Apple Bets On The Emerging Markets Growth Story

June 05, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jun 1, 2023,08:15am EDT

The smartphone market continues to be hit hard in q1, with prices down 20% and shipments down 13%, according to Canalys. Despite double digit decline across the industry, Apple delivered marginal growth on its iPhone sales at +1.5%. According to Counterpoint Research, Apple grew smartphone shipments by 1 million year-over-year from 59 million in Q1 2022 to 58 million in Q1 2023. The decline of (1.7%) was better than the (14%) decline for the global smartphone market.

Source: BETH KINDIG

According to Apple’s management, the reason the company was able to overcome smartphone weakness was due to sales in the emerging markets. The company’s CFO, Luca Maestri, said in the earnings call, “We set March quarter records in several developed and emerging markets with India, Indonesia, Turkey and the UAE doubling on a year-over-year basis.”

Within the emerging markets, India is a primary focus for Apple due to a growing middle class. According to a survey from a non-profit, the middle-class population has grown from 14% in 2004-05 to 31% in 2020-21. Tim Cook also points to the fact that the country is at a tipping point. “There are a lot of people coming into the middle class, and I really feel that India is at a tipping point, and it's great to be there.”

Although Apple does not break down India sales figures, Bloomberg News reported that sales grew by 46% YoY to about $6 billion for the trailing twelve months ending March 2023. According to a Wedbush analyst, “Apple is now aggressively looking at India from both a production and retail expansion over the coming years that the firm believes will be a strategic poker move for Cupertino that could ramp annual revenue to $20 billion by 2025 in India.”

Tim Cook recently visited India in April and opened two company-owned retail stores. Apple was the second biggest revenue generating brand in India in 2022, second only to Samsung as it gained 18% of the total value of smartphone shipments, according to research firm Counterpoint.

The company also plans to make India a manufacturing hub and this move is seen as the company’s efforts to rely less on China. JP Morgan mentioned in its research note last year that the company plans to produce 25% of all iPhones from India by 2025. However, it could take a few more years to reach the 25% level. According to Bloomberg News, the company now produces 7% of total iPhones from India and this is up from 1% in 2021.

Apple supplier Foxconn announced recently that the company plans to invest $500 million to set up a manufacturing plant in India. It had also announced in March that it received approval from another state in India for a $968 million investment. Similarly, Foxconn has plans to expand its existing manufacturing plants in India.

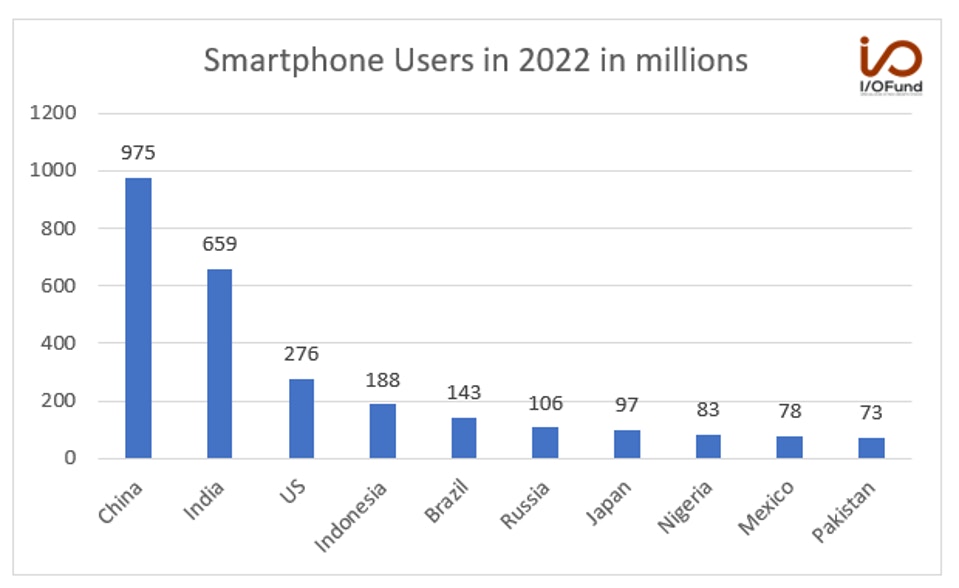

There are 2 billion Apple devices active in the world and there are 659 million smartphone users in India, compared to 975 million in China and 276 million in the United States. With India being second place, it makes sense that Tim Cook is focused here.

Source: Statista

According to Morgan Stanley analyst Erik Woodring, “The firm's 2023 revenue and EPS forecast increased by 1% and 3%, respectively, post-earnings and while the firm calls out iPhone 15 and an AR/VR headset as the next catalysts, it adds "don't sleep" on the emerging markets and India story at Apple.”

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Apple’s Brand Needs a Catalyst

Warren Buffet was recently asked why he is invested in Apple and his reply was “If you’re an Apple user and somebody offers you $10,000, but the only proviso is they’ll take away your iPhone and you’ll never be able to buy another, you’re not going to take it. If they tell you if you buy another Ford car, they’ll give you $10,000 not to do that, you’ll take the $10,000 and you’ll buy a Chevy instead.”

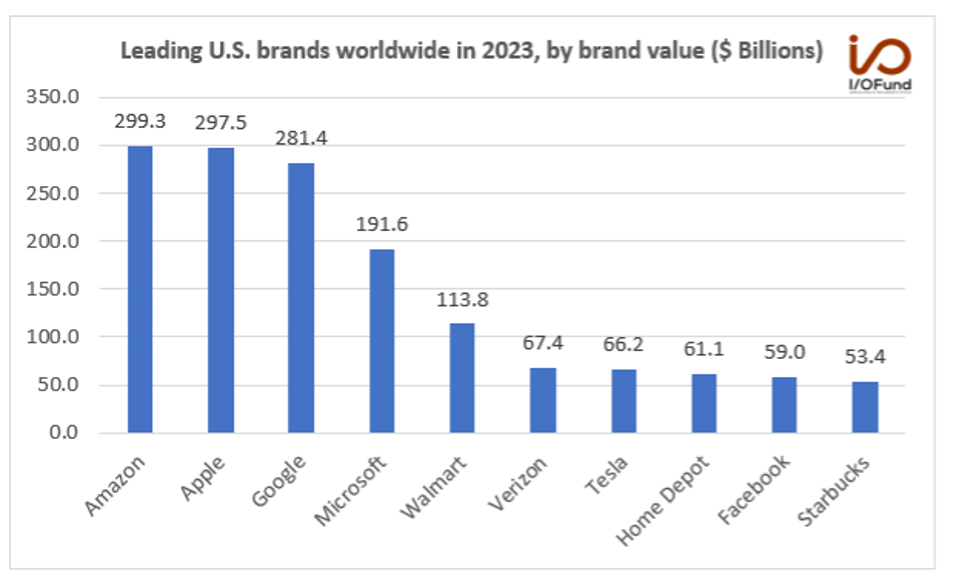

Not surprisingly, Apple is one of the world’s most valuable brands, rivaled only by Amazon and Google.

Source: I/O FUND

Despite this strong brand, the next chapter for Apple has been slow to materialize. As seen below, wearables have not become the “next big thing” for Apple with $8 billion or so in revenue per quarter. Emerging markets are promising, yet at the $20 billion per year or $5 billion per quarter, Apple will struggle to move the needle for some time by relying on this strategy alone.

Earlier this month, we published an article “Apple’s Stock in Focus: More Profitable Than Banks” where we stated:

“Investors looking for the “next big thing” will point toward companies like Stripe, Sofi or Square as the leading fintech stocks. Meanwhile, the next big thing to disrupt the financial sector may be sitting in plain sight. Apple grew its cash trove through legendary design and hardware, yet how Apple chooses to leverage its enormous reserve of cash may be what writes the next chapter for the world’s most valuable company.”

Services remain a long-term opportunity for the company to monetize its installed base of over 2 billion active devices. Apple recently launched a new high-yield savings account that offers a 4.15% interest rate, which is 10 times higher than the United States national average and 415 times higher than what Chase or Bank of America offers at 0.01%. Apple is also lending from its balance sheet for the first time ever through Apple Pay’s Buy Now and Pay Later product.

To illustrate how effective Apple’s move into finance tech has become, the cornerstone product, Apple Pay, currently has 75 percent adoption among iPhone users. This is up from 10% in 2016. In addition to taking on banks, Apple is also competing with Mastercard and Visa with features that allow merchants to use iPhones and iPads to send and receive payments. The long-term goal is to replace wallets with iPhones.

Spotlight on Earnings

For some time now, Apple has been a value stock. We discussed this when we stated:

“While comparing to other popular value stocks like Walmart, Apple is trading at a slightly higher forward P/E ratio of 23 compared to Walmart’s 19. However, the company’s net profit margin of 25.71% is very good compared to Walmart’s 1.45%.

Similarly, Apple has an excellent free cash flow margin of 26.37% compared to Walmart's negative free cash flow margin of -5.15%. This helps illustrate why Apple’s stock has held up well as investors are able to participate in the most cash efficient company of all time while also participating in the company’s future innovation cycle.”

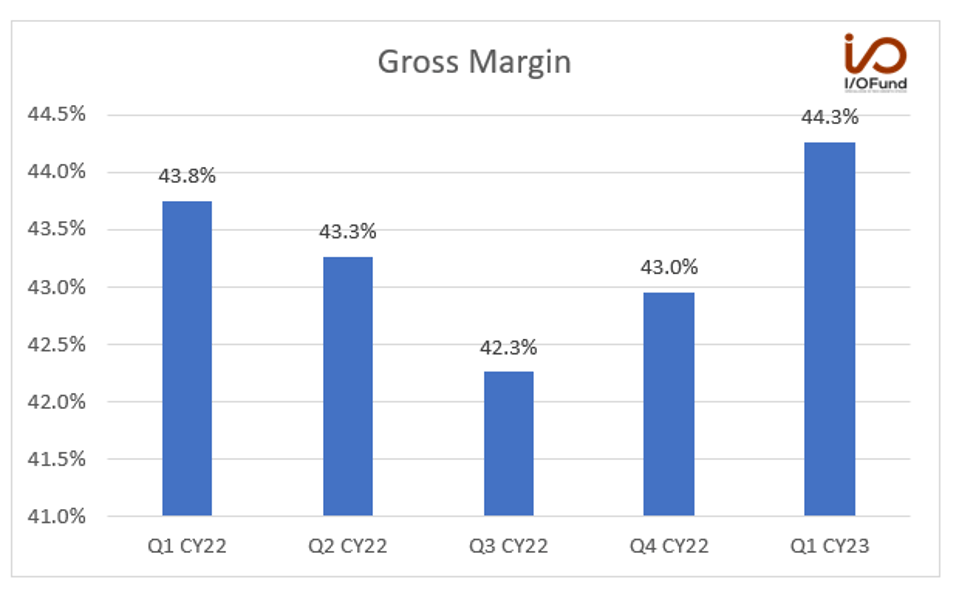

The most recent earnings results continue to prove that Apple’s management team is strong on efficiency. Despite revenue declining by (2.5%) YoY to $94.84B, the gross margin improved from 43.8% to 44.3% in the most recent quarter, up 50 basis points due to cost savings and a favorable mix from Services. The free cash flow margin remained solid at 27% compared to 26.4% in the same period last year. The board also authorized an additional $90 billion share repurchase and increased the quarterly dividend by 4% to $0.24 per share.

Source: COMPANY IR

Operating income declined by (5.5%) and net income declined by (3.4%) YoY to $24.2 billion. EPS of $1.52 remained unchanged from the same period last year, and notably, the company beat EPS estimates by 6.4%.

As stated, iPhone sales were up +1.5% to $51.3 billion. Mac revenue declined by (31%) YoY to $7.2 billion. This was due to a strong comp with M1 MacBooks sales from last year and a weaker consumer. iPad declined (13%) YoY to $6.7 billion. Wearables declined (0.6%) to $8.8 billion.

Services grew 5.5% YoY to $20.9 billion.

Paid subscriptions of 975 million, was up 18.2% YoY. This segment is important as there is a higher gross margin of 71% compared to 36.7% for products.

Management’s directional insights for the June quarter were soft with foreign exchange negatively impacting growth by about 4%. The company’s CFO, Luca Maestri, said in the earnings call, “We expect our June quarter year-over-year revenue performance to be similar to the March quarter, assuming that the macroeconomic outlook does not worsen from what we are projecting today for the current quarter. Foreign exchange will continue to be a headwind and we expect a negative year-over-year impact of nearly four percentage points.”

Analysts expect revenue to decline by (1.1%) YoY to $82.03 billion.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Where Can Apple Stock Go from Here?

There are two scenarios we are tracking for Apple based on the current price information:

The blue count suggests that we are in a long and drawn-out correction that will ultimately be targeting new lows. If Apple stays below $181.50 and then breaks below $150.50, the odds that this scenario is playing out will become very high. If this plays out, we will look towards the blue target box for a major low.

The red count suggests that the January low for Apple was a major one. This will put us in the final push in the large uptrend that began in 2009. If Apple can break above $181.50, we can see a final push to the upper red target box between $192 - $210.

Source: I/O Fund

Apple is currently under the major resistance zone between $176.25 - $181.50. Based on the relative weakness in most markets right now – small caps, industrials, materials, financials, transportation, the Dow Jones, as well as many global markets - we are expecting volatility to return sometime in early June. If Apple fails to punch through the $181.50 resistance before the market pulls back, it will need to hold the $160 - $150.50 range in order to allow for this final swing into the red target zone above. Below $150.50 and the top will be in for Apple, as the odds will greatly increase that we will be testing Apple’s January lows.

Conclusion:

My firm does not own Apple at the moment, yet given its enormous brand value and high install base, it’s a company we track closely. In addition, the company’s strong financials will only become more attractive in the event of a recession. For our purposes, my firm would want to see Services materialize as a leading Fintech play, and we would want to wait for the price action outlined above to play out before buying this stock.

The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund does not own shares in AAPL at the time of writing but may own other stocks pictured in the charts.

Royston Roche, I/O Fund Analyst, contributed to this article.

Recommended Reading:

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su