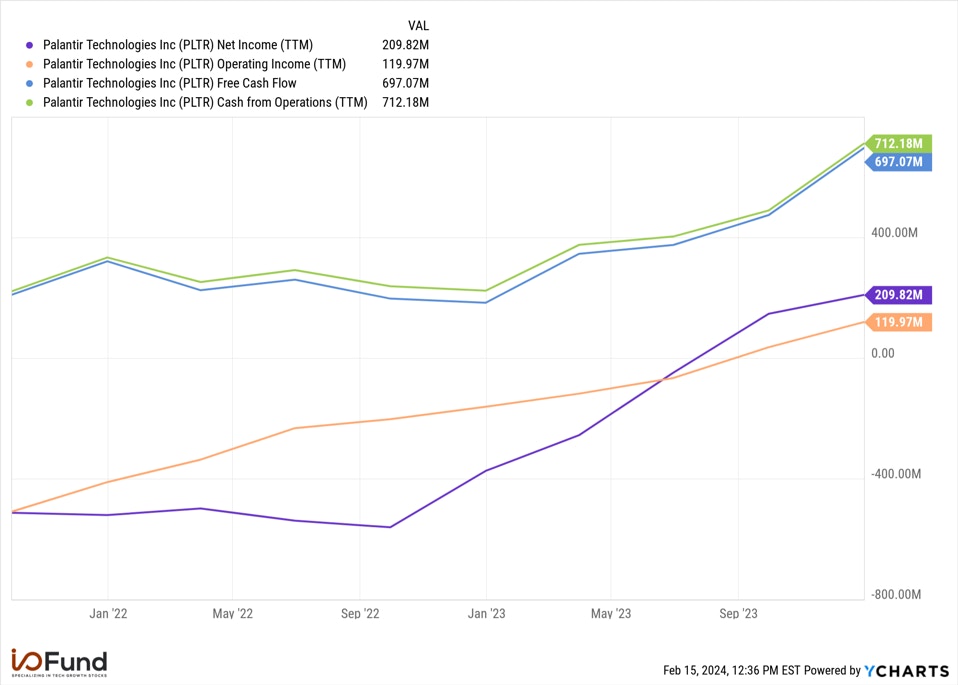

Fundamentally, Palantir has seen major improvements throughout FY23, as it became the company’s first GAAP profitable year.

Gross margin has expanded consistently throughout the year, rising 300 bp YoY from 79% to 82% in Q4. GAAP operating margin shifted positive and expanded in each quarter in 2023, rising from (4%) in Q4 2022 to 11% last quarter.

Net income growth has been particularly strong, with Palantir generating nearly $210 million in net income during the year, compared to nearly ($374 million) in 2022. Cash flow generation has improved substantially, with operating and free cash flow both more than doubling QoQ in Q4 to over $300 million. Palantir ended the year with a 32% OCF margin and a 33% adjusted FCF margin.

Source: YCHARTS

While the fundamentals are certainly supporting an increase in Palantir’s share price, the AI hype may be overshooting the near-term potential for returns at this level. What’s striking is that investors are paying prices last seen when the market set a major top in November 2021, meanwhile the 2021 growth story is decoupled from management’s long-term 30% revenue growth target.

In early 2021, Palantir’s management expected to reach $4 billion in revenue by 2025 as they expected more than 30% annual revenue growth each year for the next five years, or through 2026. Palantir exceeded this target with 34% growth in 2021, but a macro-inflicted deceleration in late 2022 and early 2023 has practically nullified its ability to reach that $4 billion target after posting 24% growth in 2022 and just 17% in 2023. Current analyst estimates point to nearly 21% growth to $3.22 billion in revenue in 2025, meaning Palantir is one year off track – it’s projected to reach the $4 billion milestone in 2026, one year later than expected.

To reach $4 billion by the end of 2025, Palantir would need to record 35% growth this year and next, about 15 percentage points above estimates for both years. While AIP is aiding strong acceleration in the US commercial segment, it’s unlikely to drive revenues to that target. As a result, shares may be pricing in perfection for AIP and AI-related stock performance.

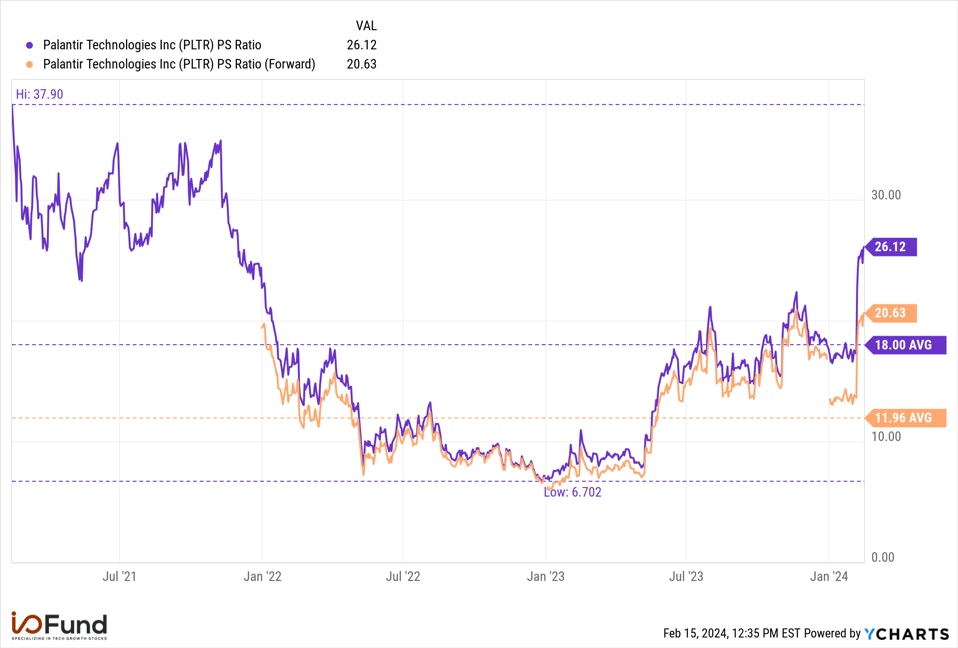

Source: YCHARTS

Prior to Q4’s earnings, Palantir was trading near its average P/S ratio of 18x, but the strong rally has now taken shares to over 26x P/S and 20x forward P/S – this is the highest level since late 2021 yet growth has slowed. On a cash flow basis, shares are trading at around 60x 2024’s projected $800 million to $1 billion in adjusted FCF.

Palantir’s shares are no longer cheap. It’s the third most expensive enterprise software stock on a forward P/S basis, behind Cloudflare and Snowflake, despite having the slowest forward revenue growth rate by more than 700 basis points, at 20% compared to 27% to 30% for the other two. This valuation may open up the door for downside throughout the year as it leaves no room for error, considering its lower revenue growth rate compared to peers; in addition, any dampening to growth stock sentiment from higher-for-longer rates with cut expectations being pushed back further in the year also presents a potential headwind for shares.

Conclusion

Enterprises are showing elevated interest in Palantir’s Artificial Intelligence Platform, which is translating to new customer additions. AIP’s early success in the US commercial segment drove Palantir’s new customer additions in Q4. US commercial revenue is accelerating significantly, reaching 70% YoY growth in Q4 from 33% in the prior quarter.

Management’s commentary about how Palantir is engaging and converting customers via bootcamps sets a foundation for a sustained acceleration thanks to a rapid customer acquisition cycle. However, the size of the US commercial business at less than 25% of quarterly revenues means that the AI-related acceleration may not be enough to sustain the stock’s current valuation.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn About our Premium Services

I/O Fund Equity Analyst Damien Robbins contributed to this analysis.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb

The AI Networking Stock That Beat Nvidia by 7X YTD for Returns of 135% YTD

AI networking stock Lumentum is among the key I/O Fund winners in 2026. We allocated heavily to LITE in January—a month before Nvidia backed the company. While most investors couldn’t stomach taking a

Bloom Energy — Our 2026 Top Pick Was the Best Performing Stock in April

April was the best month in six years for the Nasdaq-100. The single best-performing large-cap stock wasn't Nvidia, Microsoft, or Meta. It was Bloom Energy, up roughly 109% in one month. As you'll rec