Arm Stock: AI Chip Favorite Is Overpriced

March 26, 2024

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Mar 21, 2024,01:49 pm EDT

Arm Holdings is positioned to capitalize on the growing adoption of artificial intelligence (AI) technologies, leveraging its established licensing model and extensive ecosystem to drive future growth. Arm's established licensing model offers a recurring and relatively stable income source, and the stock is seeing favorable price action due to the growing tailwinds from its higher-royalty v9 design supporting next-generation AI chips from Nvidia, Microsoft, Amazon and others.

Yet, despite Arm dominating the smartphone market with 99% share, the company has made very little on licensing compared to its partners. For example, mobile handsets created a $200+ billion segment for Apple, which relies on Arm technology for the iPhone, yet only resulted in (roughly) $3 billion for Arm. In this case, it was far better to own Apple.

The market is excited about the fact that AI will drive double the licensing fees for Arm. My contention is that, similar to mobile, it’s better to own the AI leaders who license Arm’s technology rather than Arm. Analyst estimates have Arm growing to $6.5 billion by 2028. For our purposes, this isn’t high enough growth to ensure insiders, aka SoftBank, won’t take their exit following the IPO lock-up expiration. Frankly, the valuation on Arm is absurdly expensive, at more than double the most-expensive chip stocks, including Nvidia. This is why we’ve stated in the past that Arm makes a better acquisition target. For public investors’ purposes, there is no riskier proposition than an IPO that is richly valued.

Background on Arm

Arm offers the most popular CPU architecture in the world with 250 billion chips shipped since inception, of which 30.6 billion were shipped in FY2023. It’s most dominant in mobile CPUs with 99% market share, and 40.8% in automotive, for an overall share of 48% in Arm’s related markets. This dominant market share is achieved through its developer ecosystem.

For mobile (and how it came to reach 99% share), Arm’s design known as “heterogenous compute” has helped facilitate lower power requirements as the architecture allows different CPU parts to work together for improved efficiency. This enables workloads to work across both high-performance and low-performance CPU cores to lower energy by balancing performance.

Arm’s different licensing models are the following:

Arm Total Access Agreements: It is a type of licensing model wherein the company provides a package of CPU designs and related technologies for an annual fee. The agreement has a fixed term and Arm reserves the right to modify the package by adding or removing specific products.

Arm Flexible Access Agreements: This model provides a selection of CPU designs and related technologies for an annual fee. However, the latest products are not included. In comparison, the total access agreement is a comprehensive package. Another key difference is that the customers need to pay a single-use license fee for specific products if they are included in the final chip design. Like total access agreements, the company reserves the right to modify the package.

Technology Licensing Agreements: It involves licensing a specific CPU design or technology to the customer for a fixed fee. The license can be used for a fixed term or the number of uses.

Architecture License Agreements: Under this agreement the customers design their own customized CPU designs using the Arm’s Instruction Set Architecture (ISA).

Arm’s v9 Architecture

The latest Arm v9 architecture offers significant improvements in performance and efficiency, particularly for artificial intelligence (AI) applications. This has led to increased adoption by its partners, particularly in the premium smartphone segment and with hyperscalers developing their own custom silicon for data center use.

CEO Rene Haas explained that the “premium smartphone is almost exclusively now v9, and virtually every high-end data centre chip is v9. When you look at Grace Hopper, when you look at Graviton, when you look at Microsoft Cobalt, these are all v9-based designs.” However, CFO Jason Child emphasized that Arm is “overweighted towards smartphones on v9, primarily because it’s an annual refresh cycle.”

Compared to the previous v8 architecture, v9 chips command double the royalty rate. This means Arm receives a higher percentage of the chip's selling price when a manufacturer uses v9 designs.

The rapid growth in v9 adoption and its higher royalty rates have already contributed to a significant increase in Arm's royalty revenue. v9 constituted 10% of royalty revenue in the September quarter and accelerated to 15% in the recent quarter. By doing the math, v9 revenue grew 69% QoQ to $70.5 million. As adoption continues to rise, the v9 architecture is expected to be a major driver of future royalty income growth for Arm.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Addressable Market

The company’s total addressable market was $203 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 6.8% to $247 billion in CY2025. The company has maintained a market share of over 99% in the mobile applications processor market. It expects this market to grow at a CAGR of 6.4%, from $29.9 billion in 2022 to about $36 billion in 2025. The company estimates that the aggregate value of chips that contain Arm technology was $98.9 billion (48.9% market share) for the CY ending December 2022, up from 38.7% in 2014. Notably, the 6.8% CAGR is a low CAGR for an AI trend with AI chips expected to grow at a 38.2% CAGR.

Arm also has strong market share of 40.8% in the automotive chip market. Management expects the automotive chip market to grow from $18.8 billion in 2022 to $29.1 billion in 2025, growing at a CAGR of 15.7%.

The cloud compute chip market is expected to grow at a CAGR of 16.6% from $17.9 billion in CY2022 to $28.4 billion in CY2025. Arm’s market share in the cloud computing chip market has increased from 7.2% in CY2020 to 10.1% in CY2022. Since Arm-based chips are increasingly used in data centers, its market share is expected to increase significantly in the future.

Per the prospectus, “Arm-based chips have been gaining market share as CSPs, such as Amazon AWS and Alibaba, have started to deploy Arm products in their own in-house designed chips used in their data centers, and as other CSPs, such as Microsoft and Oracle, start to deploy chips designed by Arm licensees, such as Ampere. As a result, we expect our market share of cloud compute to grow significantly faster than the overall cloud compute market.”

Financials

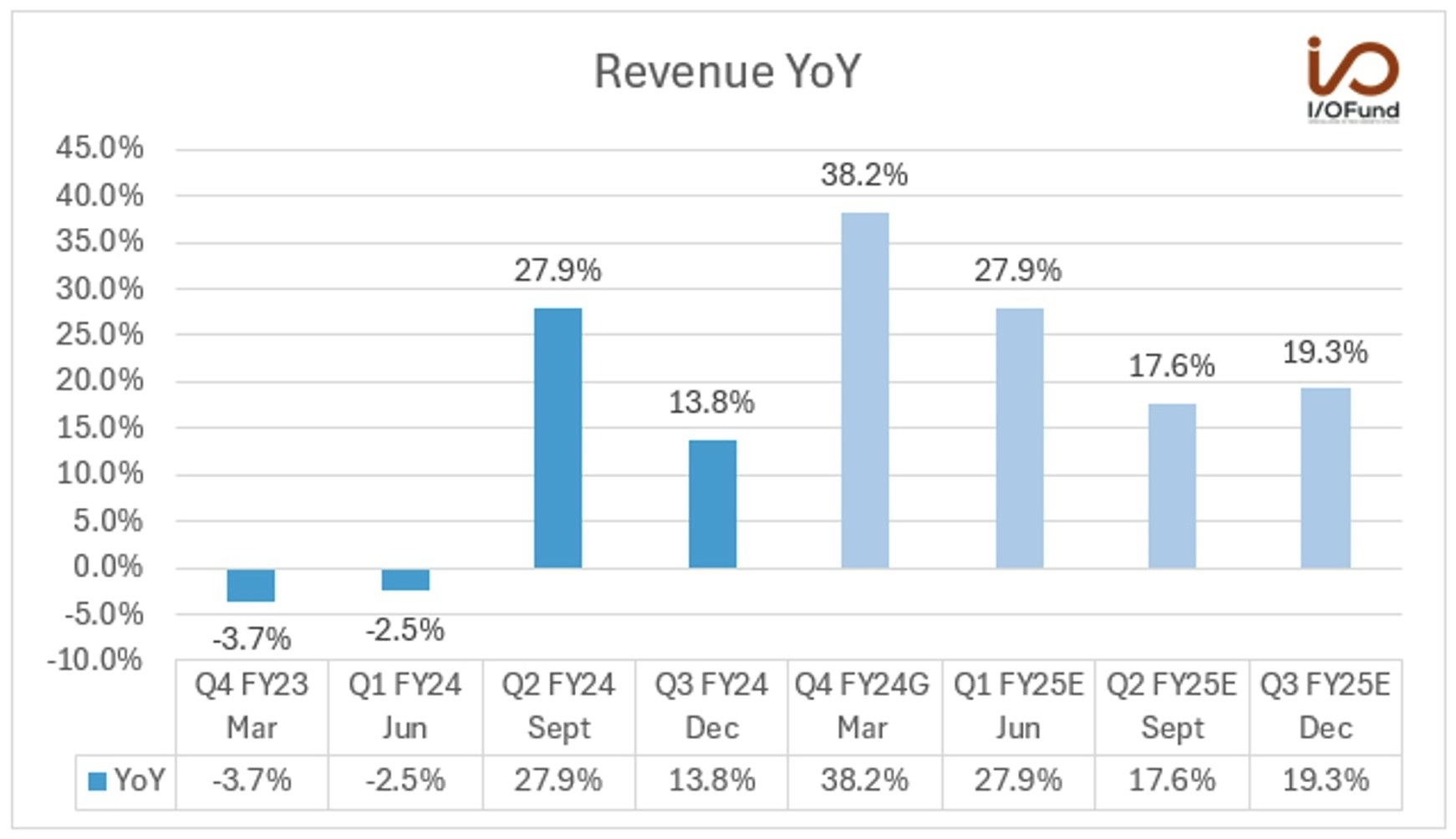

Arm’s recent Q3 FY2024 revenue ending December grew by 13.8% YoY to $824 million, helped by the recovery in the smartphone market and demand for AI technology. This marks the second consecutive quarter of positive revenue growth, following declines of (2.5%) in the June quarter and (3.7%) in the March quarter, due to the cyclical downturn from smartphones.

License and other revenue grew 18% YoY to $354 million. The company has seen strong growth in license revenue as they are signing long-term and high value agreements with its customers due to demand for Arm’s advanced CPUs to run AI workloads. The trend was strongest in the Sept quarter as license revenue grew by 106%.

CEO Rene Haas said in the earnings call, “And that has seen growth in not only the smartphone sector but also in infrastructure and other markets, which drives growth. We are also seeing strong momentum and tailwinds from all things AI. From the most complex devices on the planet for training and inference, the NVIDIA Grace Hopper 200 to edge devices such as the Gemini Nano Pixel 6 from Google or the Samsung Galaxy S24, more and more AI is running on more end devices, and that's all running on Arm.”

They expect another record quarter for the licensing revenue. CFO Jason Child said Arm is “expecting another strong quarter for licensing with revenue up sequentially to near record levels. As with recent quarters, we expect to sign multiple new ATA deals in Q4, and demand for our latest technology remains high as customers need access to AI-capable CPUs and related technology such as our Compute Subsystems.”

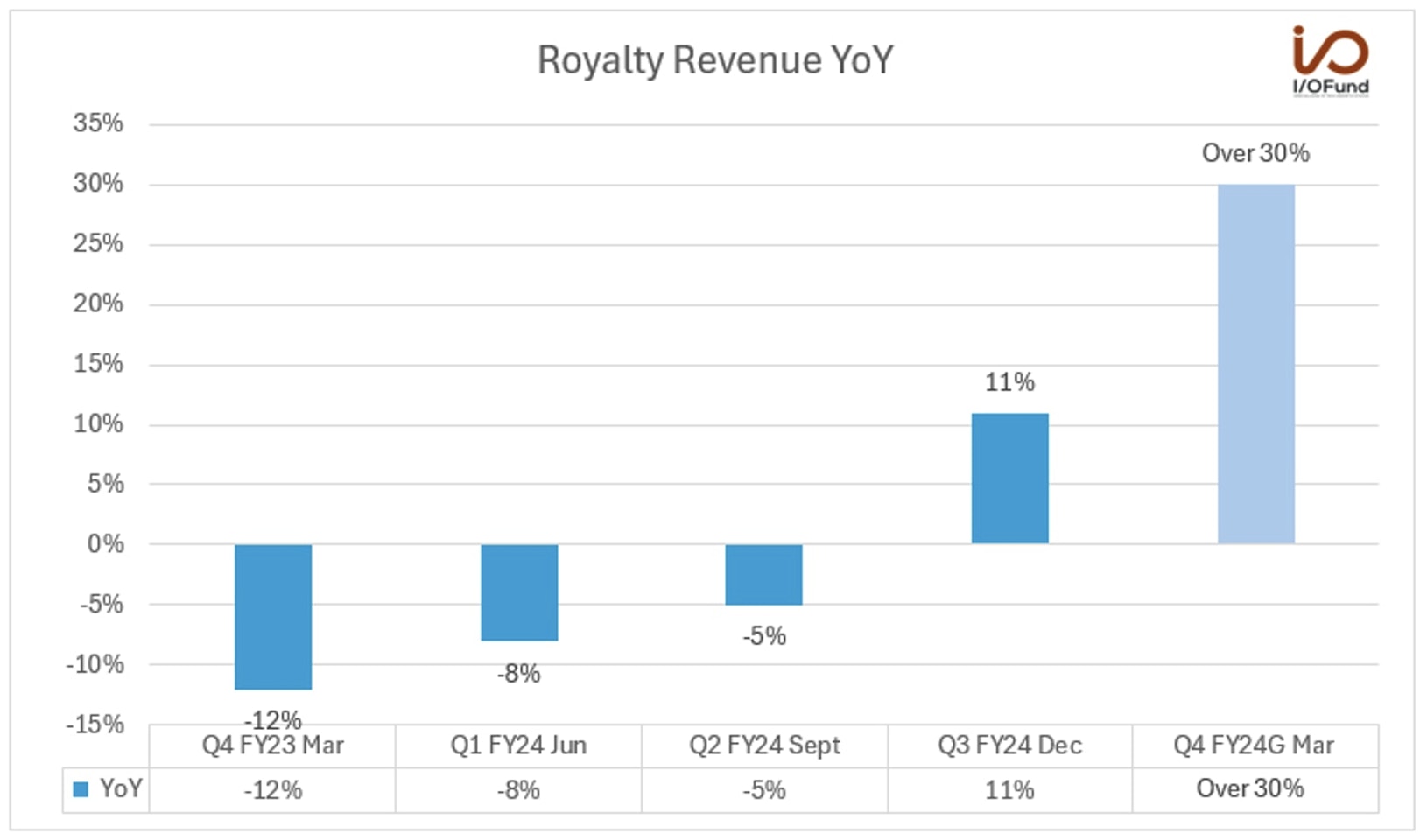

Arm reported record royalty revenue, thanks to its higher value v9 technology and market share gains in cloud server and automotive markets. Royalty revenue rebounded to 11% YoY growth to $470 million from a decline of (5%) and (8%) in the previous two quarters.

Management’s guide for the next quarter is to grow over 30% YoY, due to a weak comp against the “bottom of the industry wide inventory correction that occurred in prior year Q4.” On a sequential basis, royalty revenue was guided to increase by the mid-single digits.

Source: ARM

CFO Jason Child explained that the “sequential growth is mainly coming from increasing penetration of Arm v9, where royalty rates are on average, at least double the rates on equivalent Arm v8 products. Additionally, we are seeing an increasing amount of Arm technology in chips being deployed and as the amount of Arm technology in chips increases, so does the royalty rate.”

Management increased its revenue guidance for the next quarter by $95 million to a range of $850 million to $900 million, representing YoY growth of 38.2% at the midpoint. This strong upward revision was due to the points discussed earlier, including the rebound in royalty revenue and the higher revenue opportunity from AI. Analysts expect revenue to grow 37.4% YoY to $869.88 million in the next quarter and 27.9% in the June quarter.

Source: Seeking Alpha

FY2023 revenue ending March declined by (0.9%) YoY to $2.679 billion. Analysts expect FY2024 revenue to grow 18.7% YoY to $3.18 billion and 23.9% YoY to $3.94 billion for FY2025.

RPO

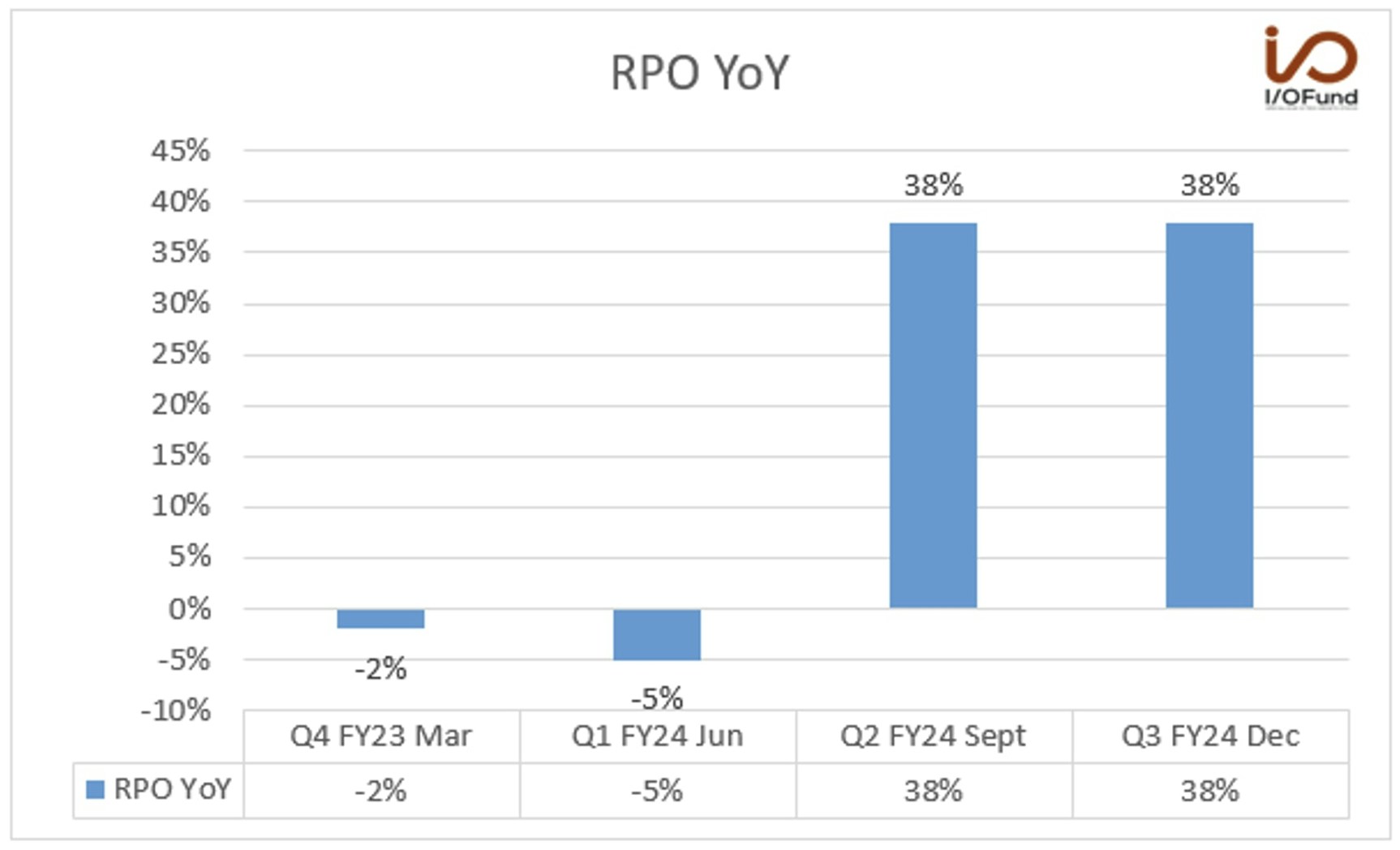

Remaining performance obligations (RPO) grew by 38% YoY to $2.43 billion, helped primarily by high-value license agreements and renewal of long-term customer agreement. As per the shareholder letter, “We expect to recognize approximately 28% of RPO as revenue over the next 12 months, 26% over the subsequent 13-to-24-month period, and the remainder thereafter.”

Source: ARM

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Margins

Gross margin was 95.6% in the recent quarter compared to 96% in the same quarter last year. Adjusted gross margin improved 50 basis points YoY to 96.8%.

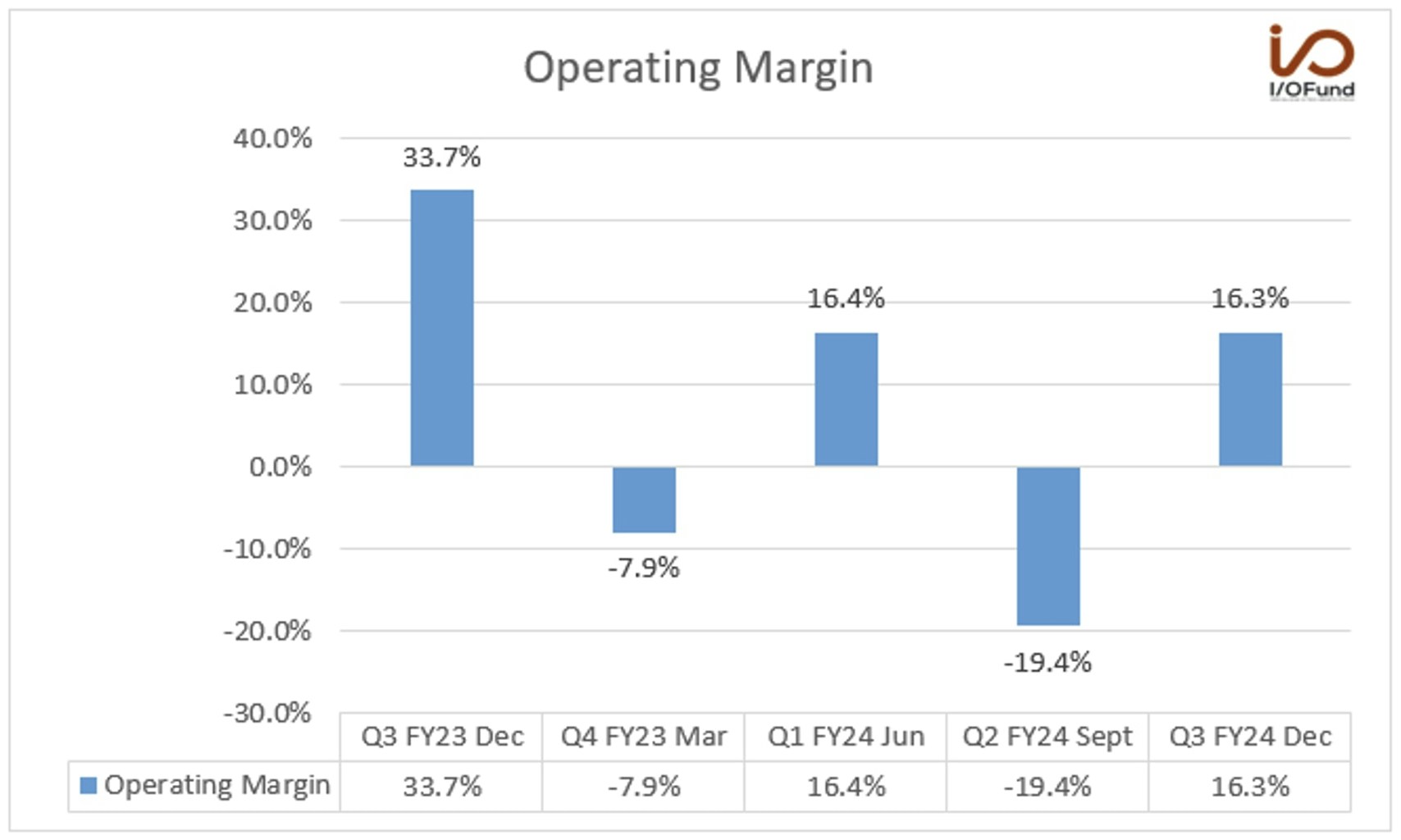

Operating margin was 16.3% compared to 33.7% in the same period last year. The operating margin was lower due to the increase of R&D expenses from an increase in engineering headcount and SG&A expenses from increase of non-engineering headcount.

In the Sept quarter, the operating margin was low at (19.4%) due to increased R&D expenses, stock-based compensation, and IPO-related expenses. SBC was higher than it is expected to be in future quarters as the IPO triggered a one-time expense for previously granted shares. SBC in the September quarter was “$509 million with $19 million in cost of sales, $343 million in R&D and $147 million in SG&A.” The future SBC run rate “will depend on a number of factors, including the share price, but is currently expected to be between $150 million to $200 million per quarter.” At the midpoint, this will be about 20% of revenue.

Adjusted operating margin was 43.8% compared to 39.9% in the same period last year and 47.6% in the Sept quarter.

Source: ARM

Net margin was 10.6% compared to 25.1% in the same period last year and (13.7%) in the Sept quarter. The adjusted net margin was 39.3% compared to 31.1% in the same period last year and 46.9% in the Sept quarter.

Valuation and Risks

Arm’s IPO lock-up period expired on March 12th, so there is risk of volatility in the coming months. Arm is wildly expensive, and it’s this ultra-premium valuation that leads to elevated downside risk for investors, especially now that SoftBank’s IPO lock-up has expired.

Arm was previously listed from 1998 to 2016 when it was taken private by SoftBank Group, and it holds about 90% of the outstanding shares. Arm’s current valuation of $133 billion (90% of that is ~$120 billion) is significantly higher than SoftBank’s current market valuation of $86 billion. The lockup expiration frees up SoftBank’s 90.6% (~930 million shares) stake, allowing SoftBank to lock in gains on Arm after acquiring the company in 2016, should the holding company decide to do so.

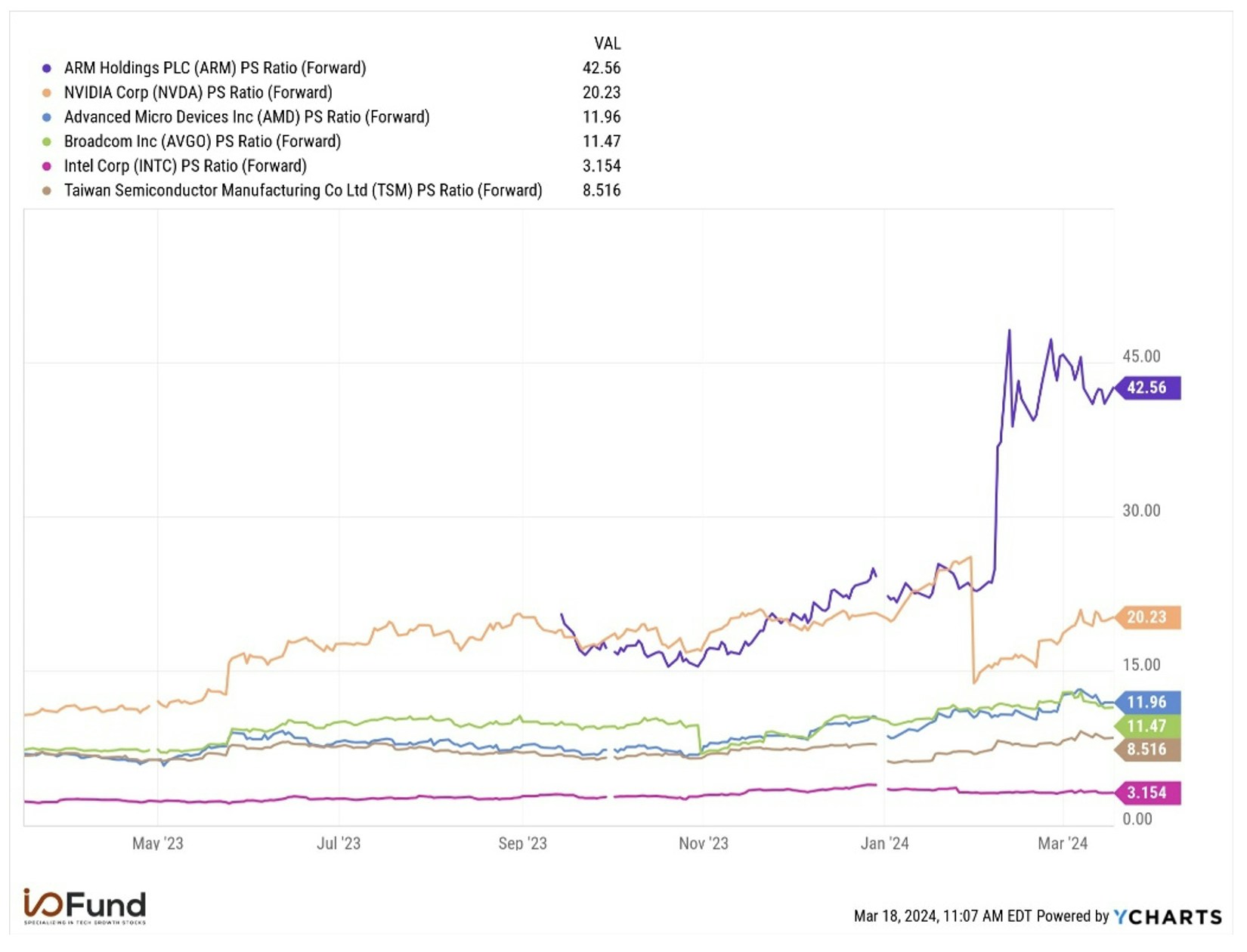

Arm’s shares have doubled since its IPO in September 2023, and it is currently trading at a forward P/S ratio of 43x, far higher than AI semiconductor companies that have much higher growth. For as much as Nvidia is being called a ‘bubble’, Arm is trading at more than double its forward P/S multiple of 20x. Meanwhile, AMD and Broadcom, also followed closely for AI potential, are trading in the 11x P/S range, or one-quarter of Arm’s multiple.

Source: Ycharts

Though Arm’s licensing and royalty model allows it to have a superior gross margin profile relative to its GPU customers, it does not have the same hypergrowth profile that will allow it to command such a multiple, let alone expand on such a multiple to provide gains for investors at these levels.

Nvidia is expected to see 81% revenue growth in FY25 (Q1 beginning in February) to more than $110 billion, with similar earnings power, whereas Arm is expected to record just 24% revenue growth to $3.95 billion. Despite tens of billions in revenue growth next year for Nvidia, not to mention other AI chipmakers underpinned by Arm’s designs, Arm is expected to only see $800 million in revenue growth. Even with a beat above the $800 million, this is not nearly enough to support the $60 billion gained in valuation since Arm’s earnings report.

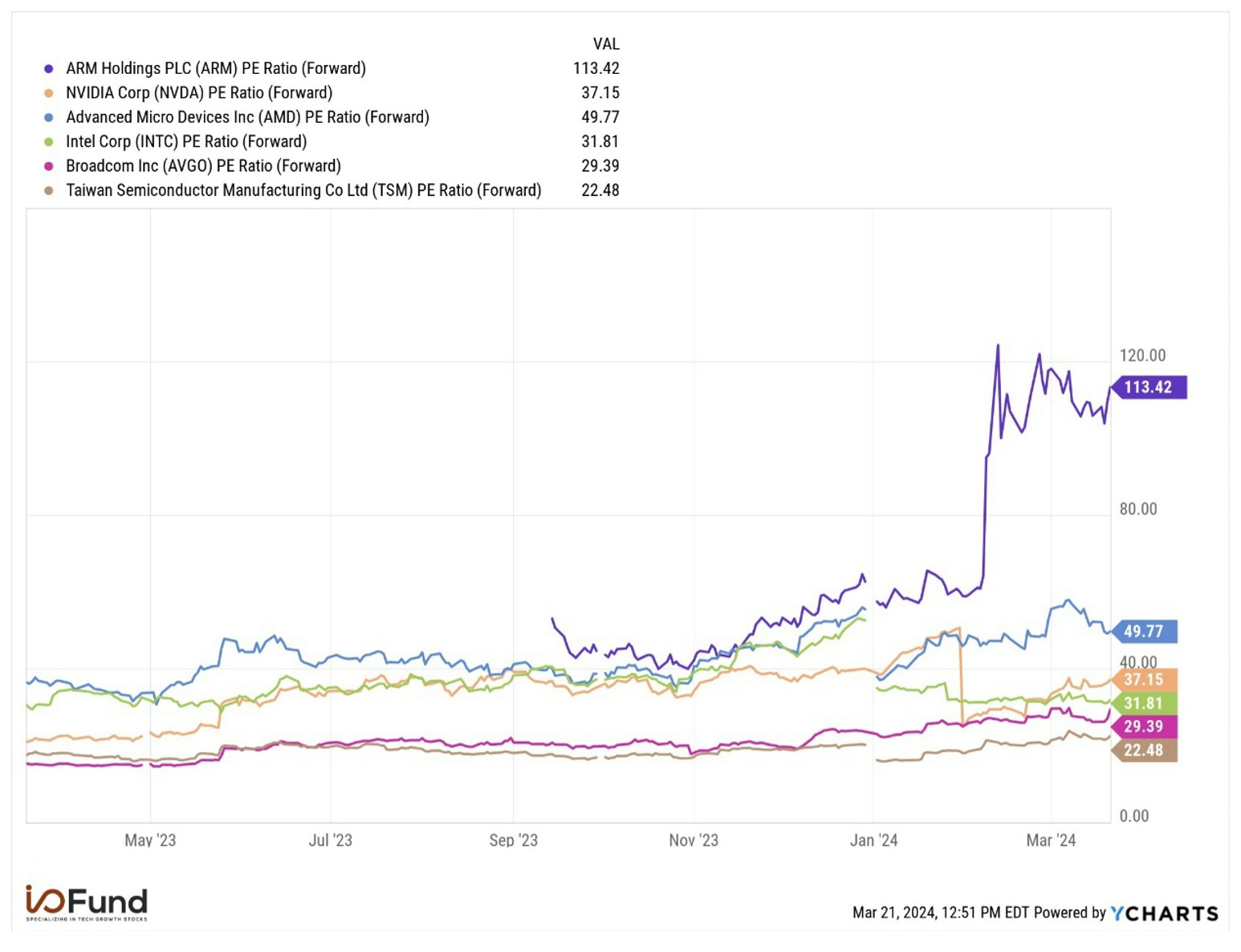

On the bottom line, Arm still trades at a significant premium to peers. Arm is currently trading above a 113x forward PE, more than double AMD’s 50x multiple and triple Nvidia’s 37x multiple. Looking ahead to Arm’s fiscal 2025, Arm is trading at an 86x forward PE with estimated earnings growth of just 27%, compared to 91% for Nvidia.

Source: Ycharts

The rich valuation combined with lockup expiration is the predominant risk, however, the longer-term risk is RISC-V.

Arm is based on lower power instruction sets and hardware, which is also known as a RISC architecture (Reduced Instruction Set Computing). As stated, this contributes to Arm’s approach to power efficiency by reducing the number of instruction sets required. Intel and AMD’s x86 CISC, or Complex Instruction Set Computing, offers more complex instructions that execute multiple operations. This leads to better performance but more power consumption due to the need to decode the complex instructions.

There is a third competitor to Arm and x86 which belongs in the RISC architecture category, called RISC-V. The instruction sets for RISC-V are similar to Arm’s yet RISC-V is open source and is also very new with an official launch in 2019. Compare this to Arm, which was founded forty years ago. RISC-V emphasizes register access over direct memory access, which may be more suitable for parallel processing.

It’s unlikely that RISC-V overtakes Arm in the near-term but it could become a serious contender in future years – some of Arm’s customers support RISC-V, which could limit Arm’s ability to raise prices.

Conclusion

Strong tailwinds for growth exist in Arm’s core markets, notably in AI, automotive and cloud compute chips, while royalty revenue is accelerating on the backs of increased royalties from the v9 design. Despite accelerating key metrics, including revenue, RPO and average contract value, Arm’s valuation poses significant risks, given that it is trading at exuberant levels even relative to the hottest AI chip stocks. In the event the valuation comes down drastically, we’ve done a thorough analysis on Arm as it’s a central player to edge AI and is key to the next phase for AI.

I/O Fund Equity Analyst Damien Robbins contributed to this report.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su