Tesla Q4 Earnings Preview: Margins Likely To Slip Again

January 23, 2024

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jan 18, 2024,03:32pm EST

Tesla’s Q4 earnings are on tap after the market close on January 24, closing up a year in which aggressive price cuts helped the automaker top Q4 delivery estimates reach a new record and narrowly beat its 1.8 million volume target. Tesla’s continued actions to improve vehicle affordability throughout the year have been detrimental to margins, as average selling price is falling quicker than production costs.

We covered in the past how Tesla’s lower selling prices in China are having a detrimental effect on margins, as well as assessing how low Tesla’s margins could go. We reiterated after Q3 earnings that this continual decline in margins highlights a broader concern for investors in that Tesla has provided no concrete guidance on how far margins will decline.

Tesla kicked off Q4 with price cuts in the US for some Model 3 and Y versions after Q3 deliveries missed expectations, though it raised prices later in October for the Model Y Long Range and X Plaid AWD. Tesla also increased the price of the Model 3 and Y in China in Q4, reportedly due to rising production costs. Given these pricing trends, ASPs look set to remain pressured in Q4 while production costs may decline marginally, a combination likely to cause margins to slip again.

It is imperative for the bull case that operating margins show sequential improvement in Q1 should it fall to the low 7% range in Q4. Assuming a ~10% QoQ increase in operating expenses, about in line with historical trends, Q4’s operating margin is projected to be ~7.2%, for a ~40 bp sequential decline. The analysis below looks at what investors need to know moving into Q4, and equally important, a few red flags we see going into Q1 and Q2 to keep an eye on.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Automotive Margin Remains a Key Item to Watch

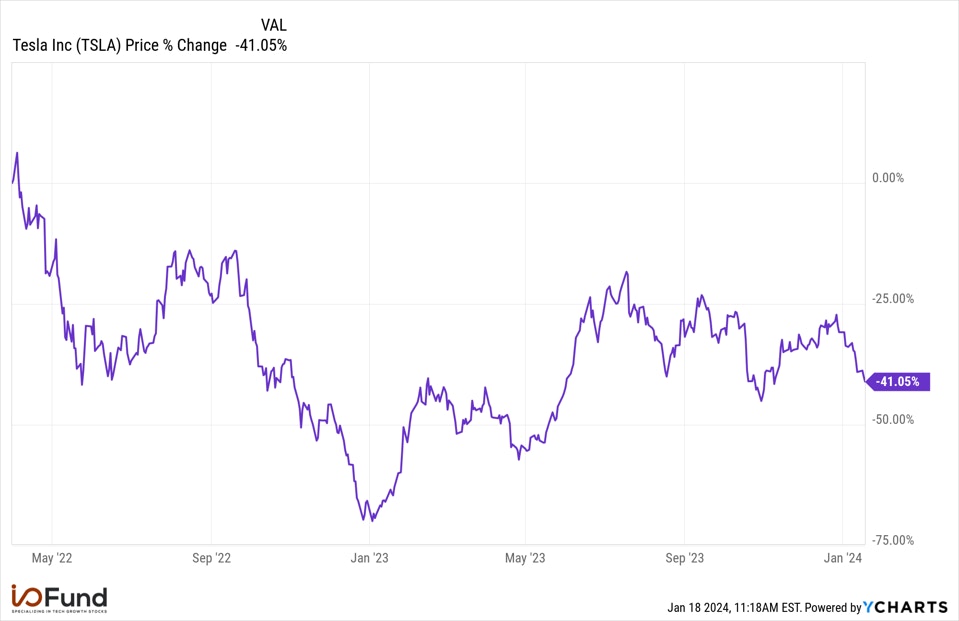

While the promise of full autonomy and its potential value entice some investors, the core story remains margins heading into the Q4 release. Notably, margins topped in Q1 2022, and shares have returned (41.0%) since the end of that quarter.

Source: YCharts

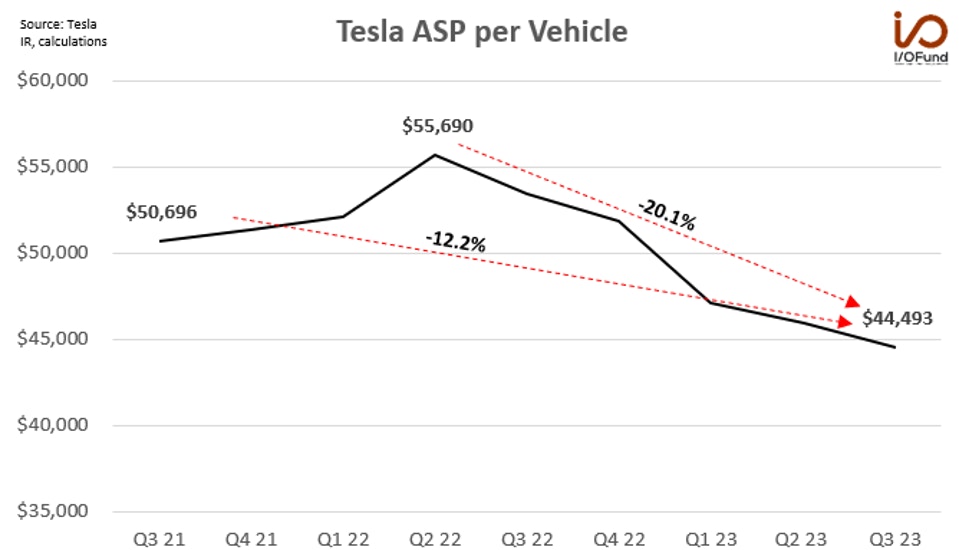

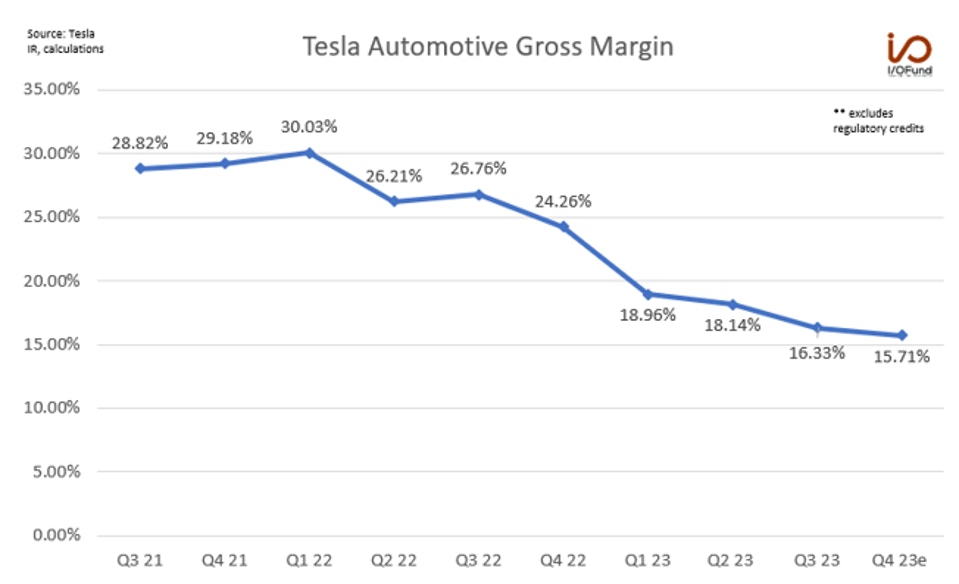

Automotive gross margin excluding regulatory credits topped in Q1 at 30.03%, before slumping to 16.33% in Q3 2023. Quarterly operating margin peaked at 19.21%, before falling to 7.6% in Q3 2023. Wall Street continues to search for a bottom in margins, which look set to decline again based on current trends in ASP and production costs per vehicle.

Source: Tesla, Author Calculations

Aggressive price cuts pulled ASPs below $45,000 in Q3, a level likely to stay in play as recent price hikes for certain models are unlikely to aid pricing given the pace of cuts throughout 2023. Looking forward to Q4, ASP is projected to decline (1%) to (1.5%) sequentially, impacted by recent price cuts and a slightly higher mix of retail sales in China in the quarter, at just over 35% in Q4 compared to 32% in Q3.

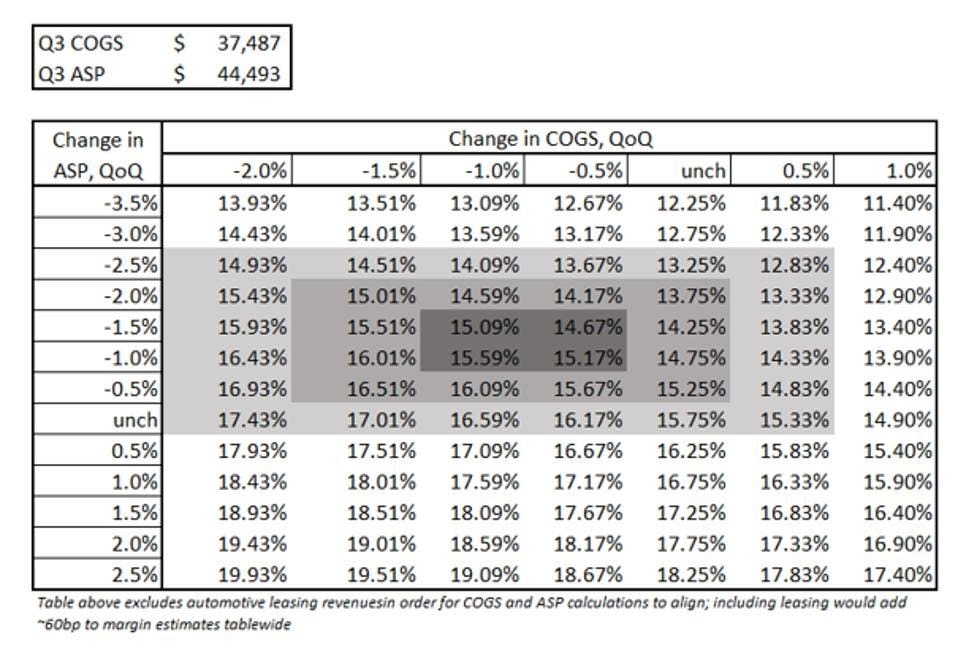

Production costs were reported to have risen slightly in China during the quarter, resulting in a price hike, but Tesla likely enjoyed favorable tailwinds to battery pack cost optimization as lithium prices continued to fall through the quarter. In addition, BloombergNEF estimated lithium-ion battery pack prices declined 14% YoY in 2023 to $139/kWh, with passenger BEV batteries falling to $128/kWh. Based on favorable tailwinds from raw materials prices and headwinds from reports of increased production costs, COGS is estimated to have declined between (0.5%) to (1%) sequentially.

As seen in the scenario analysis below, the incremental effects to gross margin from a 0.5% change in production costs are ~42 bp compared to ~50 bp for a 0.5% change in ASP – therefore, it is critical to margins bottoming that production costs decline faster and/or further than prices, or selling prices begin to increase.

Source: Author Calculations

Our current assumptions point to a slightly larger sequential decline for ASP, an unfavorable combination for margins. For Q4, automotive gross margin is projected at ~15.1%, excluding regulatory credits and operating leasing; including operating leasing, automotive gross margin would project to 15.71%, pointing to a ~60 bp sequential decline from Q3’s 16.33%.

Source: Author Calculations

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Operating Margin May Be Approaching a Bottom

A sequential decline in automotive margin likely spells another sequential decline for operating margins, though there is increasing evidence that operating margins might be approaching a bottom in Q4.

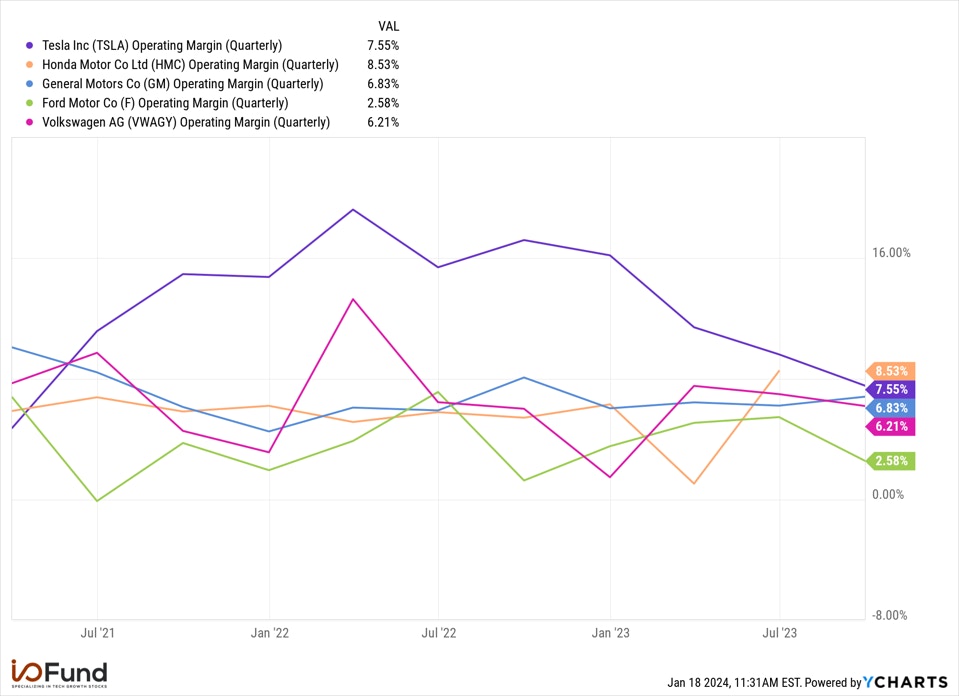

We highlighted in late August via a competitive analysis framework that we believe Tesla’s Q3 operating margins can decline to a level between Honda and VW, or between 7.8% to 9.6%. However, if operating margins were to reach a level closer to — or below GM — that could be sign they’re close to the bottom. This highlights the broader concern for investors in that Tesla has not provided any parameters nor guidance to assess how low margins may go.

Source: YCharts

Q3’s actual operating margin came in below that level, at 7.6%, landing between Honda’s 8.5% and VW’s 6.2%, while still sitting above GM’s 6.8% margin. With automotive gross margin estimated at ~15.7%, company-wide gross margin is expected to hover around 17.5%, assuming a ~180 bp benefit from regulatory credits and positive impact from Energy Storage and Services. Assuming a ~10% QoQ increase in operating expenses, about in line with historical trends, Q4’s operating margin is projected to be ~7.2%, for a ~40 bp sequential decline.

At that level, the spread between Tesla’s operating margin and GM’s would be less than 40 bp, adding evidence that operating margins are approaching a bottom. Aggressive price cuts look to be easing, a tailwind for ASP inflection, while declining lithium and Li-ion battery prices would add production cost reduction, a second tailwind for margins.

It is imperative for the bull case that operating margins show sequential improvement in Q1 should it fall to the low 7% range in Q4. This is crucial for earnings estimates to begin seeing upwards revisions once more, as forward earnings estimates have fallen significantly over the past six months:

- Q4’s adjusted EPS estimate on June 30 was $0.98 for (17%) growth. This was later revised to $0.86 in mid-October for (28%) growth, and the current estimate sits at $0.74 for (38%) growth.

- Q1’s adjusted EPS estimate on June 30 was $1.02 for 21% growth. October’s revision saw adjusted EPS at $0.95 for 12% growth, while the current estimate is pegged at $0.81 for (5%) growth.

- Q2’s adjusted EPS estimate in mid-October was $1.11 for 23% growth, while the current estimate is $0.92 for 1% growth.

Q1’s trajectory, from pointing to over 20% YoY growth to now suggesting a low single-digit YoY decline raises red flags for Q2’s growth forecast, even after a 2100 bp revision lower. Weaker than expected margins in Q4 and/or Q1 could quickly see Q2’s adjusted EPS figure revised lower for another YoY decline. The bull case would need to have concrete evidence of margins bottoming in Q4/Q1 in order to avoid multiple quarters with YoY declines for EPS. Tesla has already cut prices twice in January, by (3%) to (6%) on the Model 3 and two Model Y variants in China, followed by (4%) to (8%) cuts on Model Y variants across Europe. This raises the risk that ASPs fall much further than COGS in Q1, driving a sequential decline in margins and adding more uncertainty to when and where margins will bottom.

Near-Term Focus on Volume Growth

CEO Elon Musk emphasized in Q2 that Tesla is focusing on volume growth at the detriment of margins, based on his view that unlocking full autonomy will lead to a substantial increase in the value of each vehicle and therefore for Tesla: “it does make sense to sacrifice margins in favor of making more vehicles because we think in the not too distant future, they will have a dramatic valuation increase.” CFO Vaibhav Taneja reiterated this in Q3, saying Tesla is “focused on reducing costs, maximizing delivery volumes, and continuing making investments in the future.”

Q4’s production of 494,989 took FY23’s total production to 1.85 million vehicles, while deliveries of 484,507 took the full year’s total to 1.81 million vehicles — this represented delivery growth of 38% YoY and production growth of 35% YoY.

This focus on volume growth via price cuts comes as Tesla is increasingly at risk of losing its title as the world’s largest BEV manufacturer on an annual basis, after losing the title on a quarterly basis this quarter to BYD. BYD has extended its lead against Tesla in China, especially so in Q4, proving that it can’t be ignored as a fierce competitor on the global stage.

BEV sales for BYD increased 22% QoQ in Q4 to reach 526,409 vehicles, almost 9% higher than Tesla’s total. BYD had nearly matched Tesla’s deliveries in Q3 as both held ~18% of the global BEV market that quarter, and BYD’s rapid growth allowed it to take the throne in Q4. Annually, BYD’s BEV sales came in at 1.57 million, +73% YoY, putting it on track to challenge Tesla’s annual volumes in 2024.

Tesla Technical Analysis

Many of the FAANGs are in the final throes of very mature long-term, uptrend patterns, some of which started in 2009. Many FAANGs are either at all-time highs, or just shy of them; however, Tesla trades roughly 50% lower than its 2021 highs, which signals relative weakness compared to other FAANGs.

Source: TradingView

It’s worth noting the head and shoulders pattern that is close to confirming. This is the red count above, which implies that if Tesla breaks below $203, then the lower target will be sub-$100, as we likely press below the January 2023 lows.

If Tesla is going to have any chance at a sharp uptrend, it would need to break above $264 and $280 in a vertical manner. If this happens, we can start discussing the possibility of $345 - $400. This is the green count in the chart, and it has a low probability of manifesting.

The problem with this scenario is that no FAANG supports this type of move. This would be a 60% - 80% move higher in Tesla. Most FAANGs look like they have topped or have one more minor swing higher before topping.

Even the strongest FAANGs are suggesting a final push higher that doesn’t fit with the above green count. META, being one of the stronger FAANGs, only has room for a 4% - 10% move higher before completing a mature 5 wave pattern off the January low completes. NVDA, being the strongest FAANG, only has room for a 5% - 18% move, at most, before it becomes a better buy at lower levels. Therefore, neither the fundamentals, nor the technicals support this type of large move higher in Tesla, which makes the red count more likely at this time.

Conclusion

The main story for Tesla through 2023 and now entering 2024 has been when and where margins will find a bottom. Margins have declined significantly as Tesla prioritized growing delivery volumes via aggressive price cuts – automotive gross margin has fallen nearly 1400 bps in six quarters, while operating margin has pulled back to the mid-7% range. The two are both projected to slip again in Q4 as price cuts are expected to offset any incremental margin benefits from lowering vehicle production costs.

This rather rapid decline in margins is having a direct impact on forward earnings estimates, with Tesla now expected to report a single-digit YoY decline in fiscal Q1 and almost zero growth in fiscal Q2, compared to prior views for >20% YoY growth. Operating margins are nearing a level where we believe it will find a bottom, while more constructive pricing action through the rest of 2024 and/or continued improvements in lowering production costs will also help aid margin recovery.

If you own Tesla stock, or are looking to own Tesla, we encourage you to attend our weekly premium webinars, held every Thursday at 4:30 pm EST for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

I/O Fund Equity Analyst Damien Robbins contributed to this analysis.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su