Top 10 Tech Stocks of 2025: How the AI Trade Defied the Skeptics

January 08, 2026

I/O Fund

Team

The stock market in 2025 was a high-stakes tug-of-war between geopolitical tensions and the AI trade. Headlines were dominated by the DeepSeek fears, trade wars, tariffs, and persistent whispers of the AI bubble. However, the AI trade proved to be more than just hype; it became a cornerstone of the market. Defying the skeptics, the market wrapped up another year of growth with the Nasdaq-100 index finishing up 20.2%, the S&P 500 rising 16.4%, and the Dow Jones Industrial Average gaining 13% in 2025.

We think it’s important to pause and draw parallels among the stocks that performed well in 2025 to form an opinion on what might perform well in 2026, as many of the year’s top performers shared similar fundamental improvements or had similar thematic tailwinds, such as AI.

Below, we review the top 10 tech stocks of 2025, selected based on their price action, fundamentals, and presence within leading tech themes. Choosing a top 10 means many great stocks were left off this list, yet this sample helps form conclusions about how 2025 shaped up versus past years, centered on leading, core thematic opportunities.

Read about our Top 5 Stocks from 2024 here, 2023 here and from 2022 here – many of which went on to lead the following years.

SanDisk (SNDK): The S&P 500’s Top Performer of 2025

SanDisk has claimed the crown as the S&P 500’s top performer, delivering a stunning 559.4% return that outpaced the broader market by a wide margin. The storage pioneer, which launched the first solid state drive (SSD) in 1991, is now capitalizing on the exponential demand for AI flash storage products. Western Digital bought SanDisk in 2016 and spun it off in February 2025. The rally this year was fueled by a "perfect storm" of strong fundamentals and technical catalysts: a massive spike in demand for AI flash storage and the stock’s inclusion in the S&P 500 index in November. The latter triggered a wave of mandatory buying from index-tracking funds, catapulting the stock to the top of the leaderboard.

SanDisk’s revenue growth has accelerated over the last three quarters, primarily driven by the strong demand for flash storage in AI data centers. AI workloads require massive volumes of high-performance, reliable storage, directly boosting demand for the company’s NAND flash products. In addition, the company is benefiting from a tightening memory market and has recently raised the NAND flash prices by a significant 50% for November.

mid

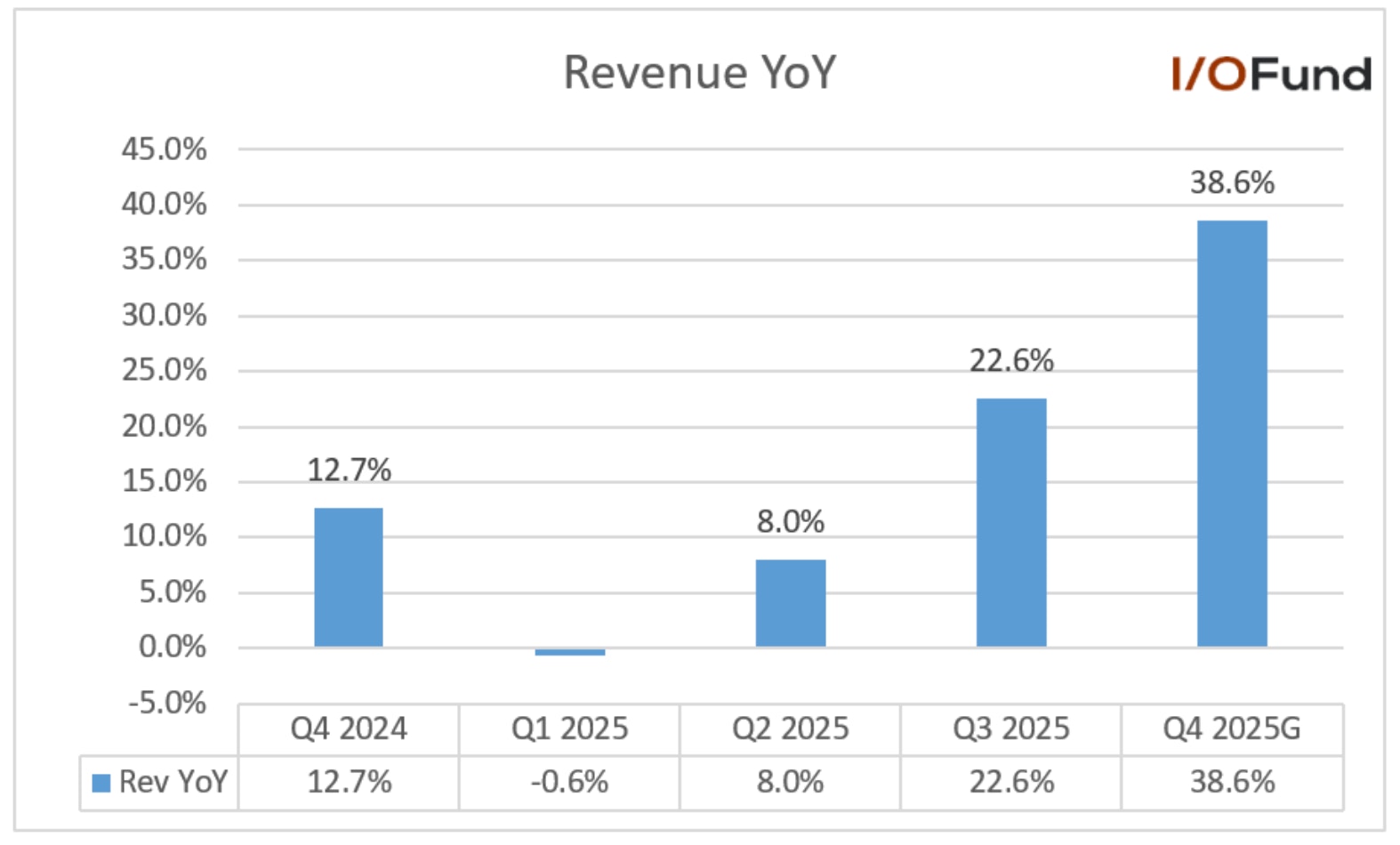

The company’s Q3 revenue grew by 22.6% YoY and 21.4% QoQ to $2.31 billion. The revenue growth accelerated by 14.6 percentage points from 8% growth reported in Q2. SanDisk had also reported an acceleration in Q2 revenue growth by 8.6 percentage points. The company’s Q4 guidance of $2.60 billion implies a YoY growth of 38.6% and 12.7% QoQ, marking the fourth consecutive quarter of YoY revenue growth acceleration, reflecting robust AI-driven demand and improved pricing.

SanDisk reported 22.6% YoY revenue growth in Q3 2025, signaling accelerating momentum as the data center demand boosts AI storage super cycle

Source: Seeking Alpha

The company’s margins have also expanded sequentially this year on higher memory prices and better product-margin mix, though margins were down YoY in Q3. The company also guided strong margins for the next quarter, with gross margins expected to expand 12 percentage points QoQ and 9.5 percentage points YoY to 41.8%, primarily reflecting higher prices. Strong free cash flow generation enabled SanDisk to reach a net cash position, six months ahead of its February Investor Day target.

SanDisk’s rally this year has been underpinned by genuine fundamental improvement, including accelerating revenue and expanding margins. While index inclusion increased the upside, the company’s pricing power and exposure to AI-driven storage demand suggest its performance is grounded in durable fundamental tailwinds.

Bloom Energy (BE): Solving the AI Data Center Power Bottleneck

Bloom Energy emerged as one of the standout stocks of 2025, with a return of 291.2%. The market increasingly recognized its strategic role in addressing one of AI’s biggest bottlenecks: reliable, scalable power. Bloom Energy is a beneficiary of surging AI data center demand, particularly as hyperscalers race to procure clean energy amid grid capacity constraints, as its fuel cells are very efficient and are currently producing 10x power within the same footprint than produced previously a decade ago.

Major highlights include signing a deal in July with Oracle to supply fuel cells for Oracle’s Cloud Infrastructure data centers. Similarly, in October, the company announced a $5 billion strategic partnership with Brookfield Asset Management to become the preferred on-site power provider for Brookfield's global artificial intelligence factories. Due to robust AI demand, the company also plans to double factory capacity to 2 gigawatts a year by the end of this year.

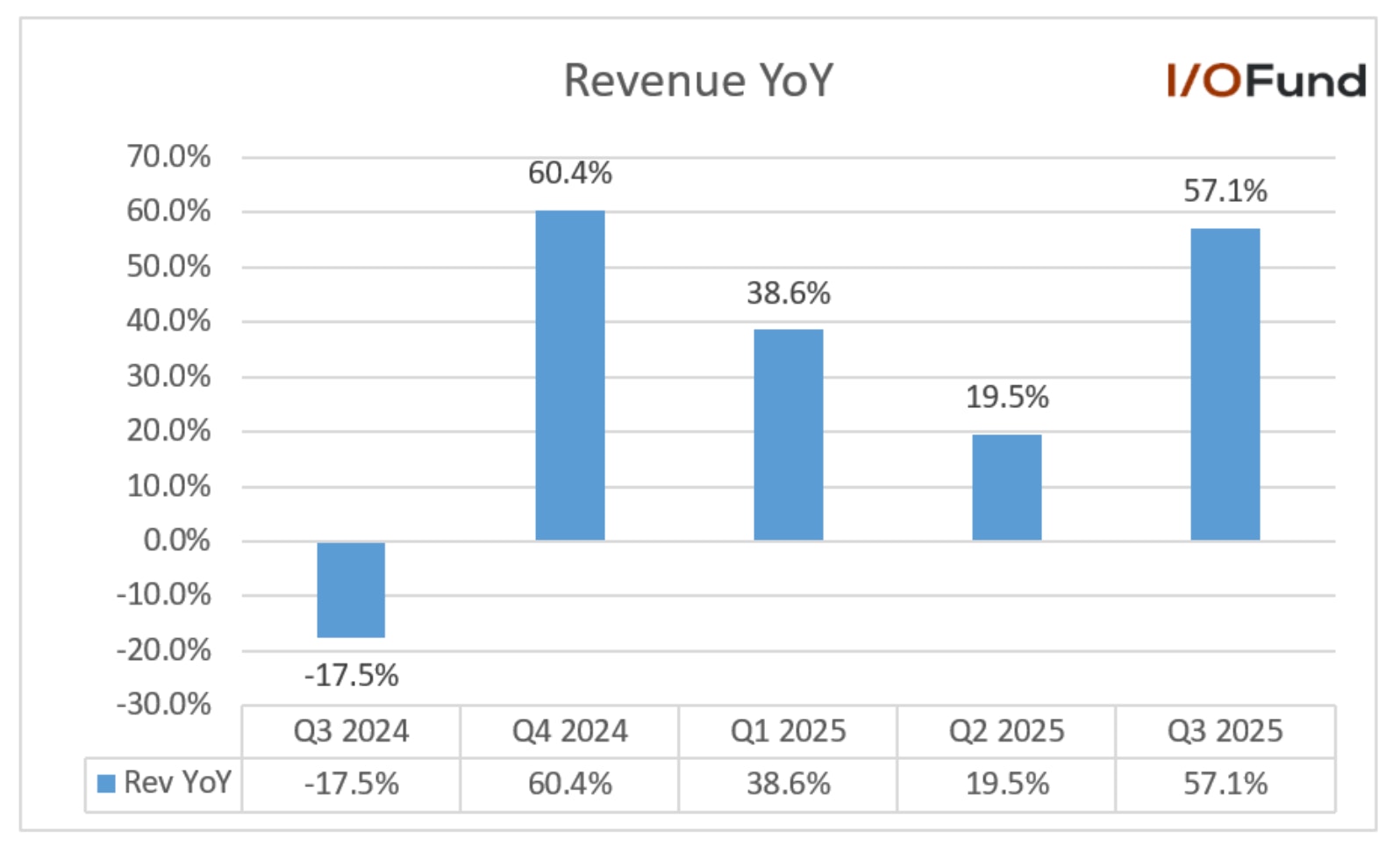

Bloom Energy’s Q3 revenue grew by 57.1% YoY and 29.4% QoQ growth to $519.1 million, accelerating 37.6 percentage points from the previous quarter’s YoY growth of 19.5%. The company’s fourth consecutive record revenue was driven by strong demand for its fuel cell technology powering AI data centers.

Bloom Energy (BE) is reporting record revenue driven by strong demand for its fuel cell technology powering AI data centers. The chart illustrates a significant turnaround from a (–17.5%) decline in Q3 2024 to 57.1% growth in Q3 2025.

Source: Company IR

Bloom Energy’s margins are improving, primarily driven by operational efficiency, product cost improvements, and operating leverage. Bloom Energy is fundamentally transforming into a stronger company, as its GAAP operating margins were previously deep in the red, in double digits. Similarly, the company reported positive operating cash flows and free cash flows in Q3, after reporting negative cash flows in the first two quarters of the year. Strong cash flows are expected in Q4, further boosting investor optimism.

Western Digital (WDC): #2 Best Performer of S&P 500 Driven by AI HDD Demand

Western Digital stock sprang a major surprise, ranking as the second-best performer in the S&P 500 index with a return of 282.3%. The company’s CEO, Irwing Tan, highlighted the company’s niche during the Q3 earnings call, “Data is the fuel that powers AI and it is HDDs that provide the most reliable, scalable and cost-effective data storage solution, playing a vital role in storing the ever-increasing zettabytes of data created by the AI-driven economy.” The company is benefiting from robust demand from hyperscalers for its higher-capacity hard disk drives. Western Digital has solid visibility, and 5 of its large customers have placed purchase orders covering all of 2026, while one of its largest hyperscale customers has signed an agreement covering all of 2027.

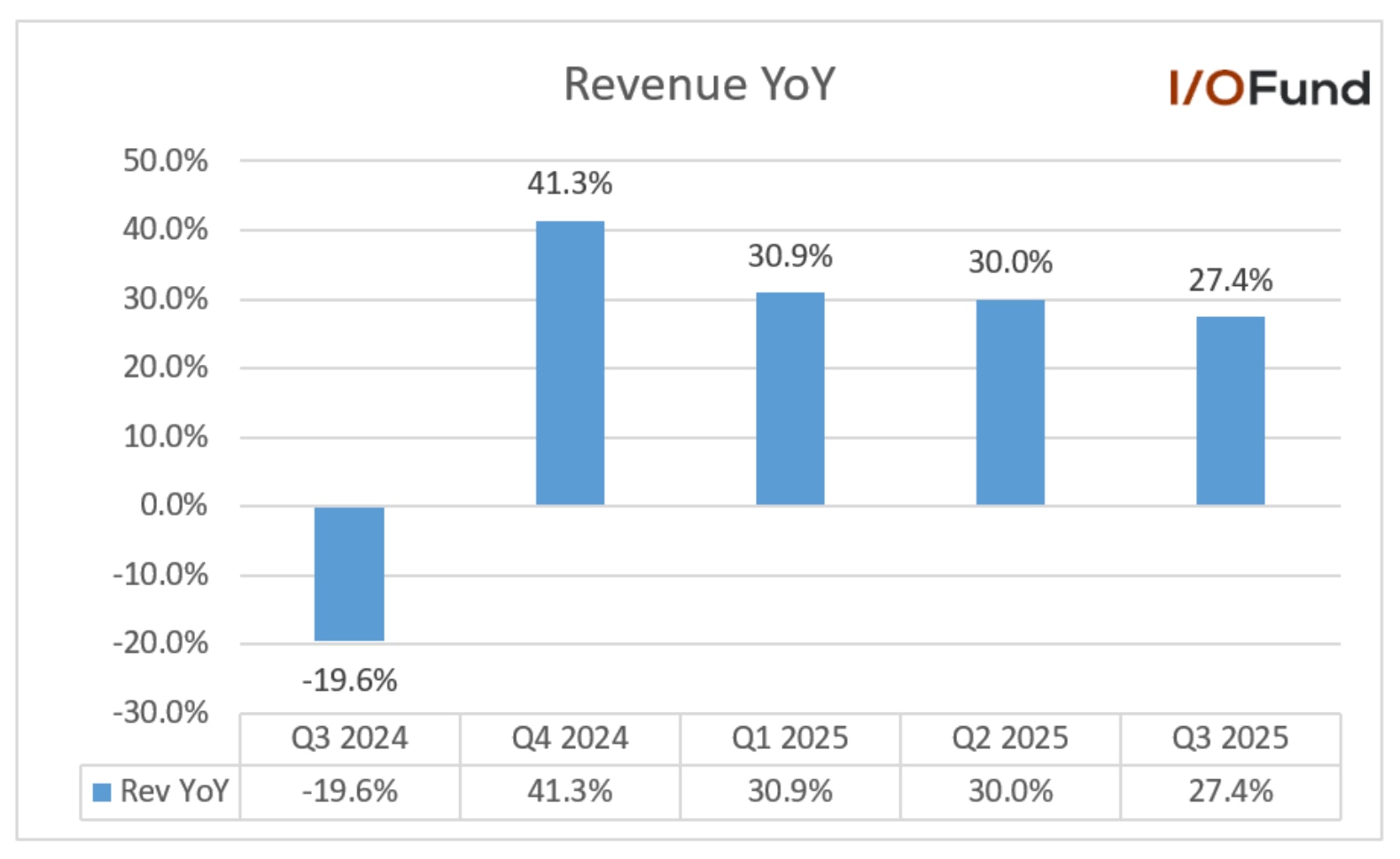

The company’s Q3 revenue grew by 27.4% YoY to $2.82 billion. The AI-related demand has turned the company’s fortunes, and it has reported its fourth consecutive quarter of YoY growth after a dull run of 10 consecutive quarters of negative growth. Margins are witnessing a turnaround, with gross margins improving by 710 basis points YoY and 250 basis points QoQ to 43.5%. The improved gross margin was primarily driven by a better product mix, higher-capacity drives, and cost controls. Operating margin also improved by 1300 basis points YoY and 200 basis points QoQ to 28.1% driven by operating leverage. AI initiatives have also led to gains in manufacturing productivity. Western Digital increased its dividend by 25% to $0.125 per share during Q3 results and the company’s inclusion in the Nasdaq-100 index also boosted the stock price in the last quarter of the year.

Source: YCharts

WDC Q3 revenue grew by 27.4% as it benefited from robust demand from hyperscalers for its higher-capacity hard disk drives, the most cost-effective solution for massive AI-generated datasets.

Micron (MU): The Nasdaq-100's Top Performer of 2025

Micron is the top-performing stock in the Nasdaq-100 index, posting a return of 239.1%. Technically, it ranks second, as Western Digital was added to the index on December 22; however, Western Digital traded for only one week after its inclusion.

Micron is no longer tied to consumer device cycles. Instead, high bandwidth memory (HBM) has led to higher margins and multi-year supplier agreements, resulting in a leveraged approach to participate in the AI infrastructure buildout. We discussed in depth in our article, Micron Stock Up 120% YTD: What the HBM Memory Leader Plans for 2026, that the historically cyclical memory market is seeing a newfound resurgence from AI that is strong enough to transform commoditized hardware into a secular trend as the AI economy is built out. AI servers use more DRAM and NAND than traditional servers, relying heavily on high-bandwidth memory (HBM) for training and inference.

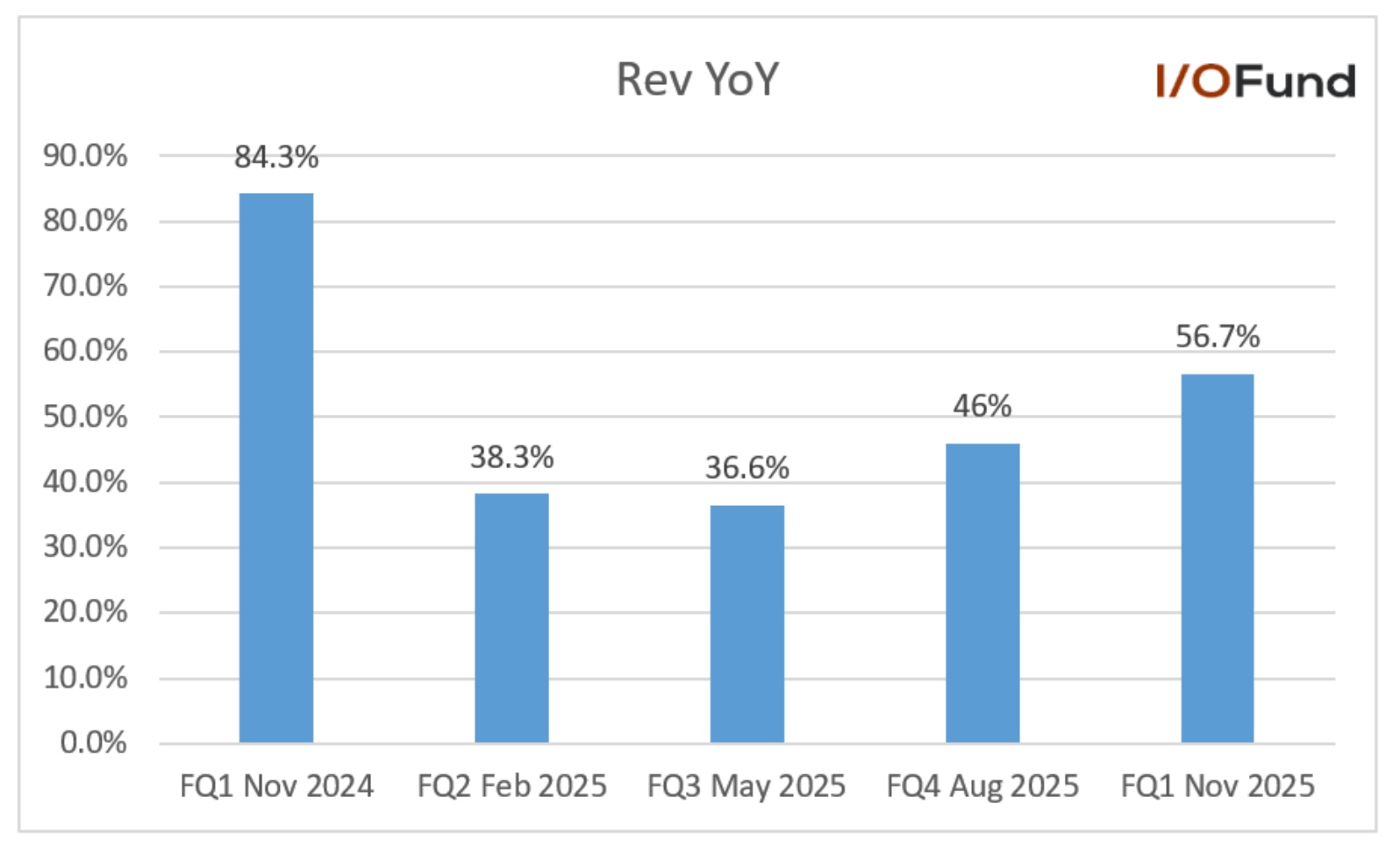

Micron topped analysts' estimates in each of the four quarters reported in 2025, benefiting from the AI-driven memory super cycle. Micron’s FQ1 revenue ending November grew by 56.7% YoY and 20.6% QoQ to a record $13.64 billion, accelerating by 10.7 percentage points from 46% growth reported in the previous quarter. The company’s gross margins improved 17.6 percentage points YoY and 11.3 percentage points QoQ to 56%, driven by an improved product mix and better pricing due to a supply-demand imbalance. Micron also reported record adjusted free cash flow of $3.9 billion, exceeding the prior record free cash flow in FQ4 2018 by over 20%. Management anticipates record revenue, margins, and free cash flows in the next quarter and FY2026, further reinforcing confidence in the durability of Micron’s AI-driven growth trajectory.

Micron’s FQ1 revenue accelerated to 56.7% YoY growth as it benefits from the AI-driven memory super cycle, driven by record High-Bandwidth Memory (HBM) demand for next-gen AI accelerators.

Source: YCharts

This past year has proven that HBM memory is a component multiplier when compared to GPUs in the hardware stack, as HBM scales faster than GPUs on a per-system basis. Each generation of GPU, from Hopper to Blackwell to Rubin, requires more memory capacity and bandwidth per chip. Therefore, there is compounded effect, as the number of GPUs rises combined with each GPU system requiring more HBM per package.

I/O Fund has a history of buying stocks at low prices. Our Nvidia’s first entry was at $3.15 in December 2018, and since then, we have been able to issue buy alerts around major lows – including $10.85 on October 13th, 2022, as well as $94.48 on April 4th, 2025, and again at $87.99 on April 7th, 2025. We discuss key technical levels in our weekly webinars for Advanced Market Signals Tier members.

Subscribe to Advanced Market Signals to get real-time trade alerts for every entry and exit, portfolio access, and join weekly live webinars. Join now.

Robinhood (HOOD): Among the S&P 500’s Top Performers of 2025

Robinhood stock continued its bull run, rising 203.5% in 2025. Along with strong results, the company’s new products, such as Prediction Markets that allow users to trade on event outcomes across politics, sports, and economics, have been very successful. Prediction markets have become the company’s fastest-growing product line by revenue ever, with 11 billion contracts traded by more than 1 million customers. Furthermore, Robinhood accelerated its global expansion by acquiring crypto exchange Bitstamp for $200 million in June and announced in May that it will buy Canadian crypto platform WonderFi for $179 million, thereby gaining critical regulatory licenses and a robust infrastructure to scale its digital asset services internationally. Robinhood stock received an additional tailwind from passive index-fund buying after its inclusion in the S&P 500 in September 2025.

Robinhood’s Q3 revenue grew by 100% YoY to a record $1.27 billion, driven by 129% YoY growth in transaction-based revenues. The company’s net deposits in the quarter were a record $20.4 billion, and Robinhood Gold subscribers reached a record 3.9 million, up 75% YoY. In Q3, two more businesses, Prediction Markets and Bitstamp, surpassed $100 million in annualized revenue, taking the total to 11 business lines. Based on October volumes, Prediction Markets is on a $300 million run rate. Robinhood has also consistently delivered GAAP profitability, with net income growing 271% YoY and 44% QoQ to $556 million in Q3. Robinhood’s 2025 stock performance reflects a company that has successfully evolved into a diversified, profitable financial platform with multiple high-growth revenue streams.

Robinhood (HOOD) Record Q3 2025 Revenue: 100% YoY Surge to $1.27 billion. This chart illustrates a massive revenue doubling, driven by a 129% jump in transaction-based revenues.

Source: Seeking Alpha

Digital Turbine (APPS): AI Ad-Tech Top Performer of 2025

Ad-tech company Digital Turbine’s stock rose 195.9% in 2025 after three years of negative returns. Digital Turbine’s revenue growth has accelerated in recent quarters, with the company returning to positive year-over-year revenue growth in Q1 2025 after a prolonged period of declines. The company’s margins have also turned around, and it reported its first positive operating margin in Q3 in about 3 years. Digital Turbine also refinanced its debt in September 2025, thereby extending its debt maturities.

The company’s Q3 revenue grew by 18.2% YoY to $140.4 million, accelerating by 7.2 percentage points from 11% growth in the previous quarter. The company benefited from strong advertising demand and international growth, and management also highlighted meaningful progress on its first-party data and AI-driven machine learning platform during the earnings call, laying the groundwork for better targeting and improved returns on investment for advertisers.

The company reported an operating profit of $6.5 million compared to a loss of (-$13.5 million) in the same period last year, its first operating profit in about three years. Digital Turbine’s adjusted EBITDA also grew by solid 78% YoY to $27.2 million, driven by strong operating leverage. Due to improved visibility, management also increased the full-year revenue and adjusted EBITDA guidance for FY2026, ending March 2026.

Source: YCharts

Digital Turbine (APPS) Revenue Breakout Signals AI Ad-Tech Turnaround: Q3 revenue grew by 18.2% YoY to $140.4 million, accelerating by 7.2 percentage points from 11% growth in the previous quarter.

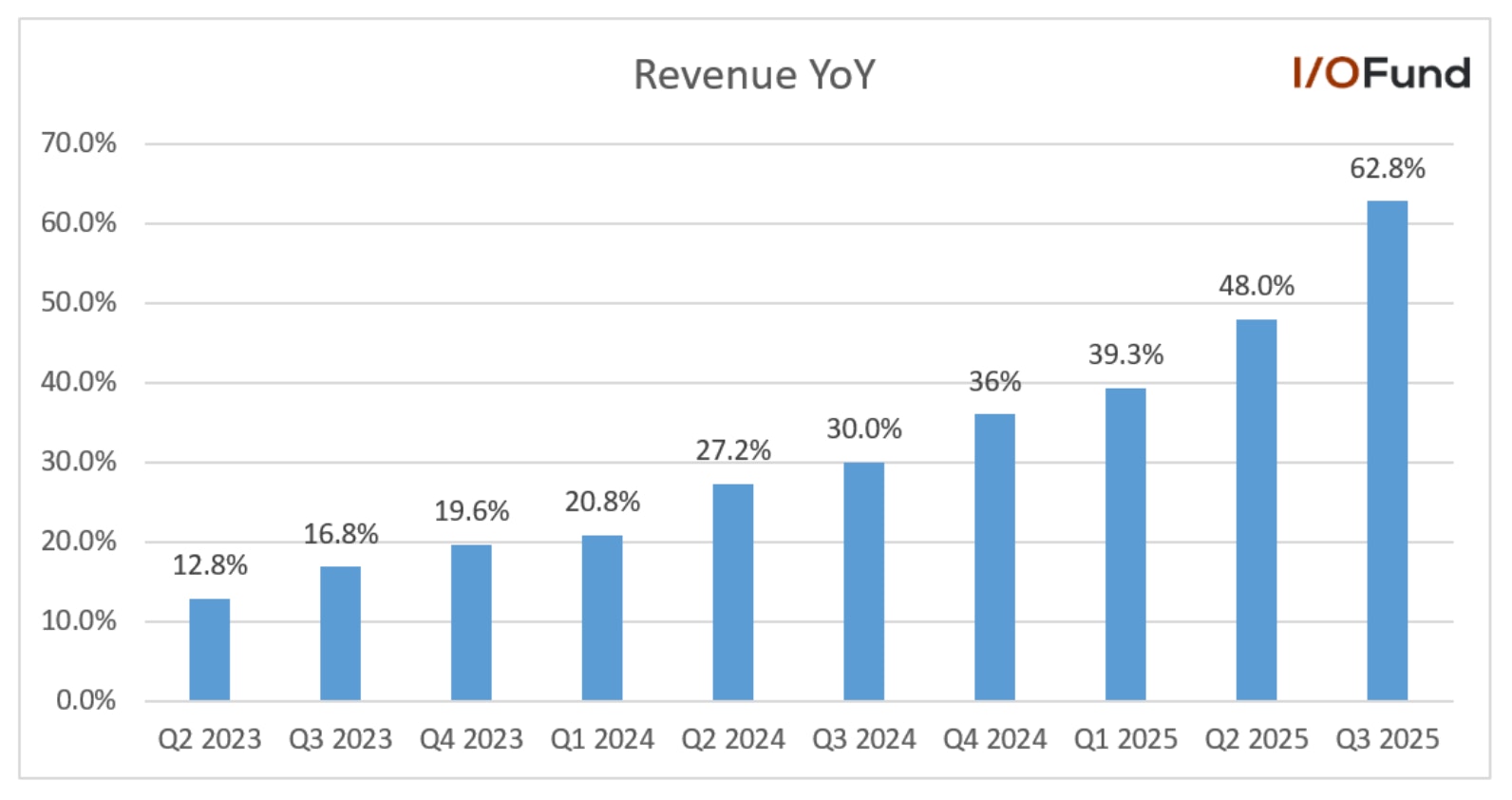

Palantir (PLTR): The S&P 500’s Standout AI Software Leader of 2025

Palantir joins the list of I/O Fund's Top Tech Stocks for a third-year running, with shares rising 135% in 2025. I/O Fund’s editorial previously pointed out that Palantir was “one of the rare few that sees AI drive both real returns for its business and real value for its customers,” as it continues to crush its software competitors in AI-related growth.

Palantir’s Artificial Intelligence Platform (AIP) has driven a significant revenue acceleration following its launch, with profitability also expanding – a rare combination for growth software stocks. AIP is a cloud-agnostic and model-agnostic platform that connects AI with existing systems and operations. AIP goes beyond what LLMs can deliver on their own by embedding models in workflows and logic. The value creation comes from being able to work with incomplete datasets through the ontology layer, while also offering a level of reasoning that goes far beyond analysing the data itself.

Palantir has capitalized on the AI software opportunity at hand via AIP’s unique value proposition, its scalability, and versatility. AIP’s scalability and flexibility continue to attract larger and more ambitious commercial engagements. In the software universe, Palantir is in rare territory, as one of the few cloud stocks seeing meaningful AI growth across multiple key metrics.

The company’s revenue growth has accelerated over the last 9 quarters. Q3 revenue grew by 62.8% YoY and 17.7% QoQ to $1.18 billion. Revenue growth accelerated 14.8 percentage points from 48% in Q2, the largest sequential acceleration to date and marking Palantir’s highest growth rate since going public. The strong growth was driven by unwavering momentum in US Commercial segment, generally seen as the primary vector for its AIP-driven growth, with revenue accelerating by 28 percentage points to 121% YoY in Q3.

Margins strengthened considerably in Q3, with an adjusted operating margin of 51%. Palantir’s Rule of 40 score (revenue growth + adj operating margin) expanded to a wild 114%, up from 94% last quarter and 68% in Q3 2024.

Palantir (PLTR) Revenue YoY Growth: 9-Quarter Acceleration Hits Record 62.8% in Q3 2025, marking the highest growth rate since its IPO. This chart highlights the unprecedented revenue acceleration driven by Palantir’s Artificial Intelligence Platform (AIP).

Source: YCharts

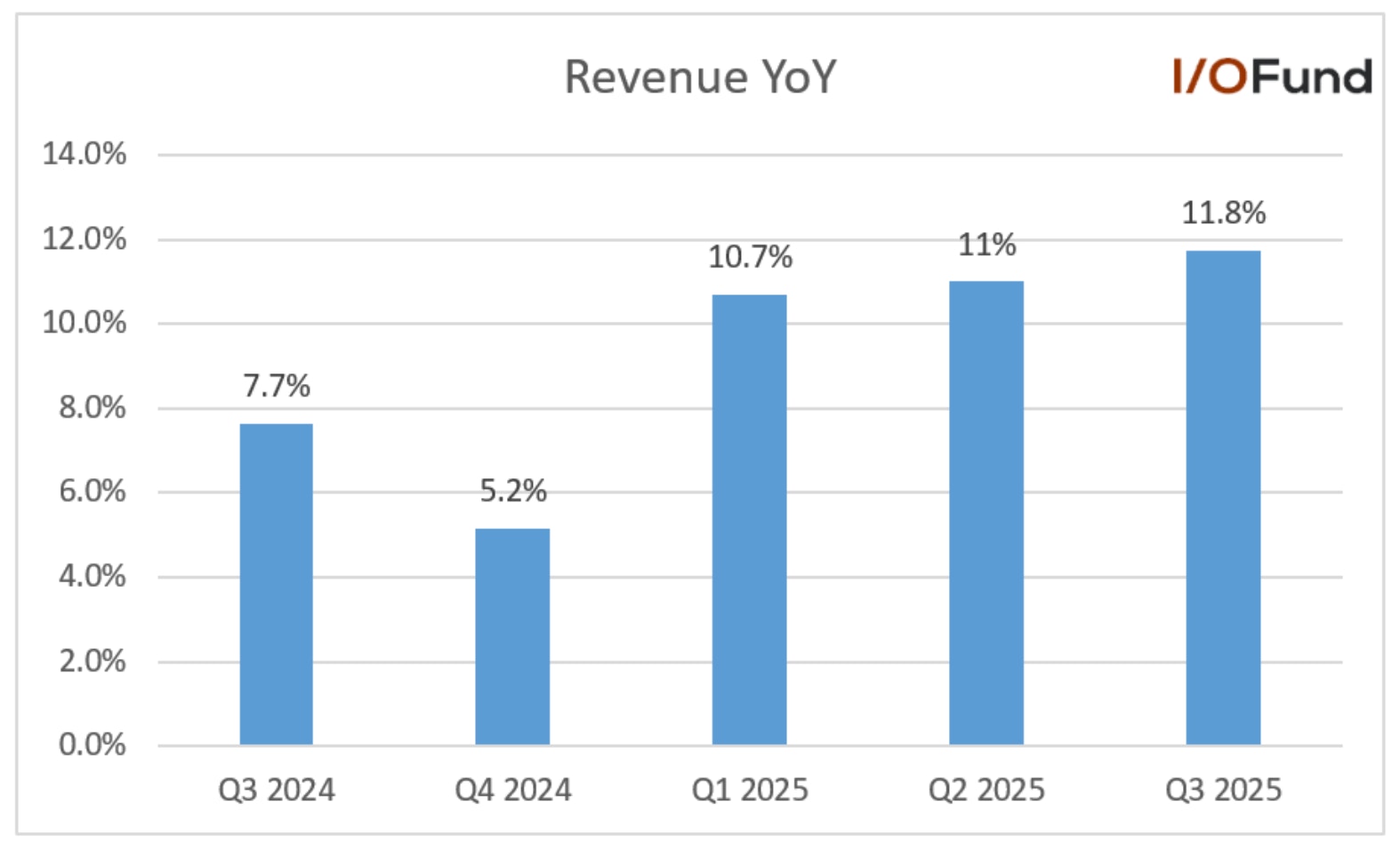

GE Vernova (GEV): Powering the AI Grid with 98.7% Return

GE Vernova is part of the spinoff that General Electric first announced in 2021 and later completed in 2024. The company is the world’s largest gas turbine supplier, at 25% ahead of Schneider at 24%. GE Vernova is a major beneficiary of the increasing energy requirements from the global AI infrastructure build-out, positioning the company as a key beneficiary of this secular trend. The stock rose 98.7% in 2025. 25% of global electricity was generated using the company’s equipment. Due to a sudden surge in AI-related electricity demand, turbine orders are vastly outpacing demand, and the company’s order book is sold out through 2028.

The stock also got a boost after the company’s 2025 investor update. The company raised the by 2028 revenue outlook to $52 billion from the prior $45 billion. Similarly, the adjusted EBITDA margin was raised to 20% from the prior 14%, and cumulative 2025 to 2028 free cash flow was raised to over $22 billion from the prior over $14 billion. GE Vernova expects to grow total backlog from $135 billion to $200 billion by year-end 2028, including doubling the size of electrification backlog from $30 billion to $60 billion. The Board of Directors also increased the share repurchase authorization from $6 billion to $10 billion and doubled the annual dividend to $2 per share.

The company’s Q3 revenue grew by 11.8% YoY to $10 billion. Operating margin improved on a YoY basis and came at 3.7% compared to (-4%) in the same period last year. The company also announced that it will acquire the remaining 50% stake in Prolec GE, its joint venture with Xignux for $5.275 billion and the transaction is expected to close in mid-2026.

GE Vernova (GEV) Q3 revenue grew by 11.8% YoY to $10 billion beating analysts' expectations and growth was driven by the AI Energy Supercycle.

Source: YCharts

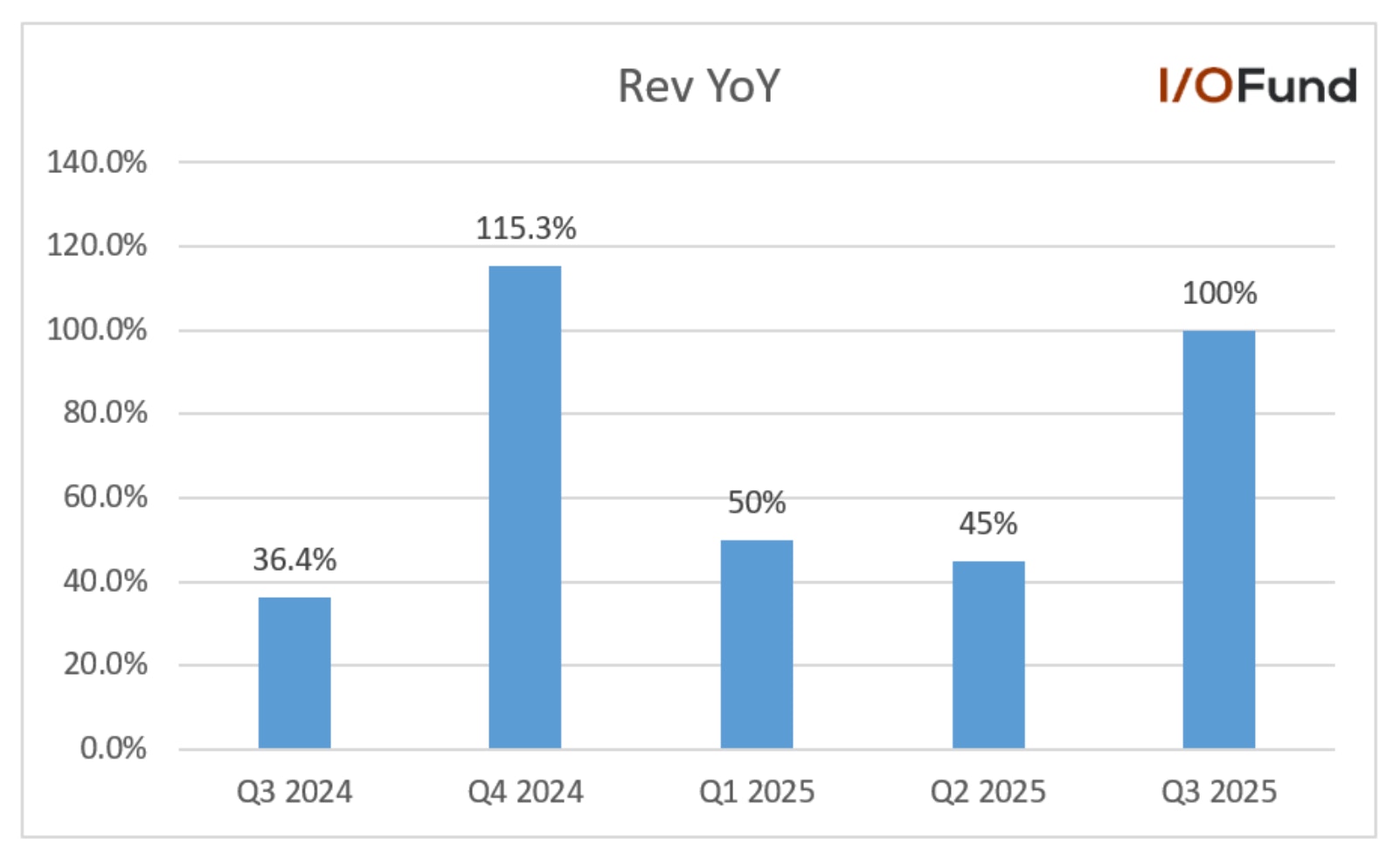

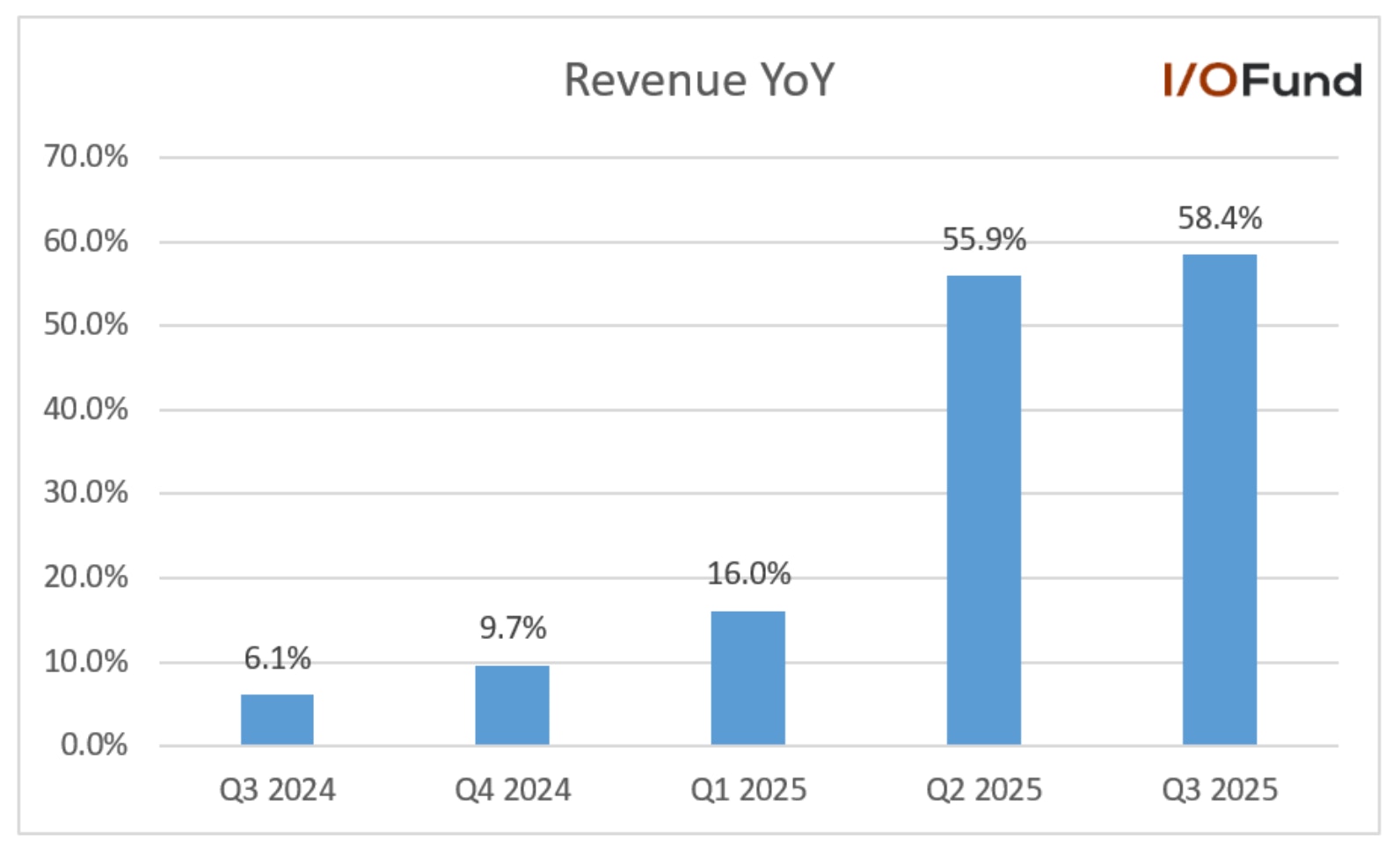

#9: Dominating the AI Optical Interconnect and EML Market

This little-known optical technology supplier became a must-own AI beneficiary in 2025—surging 339.1% as Nvidia’s Blackwell rollout and explosive data-center demand rewrote its growth and profitability story. The company supplies components for datacom transceivers and optical interconnects. It has a differentiated technology that has caught the attention of AI heavyweights such as Nvidia, and the company’s Electro-absorption modulated lasers (EMLs) are a critical component with Nvidia’s Blackwell generation. Similarly, optical interconnects help data centers accelerate data throughput between data centers and inside the data center between servers or racks, while reducing latency and power consumption. AI is driving cloud demand higher among hyperscalers, leading to more data being created and processed, thereby fueling a need for interconnects to support high-speed, low-power data transmission in data centers. To find out which company it is, sign up early here.

Similar to SanDisk, the company reported strong revenue growth acceleration in 2025 from 16% YoY growth in Q1 to 55.9% in Q2 and 58.4% in Q3. Revenue growth is expected to further accelerate to 60.6% and 62.1% in the next two quarters. The company also surpassed its guidance of over $500 million revenue a quarter earlier than its expectations, reporting a record $533.8 million in Q3. The company’s Q4 guidance of $650 million is significant as it will reach its $600 million quarterly revenue target two quarters ahead of schedule, primarily reflecting accelerating AI-driven demand.

Source: YCharts

The company reported its first positive operating margin in the last three years. The company reported an operating margin of 1.3% in Q3 compared to (-24.5%) in the same period last year. The company is witnessing a turnaround in margins driven by strong operating leverage, higher pricing due to the supply-demand imbalance, improved manufacturing efficiencies, and a favorable product mix. Margins are expected to improve further in 2026, with premium pricing from supply-demand imbalances serving as a strong lever for margin expansion.

AI-driven demand translated into rapidly accelerating revenue growth, early achievement of revenue targets, and a meaningful turnaround in profitability, significantly strengthening investor confidence in 2025.

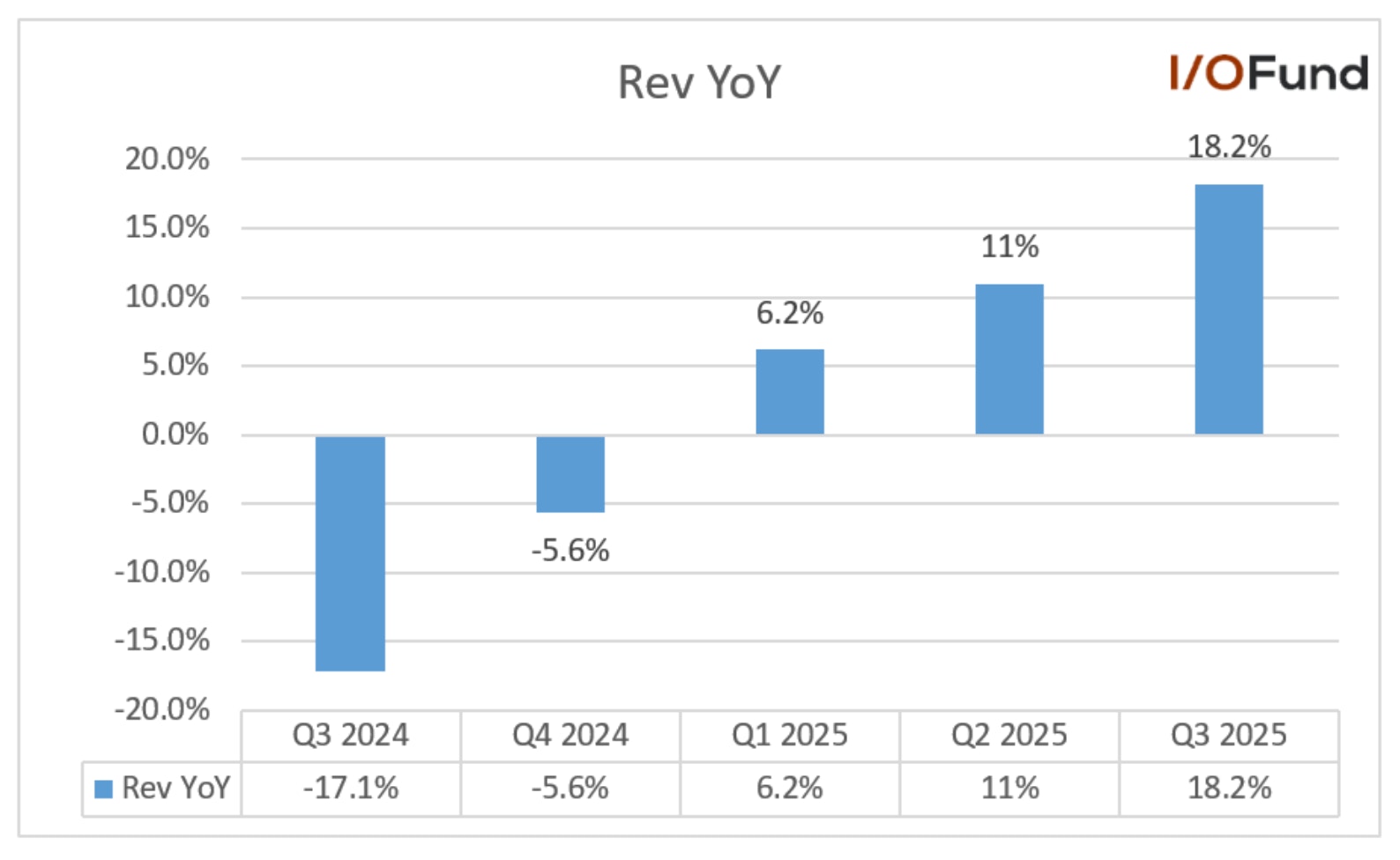

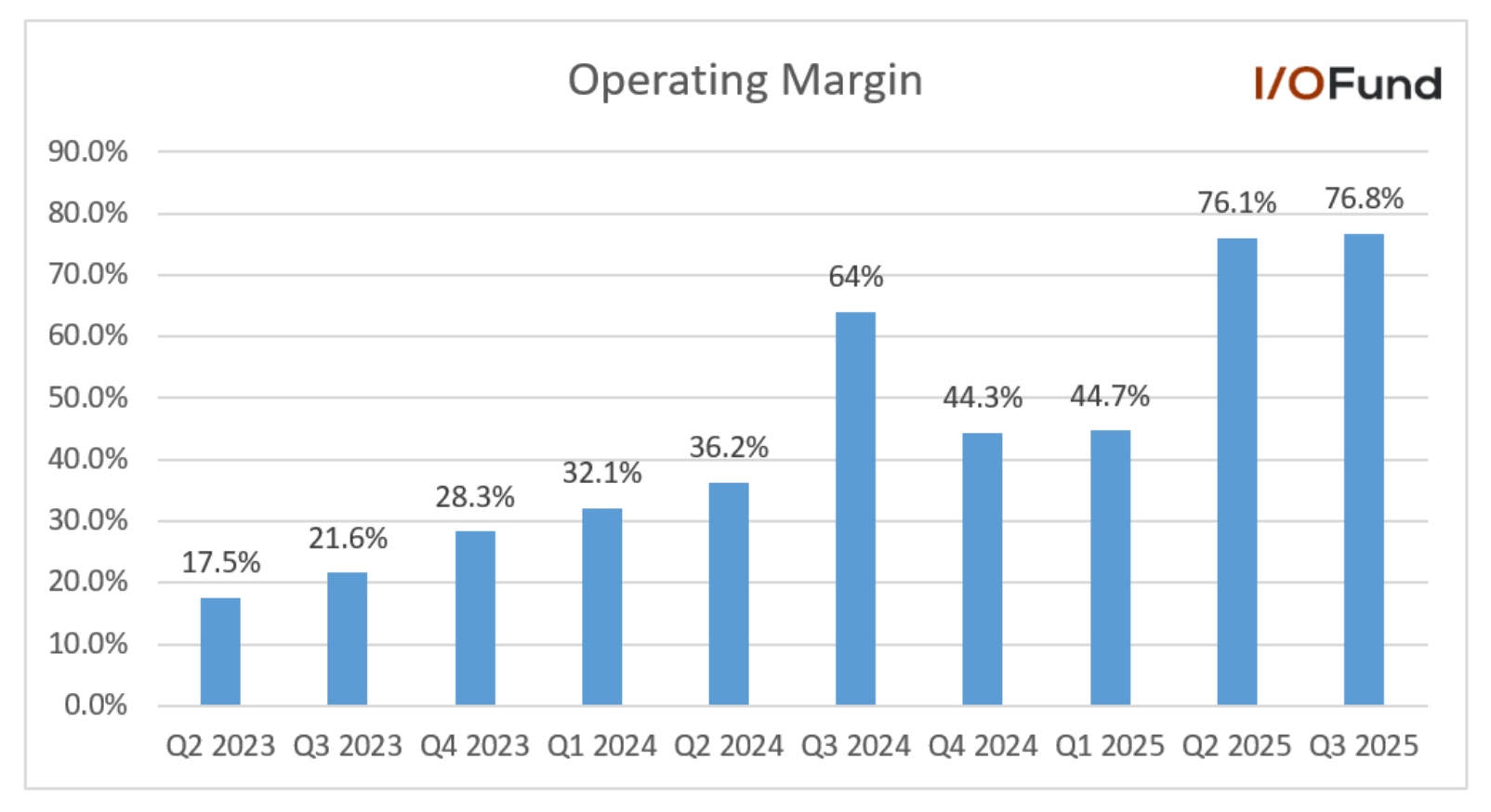

#10: The S&P 500’s Top-Performing AI Ad-Tech Stock

This stock soared 108.1% in 2025 as its AI-powered advertising engine accomplished the unthinkable—reviving a stagnant mobile gaming ads market and delivering extraordinary profitability. The company also divested its gaming assets segment in Q2 2025 and is now a pure-play ad-tech stock. The high-growth, high-margin advertising business that drove the strong returns over the past few years is now the company’s sole focus. To find out which company it is, sign up early here.

The stock was added to the S&P 500 index in September. The stock also received a further boost as it launched the self-service platform in October, which will help the company tap into e-commerce ad budgets. Management is confident in maintaining 20% to 30% YoY growth for the foreseeable future, and incremental growth from the self-service platform could help exceed this baseline.

The company’s Q3 revenue grew by 68.2% YoY and 11.6% QoQ to $1.41 billion. The growth was primarily driven by the strong gaming advertising revenue. The company’s revenue growth is only part of the story, whereas the bottom line is what sets this stock apart. Its margin expansion is truly outstanding, primarily driven by strong operating leverage. The company’s AI-powered advertising engine, launched in Q2 2023, served as a game-changer, driving strong revenue and profits. The company’s operating margin has increased from 17.5% in Q2 2023 to a remarkable 76.8% in Q3 2025. Adjusted EBITDA grew by 79% YoY to $1.16 billion with an outstanding adjusted EBITDA margin of 82%. The company has an exceptionally strong cash flow margin profile, primarily driven by strong profits, and free cash flows grew by 92.4% YoY to $1.05 billion in Q3.

Source: Company IR

Conclusion

Reflecting on 2025 is vital; it provides the blueprint for 2026. While 'winners keep winning,' our goal isn't to chase a carbon copy of last year, but to identify the structural patterns that drove that success. The 2025 leaders proved they could thrive despite macroeconomic headwinds, driven by revenue acceleration and operating leverage that turned high demand into massive margin expansion.

Most importantly, 2025 shifted the AI narrative. The focus rotated toward the 'physical' layers of the stack, revealing that memory, storage, and energy are now the industry's critical bottlenecks. As we enter 2026, we are watching for the next set of companies that can turn scarcity into a competitive moat.

Subscribe to Advanced Market Signals to get real-time trade alerts for every entry and exit, portfolio access, and join weekly live webinars. Join now.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. I/O Fund own shares in NVDA, MU, BE, and GEV at the time of writing.

Recommended Reading:

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i