Renewable Energy Stocks That Benefit From $400 Billion IRA Bill

June 28, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jun 22, 2023,09:31 pm EDT

China’s 2001 entry into the WTO marked the beginning of the golden age of globalization. This was the catalyst that led to the global outsourcing of domestic manufacturing capacity to lower cost regions around the world. As a result, world economies became more interlinked.

In 2016, President Trump began his administration by imposing tariffs on China, one of the United States’ largest trading partners. This signaled globalization’s peak and the beginning of a shift downward. This shift has continued with the Biden administration and the passing of the Bipartisan Infrastructure Law (BIL) ($550B) and the CHIPS and Science Act ($53B). The legislative goal is to improve US economic competition, innovation, and industrial productivity.

On August 16, 2022, Biden signed the Inflation Reduction Act (IRA). It directs new federal spending toward reducing carbon emissions. The IRA’s primary objective is to spur investments in US domestic manufacturing capacity. This most recent legislative action is another step toward the “Made in America” goal and increasing manufacturing-related national security. Its signing was a boon for the alternative energy sector’s 2022 performance.

2023 has been marked by higher volatility as the final legislative details, implementation and earnings impact of the IRA have slowly crystalized. Meanwhile, threats made against parts of the bill during last-minute legislative horse trading in the debt ceiling negotiations also created uncertainty. With that signed, we have a clearer roadmap as to how to best position for the IRA from an investment perspective.

We believe those companies that have these three characteristics stand to benefit the most. 1) Meaningfully collect the IRA corporate tax credit 2) Established US based manufacturing operations and 3) Viewed as important players in the IRA.

Based on these criteria, we believe First Solar stands to benefit. Furthermore, we believe that First Solar has positioned itself as one of the national champions in its implementation. In First Solar’s Q422 earnings call, they provided initial guidance as to the positive financial impact the credit would have in 2023. At the time the stock was trading $170 and rallied 30% to $220. The stock has given back a portion of these gains and currently trades at $187.

At current levels, we see a compelling risk/reward. Our medium price target indicates 30% upside versus 7% downside. Longer term, we see over 50% upside to our price target. We have a preference for companies who are selling to utilities such as First Solar rather than those selling to consumers via installers, such as Enphase. Enphase will not immediately benefit and the impact will be smaller, plus management pointed out near-term macro concerns due to higher interest rates affecting their business. Tesla may potentially benefit from its battery operations which could provide a buffer to its automotive margins if it continues to lower prices to gain share.

What is the IRA?

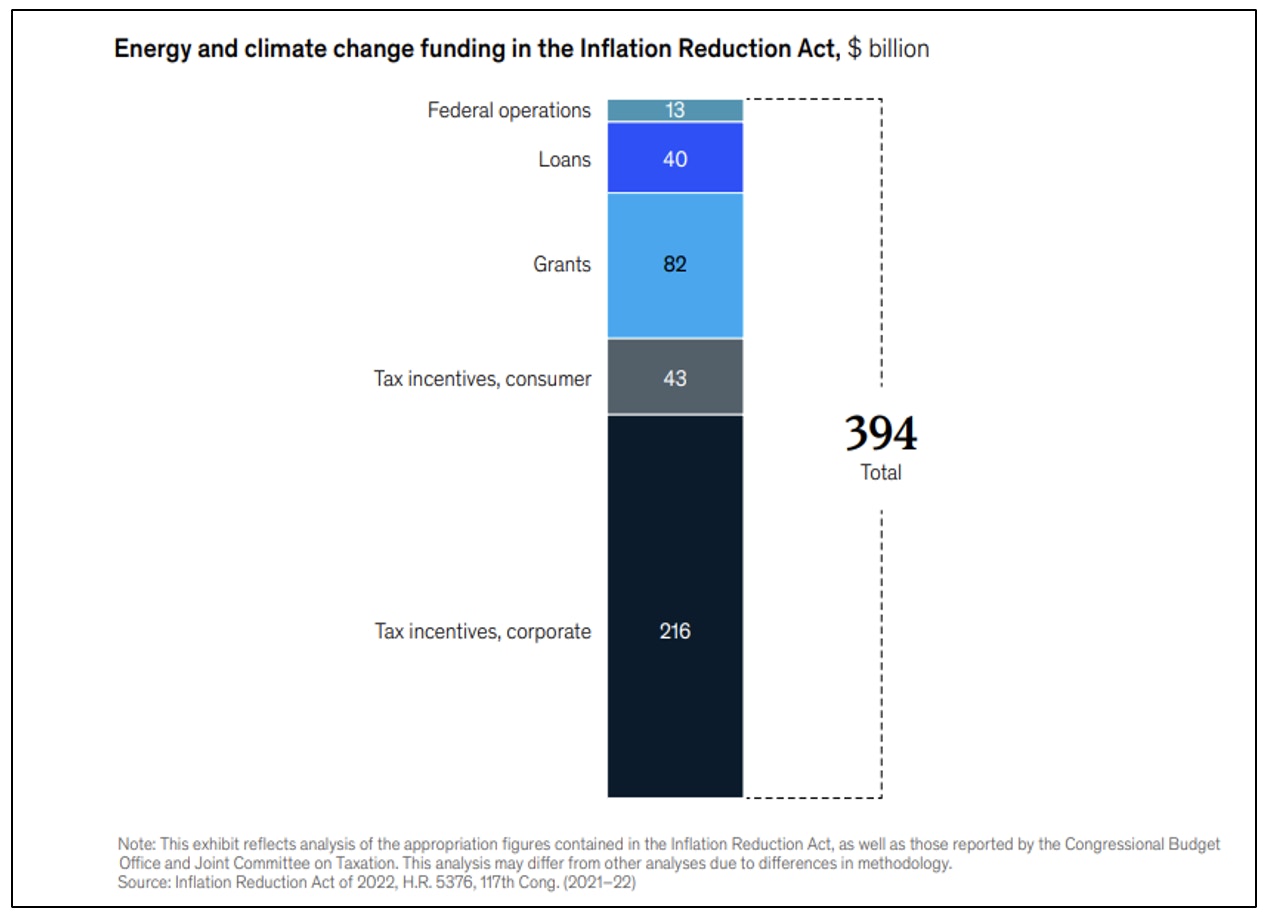

Based on an analysis by McKinsey and Company , the IRA directs nearly $400B in federal funding to clean energy, with the goal of substantially lowering the US’s carbon emission by the end of this decade. The funds will be dispersed via a mix of tax incentives, grants and loan guarantees. Clean electricity and transmission will receive the highest funding, followed by clean transportation, including electric-vehicle (EV) incentives.

In the past, the US has generally relied on imports for solar equipment. This law will encourage more production at home with incentives for domestic solar panels and inverter manufacturing. It is also designed to support the construction of renewable electricity plants.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Who benefits from it the most?

In the McKinsey report, there are estimates that the majority of the $394B in energy and climate funding will be in the form of tax credits. Corporations with US manufacturing capacity are the biggest beneficiaries with an estimated $216 billion worth of tax incentives available. They are meant to provide an incentive for private domestic investment in clean energy, transport and manufacturing. Many of the tax incentives are direct pay, meaning they can claim their credit in that tax year and be paid the following year.

Source: MCKINSEY

How does the IRA impact earnings?

The IRA should provide an earnings tailwind for the clean energy sector. Companies are now just beginning to discuss the potential earnings impact in their commentary. Some have provided more details than others.

From an investment perspective, the key is to identify companies with US based manufacturing capacity that are eligible to directly collect a portion of the Corporate Tax Incentive ($216b) rather than those companies that will indirectly benefit from consumers claiming the Consumer Tax Incentive ($43b).

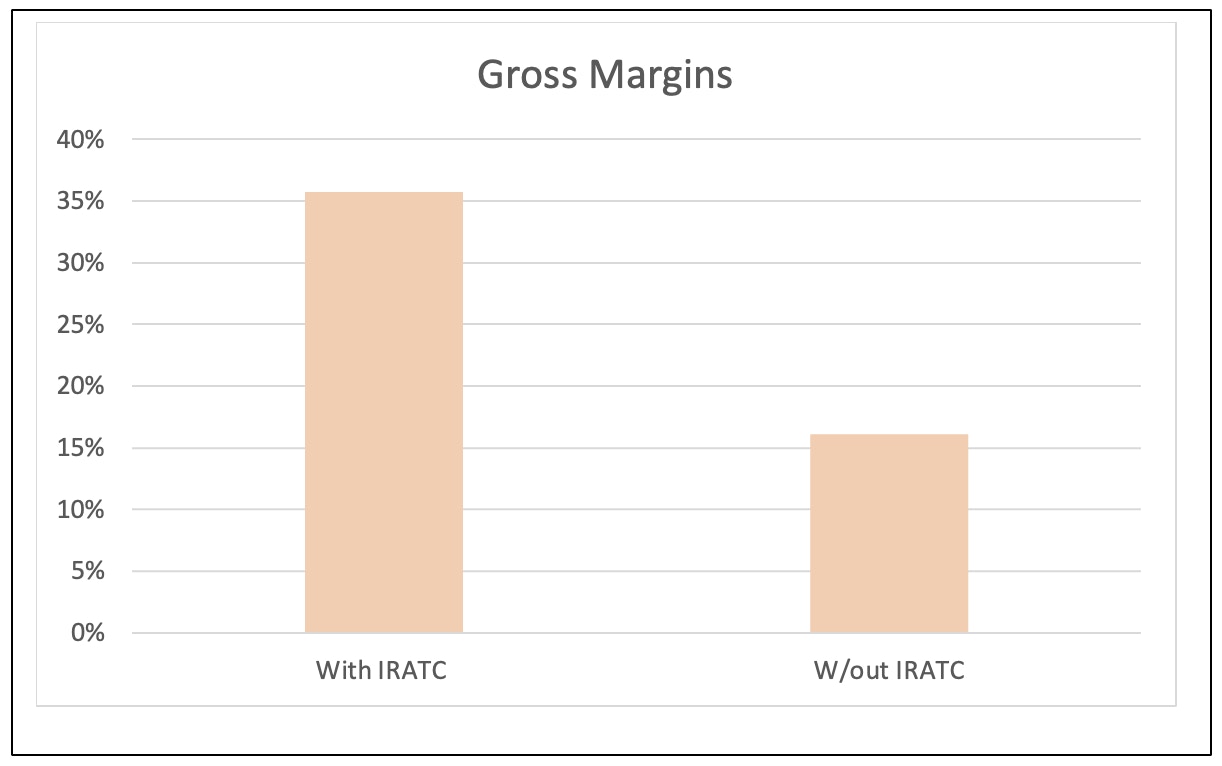

Critically, it’s important to identify those companies whose earnings will be significantly impacted by the Corporate Tax Incentive. For example, this is the potential impact the IRATC will have on First Solar’s gross margins. Its gross margins more than double. The intent of the IRA bill is clear. Provide companies with a profitable financial incentive to install domestic manufacturing capacity.

Source: I/O FUND

One of the reasons that First Solar stands out is due, in no part, to the fact that they have provided the most visibility as to how the IRA will impact their earnings. In doing so, they have provided a useful investment framework to assess how other companies may benefit. Not every company will have this type of impact on their profitability.

Companies are eligible to claim these claims starting in 2023 through 2030. It is still very early stages on assessing the full impact this may have on the years to come. Those that are positioned to meaningfully collect them will outperform those that aren’t.

How does the IRA Tax Credit (IRATC) work?

This is how First Solar described how the IRATC will work with the benefit first recorded in Q1 of 2023:

“Following consultation review with outside advisers, our auditors and the SEC, we expect to recognize these credits as a reduction to cost of sales in the period such modules and the integrated eligible components are sold to customers.”

In their 2023 guidance, they went on to say

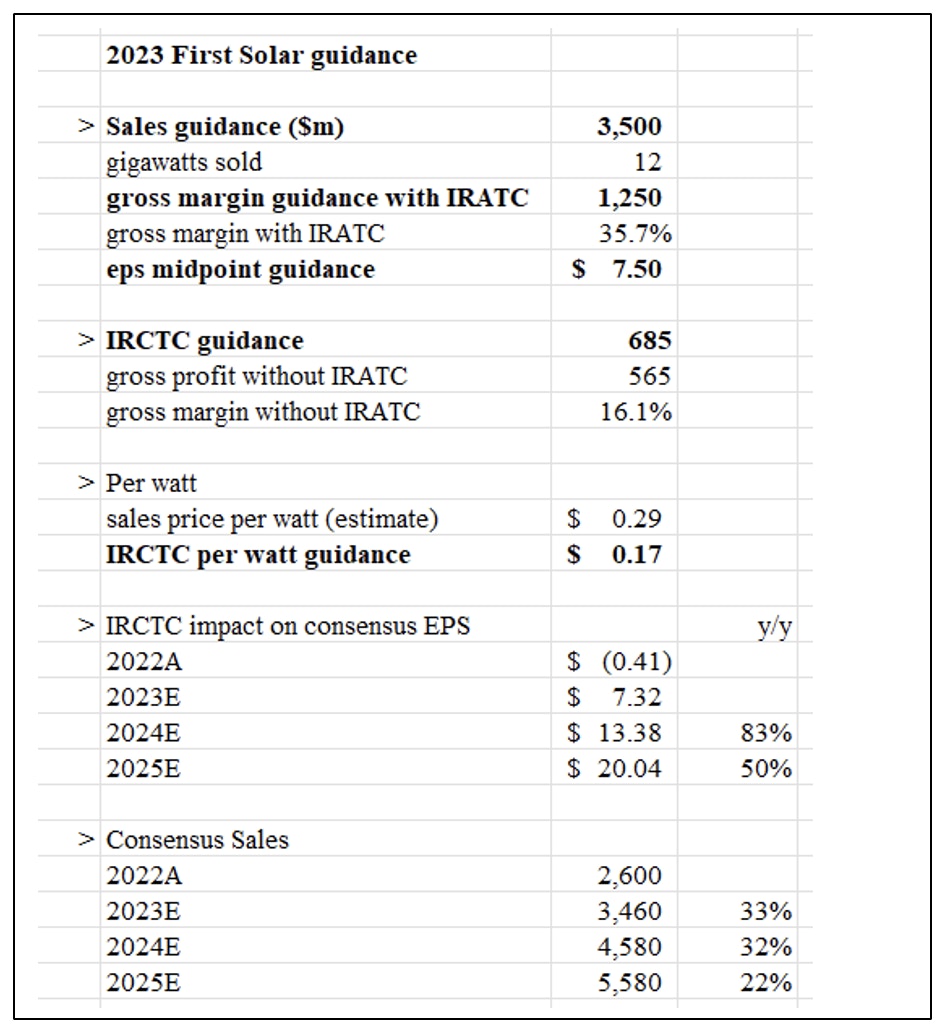

“I’ll now cover the full year 2023 guidance ranges. Our net sales guidance is between $3.4 billion and $3.6 billion; gross margin is expected to be between $1.2 billion and $1.3 billion, which includes $660 million to $710 million of advanced manufacturing production tax credits under Section 45X of the IRA; and $110 million to $130 million of ramp and underutilization costs. This results in a full year 2023 earnings per diluted share guidance range of $7 to $8.”

The best way to appreciate the impact of the IRATC is to analyze the impact on profitability with and without the IRATC.

FSLR’s guidance provides insight on the impact of the IRATC. To simplify the analysis, we’ve taken the mid-point and excluded the ramp-up related costs.

Source: I/O FUND

As we pointed out earlier, First Solar’s gross margins will more than double. Another way to look at it is that in addition to the First Solar’s current estimated 2023 average sales price of $0.29 per watt. First Solar will receive an additional $0.17 per watt in the form of the IRATC. An effective 59% increase in its sales price.

This is how FSLR broke down the 2023 IRATC in the Q422 call.

“Given our fully integrated thin film manufacturing process, we expect that this guidance will entitle us to integrated tax credits for wafers, cells and module assembly, which we estimate will equal approximately $0.17 per watt for modules produced in the United States and sold to a third-party.”

Because First Solar has been advised to treat the IRATC as a reduction in costs of sales, it’s important to focus on their growth in earnings per share. Assuming other companies adopt the same reporting standard, the same investment parameters will apply.

The impact on earnings is significant. Consensus earnings are expected to increase 80% from 2023 to 2024 and 50% from 2024 to 2025. Comparing it to 2022 is not an apples-to-apples comparison as there was no IRATC benefit in 2022 while gross margins were impacted by higher than expected logistic related costs. There were mainly penalty costs related to exceeding dock waiting times due to Covid supply-chain issues. FSLR has indicated that these and other costs will trend back down toward pre-pandemic levels over the course of the year.

Not every company will capture a similar level of profitability uplift. Generally speaking, those with higher domestic content can claim more of the IRATC. Companies will seek to capture as much of the IRATC as possible. And from an investment perspective, companies that have existing domestic capacity and can claim the IRATC in 2023 will be the stocks that benefit the most in the short-term.

In Q422, FSLR provided insights on domestic capacity expansion as it relates to collecting the IRATC.

“… we believe that the intent of IRA is to create enduring long-term supply chains, which would therefore motivate and align the incentives to true manufacturing in the U.S., more than just final module assembly with all the build material being sourced from international locations.

And if everything lines up along those lines, then that sort of helps inform our view there as it relates to the inherent value of more domestic manufacturing, plus we want to make sure that, while we believe we're fully entitled to the vertically integrated manufacturing tax credit, to the extent that we can get confirmation through guidance from IRS and Treasury, that would be very beneficial as we think about factory expansion.”

The key word is “vertically integrated”. The more that a company’s US based manufacturing is vertically integrated, the more of the IRATC it can claim.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Making of a National Champion

FSLR manufactures solar modules based on thin film Cadmium Telluride (CadTel) photovoltaic (PV) technology demonstrated to have lower cost, superior scalability, and a higher theoretical efficiency limit over conventional technologies, like crystalline silicon (c-Si). Solar module sales represented 93% of total sales and the majority of sales were to developers and operators of systems in the United States. A few of its largest customers include Intersect Power, Lightsource BP, and NextEra Energy.

FSLR will benefit as its clients have an incentive to build out their own capacity to capture the IRATC. We have preference toward those companies that will benefit from the corporate IRATC rather than the consumer IRATC. The former includes utilities while the latter includes installers that are reliant on consumers to make the financial outlay to install solar panels etc.

It goes without saying that the IRA is an important piece of legislature. First Solar is positioning themselves as one of the National Champions to help in the IRA’s implementation. As we’ve seen internationally, National Champions typically get to provide input into and beneficial treatment from the government and other regulatory bodies. We believe the amount of IRATC visibility that FSLR has provided, in contrast to others thus far, is a reflection of that.

A further case in point, in the Q123 call First Solar cited remaining legislative hurdles. There was a tug-of-war to finalize the details of the IRA bill between the Treasury and Congress. It came down to Assembled vs Made in the USA. The former relates to companies that apply for waivers to procure certain components overseas, assemble the final product domestically and then attempt to qualify for the IRATC.

“As it relates to capacity expansion, look, the — as we said, the primary engaging factor right now is clarity on policy. And I said it in my prepared remarks, if we — if the domestic content stays true to the Congressional intent of IRA and it truly requires a highly manufacturable component here in the U.S. in order to qualify and the bonus being truly a bonus and not trying to create some form of entitlement, which we believe that should include at least the cell, if not beyond the cell as part of the domestic content requirements to be manufactured here in the U.S. That's going to be a key determining factor in terms of new capacity”

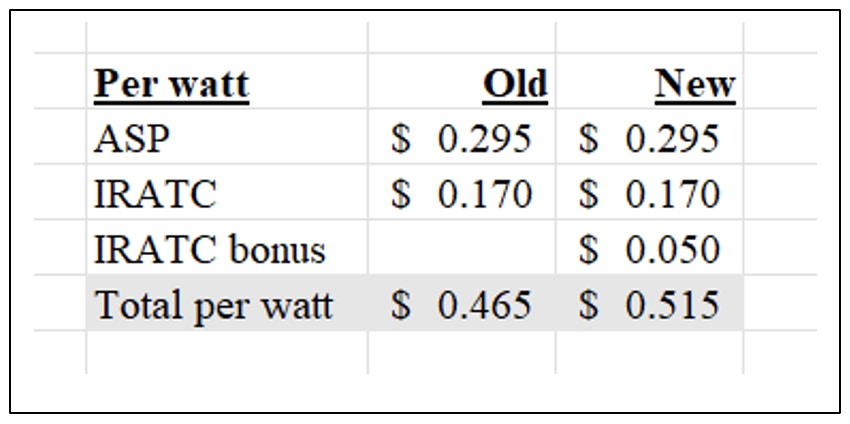

After that comment, an IRATC Bonus was announced that heavily favors and appeases “National Champions” like First Solar who are in the best position to collect the IRATC bonus that is tied to the use of US steel in their manufacturing. We estimate that the IRATC Bonus is worth another $0.03 to $0.05 per watt.

So breaking it all down, this is the estimated impact the IRATC and IRATC Bonus will have on First Solar’s estimated effective “total selling price” before domestic price escalators. A 75% increase from its $0.295 estimated ASP.

Source: I/O FUND

Resetting 2023 Expectations

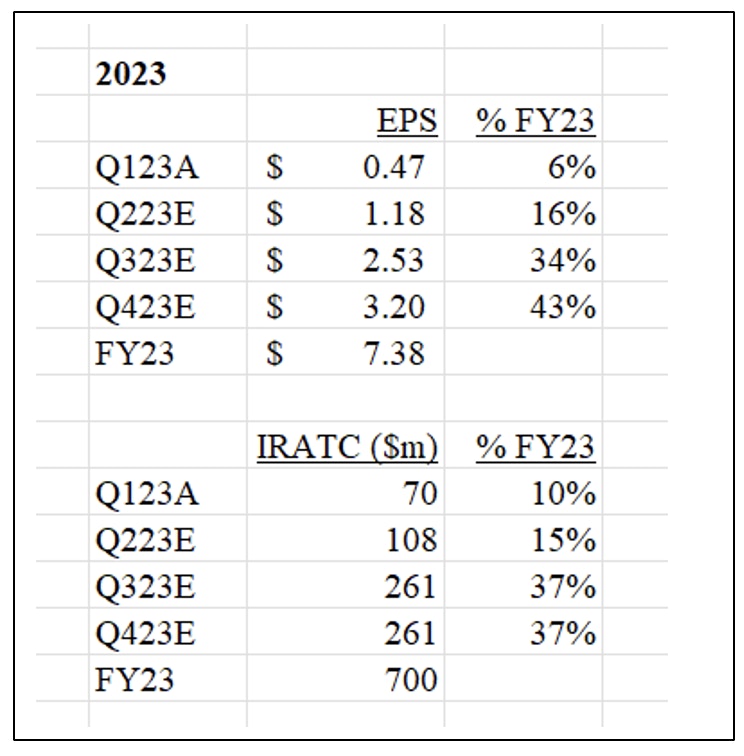

In Q422, FSLR guided for about $700m in 2023 IRATC. The stock rallied higher but has been very volatile and now has given up most of its gains. We believe this has been somewhat self-inflicted. If First Solar management can be criticized for one thing is that they could have done a better job of managing expectations. For example, as part of its $700 guidance, it stated

“Section 45X credits, recognized, will increase after Q1, driven by both the timing of volumes sold as well as the inventory lag, whereby products sold in the early part of 2023 may have been manufactured in 2022.”

Despite this, market expectations were likely elevated going into Q1 and the market did not appreciate these timing differences. Additionally, logistic costs that were elevated during the pandemic have not quite returned to normalized levels and were still a drag on gross margins. While FSLR did not provide any Q1 guidance, it did miss consensus by a significant margin. Q123 sales were $583 million, up 49% y/y and down 45% sequentially. Q123 sales missed consensus expectations of $713m and eps was $0.47 vs consensus expectations of $0.86

Despite this Q123 miss, FSLR management did not change their full year 2023 guidance and stated: “we anticipate our earnings profile will be higher in the second half of the year.”

Putting this all together, we can see the timing on consensus eps and FSLR IRATC recognition. It’s still very much 2h23 weighted. In light of the timing differences and the fact that legislation had not yet been finalized at the time of their 2023 IRATC guidance given in Q4. If FLSR could do it all over again, we suspect they likely would have provided more conservative FY2023 IRATC guidance and wait to revise it up as the final legislative details were cemented.

Source: I/O FUND

Q2 Earnings and Forward

Although from an earnings and IRATC contribution perspective, Q223 will not make a large contribution. It is important in terms of FSLR reestablishing credibility to their 2023 earnings guidance and confidence in the potential earnings power in 2024 and 2025.

Unlike Q123, expectations are muted going into Q2. The IRATC Bonus may provide FSLR another lever to at least meet Q223 consensus. Importantly, the IRATC bonus may provide an opportunity for FSLR to revise up their $700 IRATC guidance. The stock would react positively in this situation. However, the one factor worth noting is that the CEO has recently sold about $8m worth of stock.

At current levels around $185, we see a compelling risk/reward. Our medium price target indicates 30% upside versus 7% downside. Longer term, we see over 50% upside to our price target once we gain more confidence the 2025 eps is attainable; where on consensus estimates, valuation is not demanding.

Will Tesla benefit from the IRATC?

Tesla stands to benefit indirectly from the Consumer IRA tax credit as it may spur demand for its EVs. The IRA provides consumers a maximum $7,500 tax credit to incentivize the purchase of EV over combustion engine cars. Not every automaker’s EV will quality for the tax credit. In the case of Tesla, their Model 3 and Model Y qualify for the full credit.

Consumers have to meet certain criteria to claim the full $7,500. For example, married couples filing jointly can’t make more than $300,000 and $150,000 for singles. Importantly, you have to have paid at least $7,500 in federal taxes in order to claim the full $7,500 credit in your tax return. In states like California, Tesla cars qualify for the Cleaner Vehicle Rebate which ranges from $2,000 to $7,000, this is an actual cash rebate rather than a tax reduction.

For those consumers who were already interested in buying a Tesla, these two programs provide further incentives.

On the corporate tax credit side, we have been waiting to see if Tesla will provide guidance as to whether their battery manufacturing qualifies for section 45x of the Inflation Reduction Act Tax Credits (IRATC). Given the accounting treatment of the IRATC, the credit lifts both gross and operating margins.

Benchmark Mineral Intelligence estimates that Tesla will receive $1.8b in IRATC in 2023. To provide some context, Tesla reported $2.7b in gaap operating profit in q123. This works out to $1,000 IRATC per car based on Tesla’s 1.8 million unit production guidance,

If Benchmark’s estimate is accurate, this is very important for Tesla’s stock price. Currently, the market is concerned that Tesla will sacrifice automotive margins in the short term by lowering its prices to gain market share. The IRATC potentially will provide a cushion so that Tesla’s margins are impacted less by lowering prices. Or put another way, it may provide Tesla ammunition to further lower prices. Perhaps an unintended consequence of the IRA whereby the US government is providing a company financial support to attack the major US auto manufacturers.

However, Tesla has not yet provided any official guidance. They may do so in Q223.

Will Installers benefit from the IRATC?

Our analysis points towards less of a benefit for module/inverter companies, such as Enphase, who typically manufacture overseas and then sell through installers who then sell to US consumers.

Enphase outsources the actual manufacturing of its solar inverters to overseas electronic contract manufacturers (ECM). Enphase is in the process of using a US based ECM in order to qualify for parts of the IRATC. However, ENPH will have to give-up a portion of the IRATC to the ECM. This US operation should be fully up and running in 2024 and will contribute about 50% of Enphase’s total manufacturing capacity. So Enphase won’t benefit from the IRATC until sometime next year. Based on Enphase’s initial guidance, we estimate this could add additional 2-5% to Enphase’s gross margins which currently stand at about 43%.

Conclusion:

The IRATC is in place until 2030. The last remaining details of the bill were just finalized. Taking a baseball analogy, the game is not even in the first inning. This will unfold over the next several years. The Inflation Reduction Act is an important piece of legislation and is supportive of the alternative energy sector. We prefer companies that have more direct earnings exposure to the IRATC and to corporate (i.e., utility) rather than consumer capex.

For a potential entry, we’d like to see if price can break above $230. If it can, then it could reset the current downward bias. We would consider that a clear breakout buy. On the other hand, if we do fail to break above this level, we will be looking to $145 for our first target buy. We share buy plans such as this one every week in our premium webinars held on Thursdays at 4:30 pm EST. We also issue real-time trade alerts when we do buy and are one of the only audited portfolios available to retail investors. Our performance exceeds institutional all-tech portfolios. Learn more here.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Readings:

More To Explore

Newsletter

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb

The AI Networking Stock That Beat Nvidia by 7X YTD for Returns of 135% YTD

AI networking stock Lumentum is among the key I/O Fund winners in 2026. We allocated heavily to LITE in January—a month before Nvidia backed the company. While most investors couldn’t stomach taking a