Palantir, Three Other Cloud Stocks Poised For An Acceleration In 2024

December 19, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Dec 14, 2023,10:42pm EST

Cloud stocks have been a mixed bag for investors heading into the end of the year, as a handful of names — Confluent, Sprinklr, HashiCorp, Bill, Paycom — plunged following their earnings reports with growth set to slow, while others — Datadog, Elastic, Salesforce – soared on renewed optimism about AI prospects.

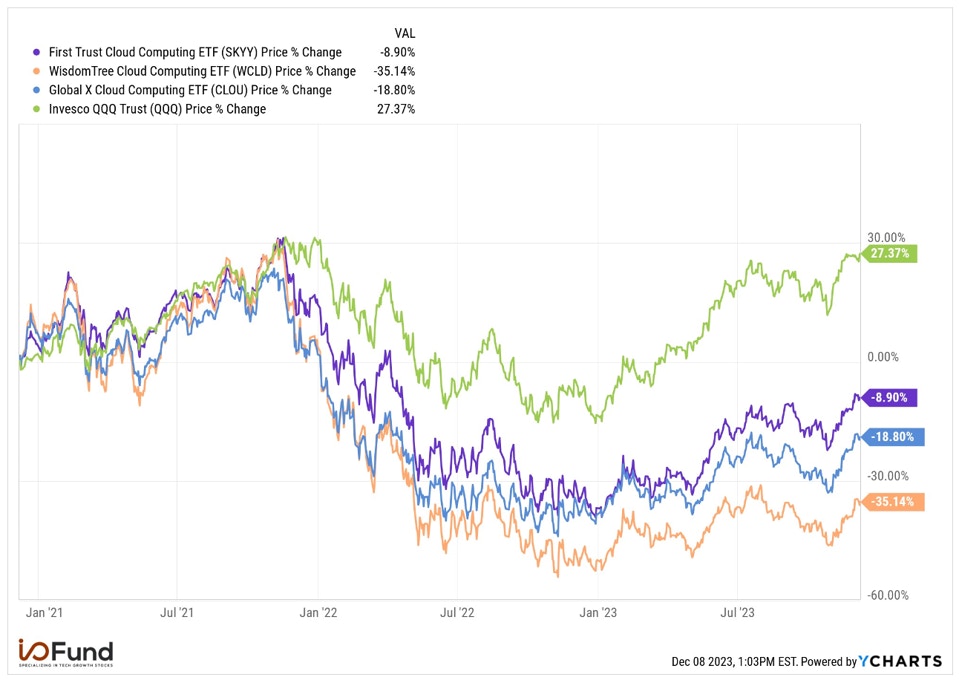

Overall, cloud has lagged broader tech’s rally this year, and on a 3-year basis, returns are still negative, compared to a 27.4% gain for the QQQ. Many cloud darlings in 2020 and 2021 remain far below those highs – take Fastly, for example, where quarterly growth has slowed from the 40% range to the teens, with shares nearly (-80%) lower.

Source: I/O FUND

2023 was a stock picker’s market, and 2024 likely will be as well, with revenue growth rates for a majority of the sector set to slow. Only a few cloud stocks are expected to see revenue growth rates accelerate in 2024. We detail for you the four stocks set to accelerate below.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Palantir

Palantir is one of the Street’s AI favorites this year with a 179% YTD return. The company is exhibiting multiple signs of acceleration heading into 2024 with an improved fundamental backdrop driven by increasing AI demand. Palantir’s Artificial Intelligence Platform (AIP) is driving a significant acceleration in its US commercial business, while underlying metrics and the bottom line are rapidly improving: Palantir posted its first GAAP profitable quarter in February and has since reported four consecutive GAAP profitable quarters.

Customer and US commercial customer growth remains solid, growing 34% and 37% YoY respectively in Q3. CRO Ryan Thomas noted that the US commercial business accelerated in Q3, and excluding strategic commercial contracts, it grew 52% year-over-year and 19% sequentially. Total contract value in the segment increased 55% year-over-year on a dollar-weighted duration basis, with an “acceleration of larger deals and shorter times to conversion and expansion.” He attributed this growth partially to the AI Platform, as the “rapid expansion of AIP at both our existing and new customers, and the impact it is having on their operations is nothing short of remarkable.”

The AI Platform’s growth since its launch in June has also been remarkably strong, with Palantir nearly tripling the number of users in the past quarter, with over 300 organizations using the product in 5 months. Palantir’s profitability is allowing it to continue to “more aggressively invest” in the AI Platform without sacrificing margins, a key differentiator from a majority of cloud AI plays, who are investing in growth at the expense of margins.

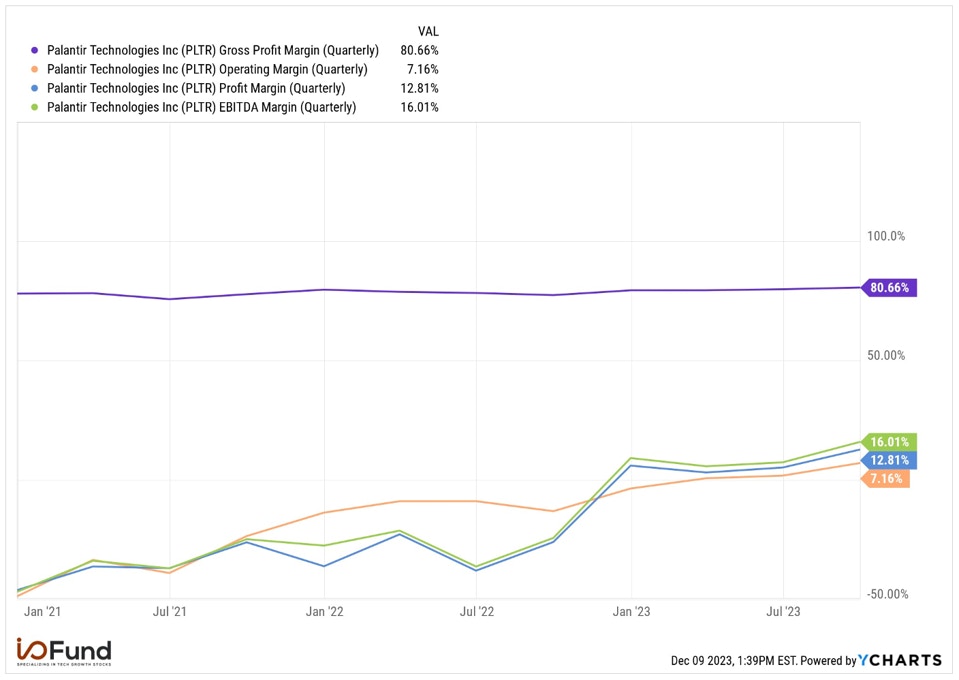

Fundamentally, Palantir is becoming stronger. GAAP gross margin expanded above 80% for the first time in Q3, GAAP operating margin has expanded to 7.2%, and GAAP net margin has risen to 12.8%. Palantir’s EBITDA margin also reached 16% in Q3, its first quarter with a double-digit positive margin, while adjusted free cash flow margin reached 25%. Margins have expanded sequentially in both Q2 and Q3, so the next hurdle will be showing further expansion in Q4 to set up for an increasingly positive trajectory in 2024.

Source: I/O FUND

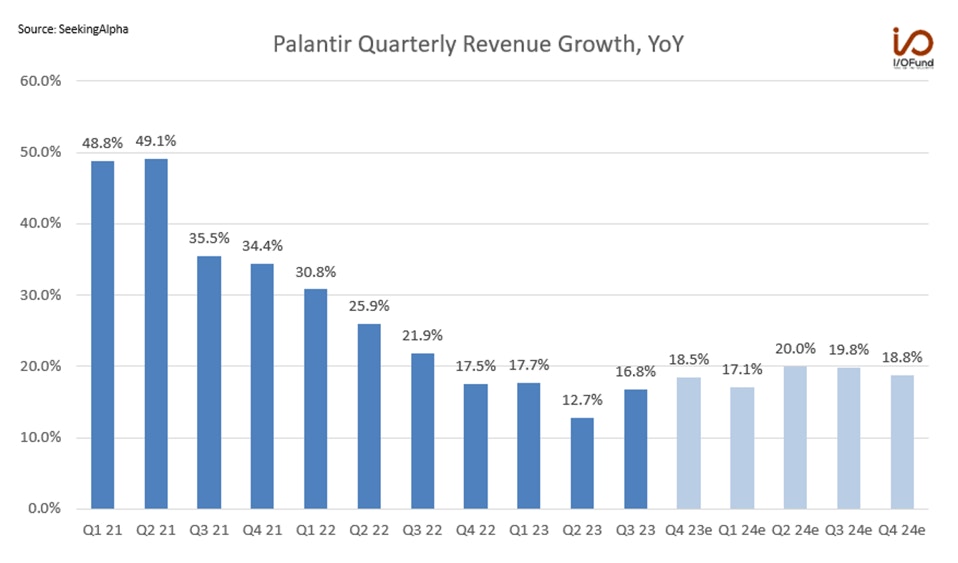

Revenue growth is poised to accelerate in Q4 and through 2024, boosted by AI demand, a reacceleration in Palantir’s US government segment, and continued strength in the US commercial segment stemming from the Artificial Intelligence Platform. Palantir is currently projected to report 18.5% YoY growth in revenues in Q4, the highest in five quarters, pulling 2023’s full-year revenue growth rate up to a projected 16.5%. 2024 is expected to see an acceleration, with current projections pointing to a 320 bp acceleration in Palantir’s revenue growth rate to 19.7% YoY.

Source: SeekingAlpha

Palantir’s underlying metrics support the revenue reacceleration story, but the stock is by no means cheap at 14.2x 2024 EV/revenue and approximately 52x 2024 operating cash flow. Palantir also noted in Q3 that its net dollar retention rate was 107%, with adverse impacts from its European commercial business. This presents a risk that a land-and-expand strategy places more emphasis on signing more customer deals each quarter, and a slowdown in customer additions raises the risk that the expected revenue acceleration won’t pan out as projected.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Shift4 Payments

Payments processing firm Shift4 Payments is not a traditional cloud stock, but it has seen significant momentum within its cloud product, SkyTab, alongside positive momentum in a land-and-expand model for its software offerings. Shift4’s recent M&A activity with Appetize and Finaro are expected to significantly contribute to revenue and EBITDA, playing a role in its 1140 bp projected revenue growth acceleration from 31.3% this year to 42.7% in 2024.

Shift4 says it is currently “in the midst of a very successful consolidation” of SkyTab POS, with some of the success owing to a significant total cost of ownership (TCO) advantage relative to competitors. Shift4 installed 8,254 SkyTab systems in Q3, or more than 35% of its cumulative install volume since its launch. Bringing existing customers over to SkyTab boosts ARPU as it is resulting in higher subscription fees per merchant.

Finaro and Appetize’s acquisitions are expected to be accretive to revenue and EBITDA growth starting this quarter and expanding in 2024. Combined, the two are expected to contribute nearly $25M in gross revenue less network fees and $6M in EBITDA in Q4. With Finaro in particular, Shift4 is expecting “a very strong Q4 ahead” as “numerous enterprise accounts have begun processing.”

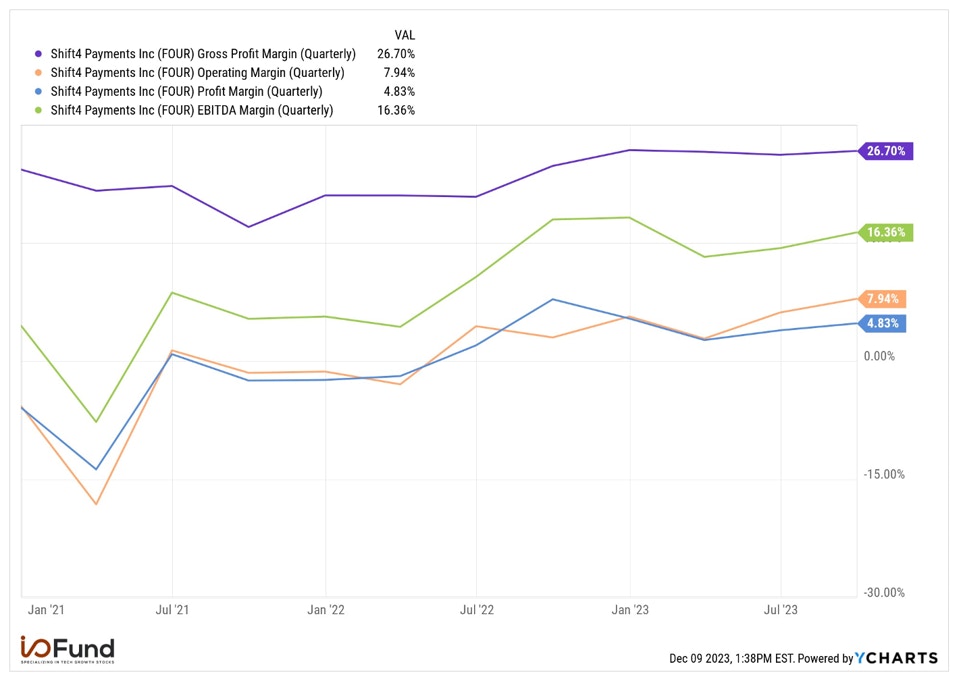

Financially, Shift4 is the strongest of the four, hitting records across a majority of its metrics, from end-to-end payment volumes, revenue, gross profit, and margins. Gross profit rose 34% YoY to $171M and reached a record 26.7% margin, leading to more operating leverage down the line as operating margin expanded to a record 7.9%, up 490 bp YoY. Net margin improved for a second straight quarter to 4.8%, though it remained 310 bp lower relative to a peak at 7.9% in Q3 last year. Adjusted free cash flow grew 69% YoY to $75.5M.

Source: I/O FUND

In 2024, revenue growth is forecast to be >40% YoY in each quarter, from ARPU expansion from SkyTab, net new merchant additions, and contributions from M&A synergies. This represents a rapid acceleration after a four-quarter deceleration, with quarterly revenue growth rates back to levels seen in 2022. However, the main risk to this case is that a pretty swift deceleration is projected in 2025, with revenue growth dropping back to the 28% range. A more uncertain macro backdrop may create some headwinds in 2024 and lead to early signs of a deceleration sooner than expected in late 2024 or 2025.

AvePoint

AvePoint provides cloud migration, management, and data protection solutions primarily for Microsoft 365, with a suite of products and AI/ML offerings for both cloud and hybrid/on-prem workloads. CEO TJ Jiang is aiming for the company to become a “key enabler of generative AI adoption within enterprises in the coming years,” as he believes AI “will drive a wave of enterprise transformation across all industries.”

Generative AI “obviously is playing a part into the future quarters,” according to Jiang. The launch of Microsoft’s Copilot AI assistant for enterprise 365 users serves as a major tailwind for 2024. This boost, alongside a continued shift to the cloud in Microsoft Office’s commercial customer base, is underpinning an expected 70 bp acceleration in revenue growth to 16.4% in 2024 before a stronger 330 bp acceleration in 2025 to 19.7% growth.

Customer expansion can also help this acceleration pan out, especially if advanced talks with large customers can translate to expanded deal sizes in Q4 and early 2024: AvePoint is in talks with a long-time customer to accelerate their cloud migration, another customer is in “advanced talks” to purchase AvePoint’s Opus solution, and a UK customer is considering expanding the scope of their deployment of AvePoint’s Secure Backup Service Solution.

Source: I/O FUND

AvePoint’s financials are improving, though it is not yet GAAP profitable, reporting a GAAP operating loss of ($0.3 million) in Q3, or a margin of (-0.4%). GAAP net margin was (-5.8%), a solid improvement from the (-12%) to (-24%) range reported over the last six quarters. EBITDA margin was 1.2%, the first positive quarter; moving forward, AvePoint needs to keep improving these metrics and post consecutive quarters with positive EBITDA and move closer to GAAP profitability on the bottom line.

Source: I/O FUND

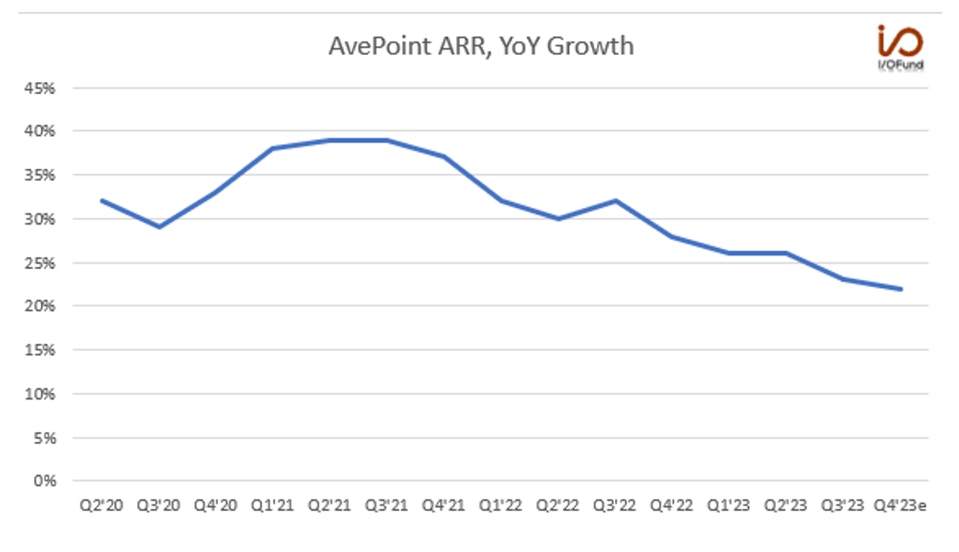

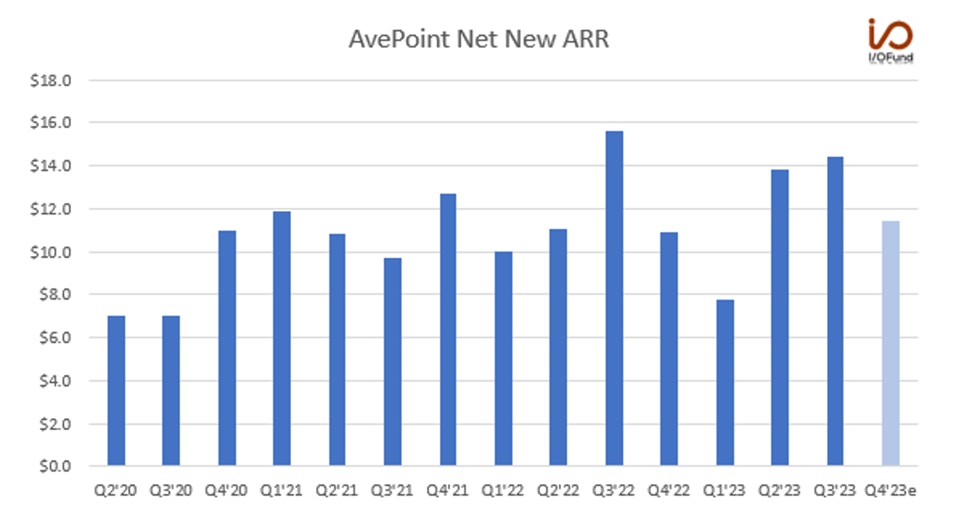

However, there is one red flag, and that’s in AvePoint’s ARR. ARR growth has been decelerating, from the high 30% range in 2021, to 23% in Q3, and now to a guided 22% YoY in Q4 to $262M. The bull case will be looking for this to bottom in Q4, and the company’s history of raising guidance each quarter this year suggests Q4’s ARR growth could come in slightly above the guide at 23%. In addition, Q4’s net new ARR guide is pointing to a sequential decline to ~$11.4M, but management clarified that this stems partially from macro headwinds but also from a spike in government strength and subsequent revenue pull-forward in Q3.

Source: I/O FUND

This guided sequential decline in net new ARR raises another hurdle for the bull case – a resumption of sequential growth in net new ARR in Q1 and Q2 next year will support this view for revenue acceleration. A further deceleration in net new ARR or ARR will raise the risk that revenue growth fails to accelerate YoY.

AvidXchange

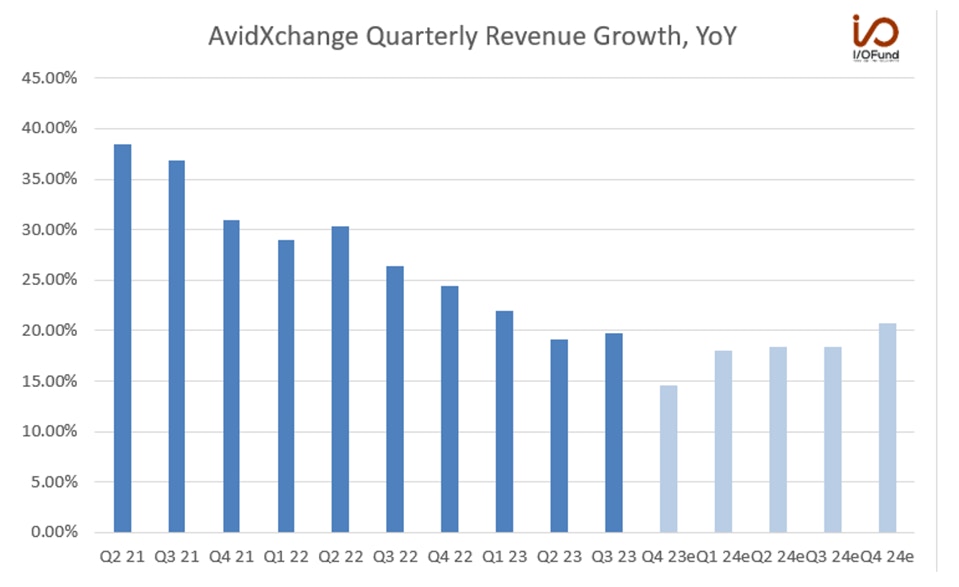

Accounts payable automation and payment solution provider AvidXchange rounds out the list with a minimal 30 bp revenue growth acceleration from 18.6% in 2023 to 18.9% growth in 2024. AvidXchange has posted nine consecutive quarters exceeding its guided outlooks, and this momentum adds a layer of confidence to the acceleration story since a few key metrics continue to decelerate.

Healthy top of funnel growth and a partnership with AppFolio coming online in Q1 next year are two growth levers driving revenue growth higher. AppFolio’s partnership could help drive a reacceleration in transaction volume and payment volume, as AvidXchange will be the first AP application solution in AppFolio with access to more than 19,000 customers.

Fundamentals are improving, but similar to AvePoint, AvidXchange is not yet GAAP profitable. GAAP gross margin is steadily expanding, and is now nearing the 70% level after crossing the 60% threshold in Q1 2022. GAAP operating and net margins improved significantly, by more than 1200 bp sequentially. However, AvidXchange does not yet have the operating efficiency nor leverage to take last quarter’s GAAP net margin of (-8.7%) to GAAP profitability within a few quarters.

Source: I/O FUND

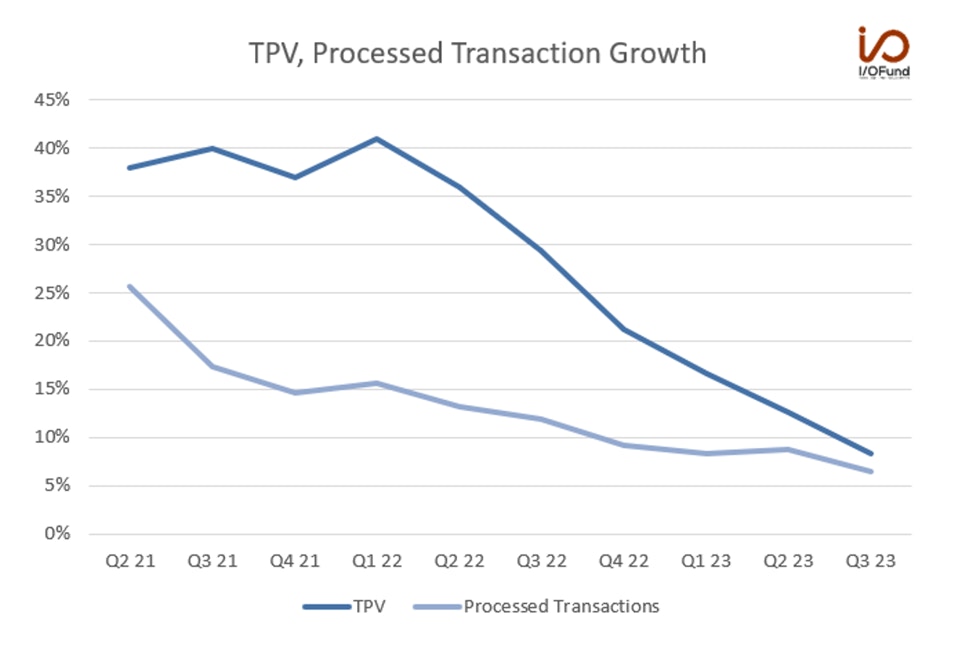

Revenue growth is expected to bottom in Q4 and then accelerate in each quarter next year. Q4’s guide is implying a 500 bp sequential slowdown, so the challenge will be quickly bouncing back to >18% revenue growth. However, this acceleration story comes with two main risks – decelerating growth in both TPV and processed transaction volume. Both metrics have decelerated rather sharply, and have not yet shown signs of stabilizing or reaccelerating.

Source: I/O FUND

Conclusion

Cloud has proven to be a very volatile sector over the past few months. Multiple companies have seen 20% or larger moves in either direction following earnings as investors praised hints of accelerating growth or slammed decelerating metrics. Only a handful of cloud stocks are expected to see revenue growth accelerate in 2024 based on current estimates, and only two of the four covered here have substantial near-term tailwinds from AI, but all are seeing steadily improving fundamentals with a handful of intact growth levers for 2024.

Missing expectations is a risk to any of the four, but more so for AvePoint and AvidXchange given that their expected acceleration is minimal. Palantir’s near 200% YTD surge has been warranted because of a shift to GAAP profitability, but its valuation remains expensive and at risk if growth slows slightly. Shift4 arguably holds the strongest fundamental picture of the four, but a higher degree of risk stems from a quick return to decelerating revenue growth in 2025.

I/O Fund Equity Analyst Damien Robbins contributed to this analysis

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i