Semiconductor Stocks Q4 Overview: AI Gains Heat Up

April 15, 2024

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 11, 2024,03:58 pm EDT

Semiconductor stocks are standout performers so far in 2024, with investor appetite for AI stocks remaining elevated as AI chip leader Nvidia continues its streak of high growth. Numerous chipmaking equipment and chip stocks outperform the broader indices on a YTD basis – sixteen have YTD gains above 20%.

For years, the I/O Fund has published on semiconductors being the leaders in tech as the building blocks and common denominators for the decade’s largest tech trends, most notably AI and high-performance computing, but also EVs, robotics, 5G, and IoT. Our premium research urged our members to look closely at semiconductors across these trends dating back to 2019.

These emerging trends, coupled with strong demand for AI and HPC applications at the moment, set semiconductors up as an ideal investment, supported by strong free cash flow generation. Below, we update our semiconductor sector analysis to look at which companies have performed well in the most recent quarter, and also which companies stand out on a forward-basis with revenue growth estimates, profits, cash flows and earnings surprises. We also look into key management insights.

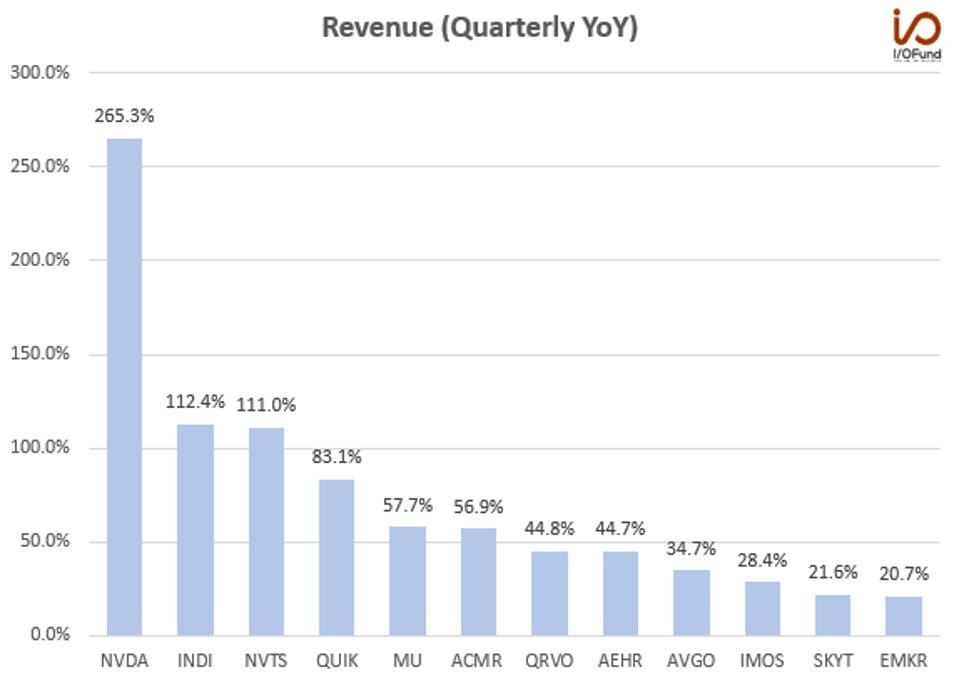

Top Semiconductor Companies with the Highest Quarterly Revenue Growth Rates

Nvidia led the semiconductor sector with 265.3% YoY revenue growth in Q4.

Source: YCharts

It should’ve been an easy guess that AI’s de facto leader Nvidia would sit atop the list here, as it reported more than 265% YoY revenue growth to $22.1 billion in its fourth quarter. Nvidia CFO Colette Kress said that Q4’s “data center revenue of $18.4 billion was a record, up 27% sequentially and up 409% year-over-year, driven by the NVIDIA Hopper GPU computing platform along with InfiniBand end-to-end networking. Compute revenue grew more than 5x and networking revenue tripled from last year.”

AI fueled gains outside of Nvidia as well – Micron is emerging as a big winner from surging AI demand. Micron’s recovery looks to be in full force as it reported nearly 58% revenue growth, driven by strong AI demand and increased pricing power stemming from a tighter supply environment.

However, we saw pockets of strength outside of AI – indie Semiconductor and Navitas Semiconductor both reported over 110% revenue growth, with primarily automotive and industrial end markets. ACM Research reported 57% revenue growth, and Qorvo followed with 45% revenue growth due to content gains at its single largest customer.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

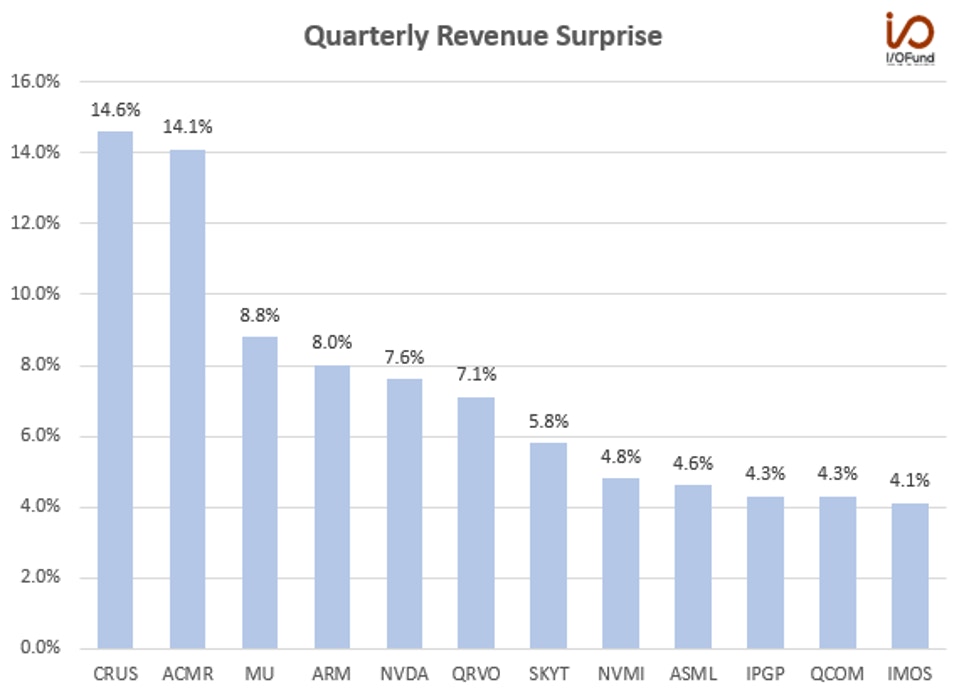

Q4 Revenue Surprise

Cirrus Logic and ACM Research both beat quarterly revenue estimates by more than 14% in Q4, while AI favorites Micron, Arm, and Nvidia each beat by more than 7.5%.

Source: YCharts

Cirrus Logic reported a significant 14.6%, or $79 million, revenue beat in the December quarter (its fiscal third quarter) as it posted a record $619 million in revenue on strong smartphone shipments. This represented 29% QoQ and 5% YoY growth. Management said the $619 million was “significantly above our guidance range, as sales of components shipping and smartphones exceeded our expectations, driven by strength in orders from our largest customer. Shipments stayed strong throughout the quarter, including the first holiday week, and we also benefited from an additional week of revenue in the quarter.” This uptick in smartphone shipments also aided Qorvo, who beat estimates by 7.1%.

Three of the Street’s AI favorites — Micron, Arm, and Nvidia — all beat revenue estimates by 7.6% to 8.8%. Strong AI-fueled memory chip demand aided Micron’s growth in the quarter, while strong GPU shipments and still-dazzling data center revenue growth served as a major contributor to Nvidia’s $1.6 billion revenue beat. Arm’s $61 million revenue beat was driven by record royalty revenue, with royalties for the newest v9 design underpinning the latest AI chips and other advanced smartphone chips, double that of the v8.

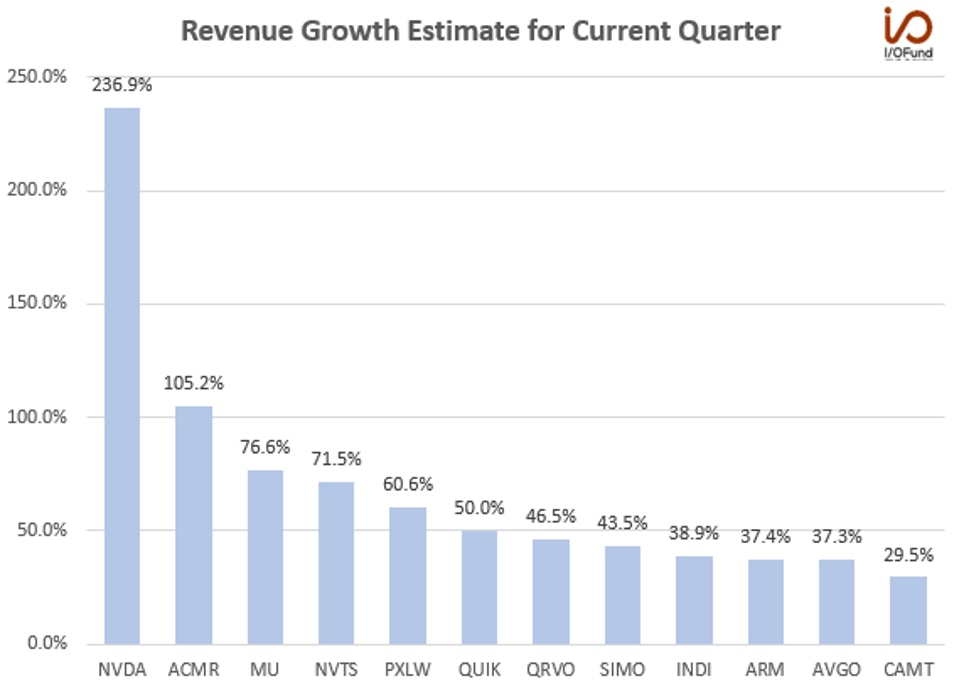

Revenue Growth Estimates for Current Quarter

Source: YCharts

If it’s not obvious which chip stock would hold the crown for the highest estimated revenue growth for Q1, then you’ve been living in a cave.

Nvidia leads the sector with a blazing 237% estimated revenue growth rate for Q1, to an estimated $24.2 billion. Growth in Q1 is expected to be driven by sequential growth in data center revenues, as Big Tech companies continue to quickly snap up GPUs. Nvidia has been on a streak of beating-and-raising by approximately $2 billion over the past couple quarters, and it will be looking to keep this streak alive in the first quarter. Analysts have had an extremely difficult time pinpointing just how rapidly Nvidia’s GPU sales and revenue growth will be – six months ago, in October 2023, analysts’ Q1 revenue estimate was pegged at $18.4 billion, and now, it’s nearly 32% higher. This is reflective of the unprecedented growth materializing for Nvidia over the past year.

ACM Research is expected to see over 105% YoY growth in Q1, with management expecting a strong 2024 on mature node investment in China and product development progress at multiple customers. However, despite the triple-digit headline growth rate, the $152 million revenue estimate would represent an ~(11%) sequential decline.

Micron’s growth is poised to accelerate from 58% YoY to nearly 77% YoY, as it continues to reap the benefits of this unfolding recovery in the memory market with strong pricing tailwinds. Management said that “AI server demand is driving rapid growth in HBM, DDR5 and data center SSDs, which is tightening leading-edge supply availability for DRAM and NAND. This is resulting in a positive ripple effect on pricing across all memory and storage end markets. We expect DRAM and NAND pricing levels to increase further throughout calendar year 2024 and expect record revenue and much improved profitability now in fiscal year 2025.”

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

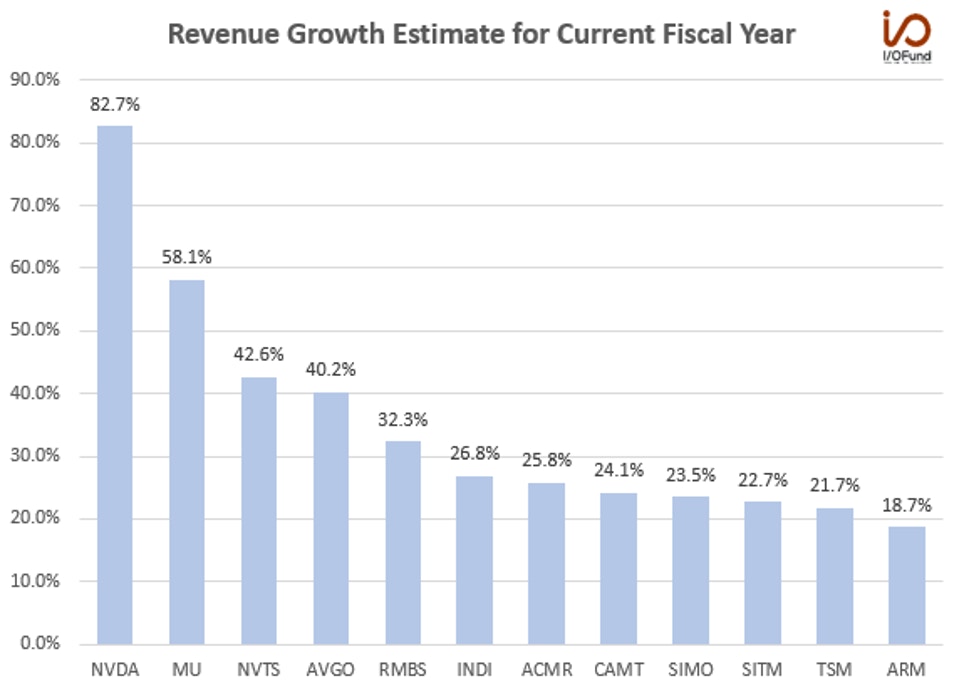

Revenue Growth Estimates for Current Year

Nvidia and Micron lead the sector with estimated revenue growth rates of 82.7% and 58.1% for the current fiscal year.

Source: YCharts

There should be no surprises here, with Nvidia and Micron leading the way with 82.7% and 58.1% estimated revenue growth for the current fiscal year. Navitas’ strong growth in Q4 and expected growth in Q1 are projected to translate to a solid year with nearly 43% growth, while Rambus is expected to record more than 32% growth.

Data center will be the main driver of Nvidia’s growth this fiscal year, with the H200 shipping at the end of the second quarter and the new B200 Blackwell GPUs commencing late in the year. Put in dollar terms, Nvidia is estimated to generate $50 billion in revenue growth this year – assuming data center drives ~90% of that growth, that could represent more than 1 million additional GPUs shipped this year.

What you may have noticed is that the estimated 83% growth for Nvidia is a far cry from the 237% estimated growth for Q1. It’s not that revenue growth will slow on a dollar basis – Nvidia is estimated to see ~$2 billion in sequential growth each quarter this year, but rather it will start to face tough comps in the back half of the fiscal year, when it comes head-to-head with $14.5 billion and $18.4 billion data center revenue prints. This is what will drag on YoY revenue growth rates, from the 237% to an estimated 40% by fiscal Q4.

We’re seeing thematic similarities in the chip companies making the list of fastest revenue growth expectations for the current fiscal year. Nvidia is capitalizing on data center AI demand and TSMC and Arm are seeing tailwinds from this growth. Micron is seeing rising DRAM and NAND prices aid AI strength, while Rambus and Camtek are both poised to capture growth on this memory upswing. Rambus is seeing the data center drive more than 75% of its chip and silicon IP revenue with outlets in DDR5 and HBM, and Camtek is benefiting from increased metrology equipment demand from HBM and AI chiplet customers.

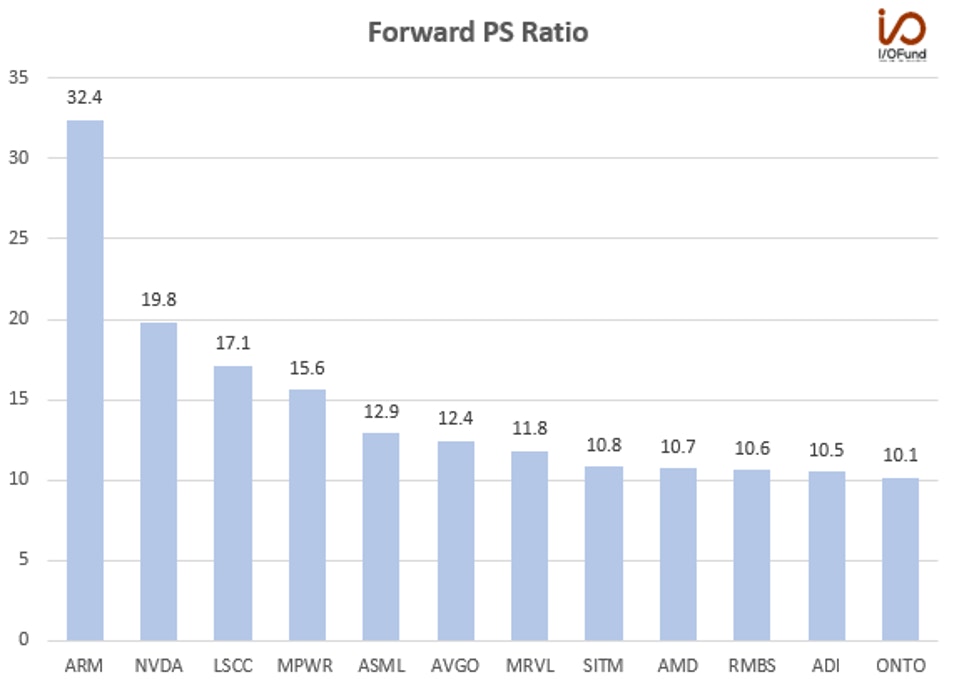

Top-Line Valuation

Source: YCharts

Despite popular belief, Nvidia is not the most expensive semiconductor stock on a top-line (and even bottom-line) valuation. On a top-line, forward PS valuation, Arm is the most expensive semiconductor stock by a wide margin, trading at 32.4x forward sales despite having a forward revenue growth rate of just 18.7%. We discussed Arm’s extreme valuation and how it poses risks to investors to our free newsletter readers last month in the analysis “Arm Stock: AI Chip Favorite is Overpriced.”

Nvidia trades at 19.8x forward sales and arguably deserves this premium valuation due to its unrivaled position on GPUs and the raw earnings power this is driving; in addition, this 19.8x multiple surprisingly is a slight discount to the 21.7x average PS multiple Nvidia has traded at over the past 5 years.

Semiconductors with the highest exposure levels to the unfolding AI megatrends are predominantly among the sector’s most expensive stocks. For example, Monolithic Power is the fourth most expensive at 15.6x forward sales, while ASML and Marvell also feature on the list. Monolithic has seen strong growth in its Enterprise Data segment as a primary power management supplier for Nvidia’s H100 GPU, though it is also recording >20% growth in automotive and ADAS markets.

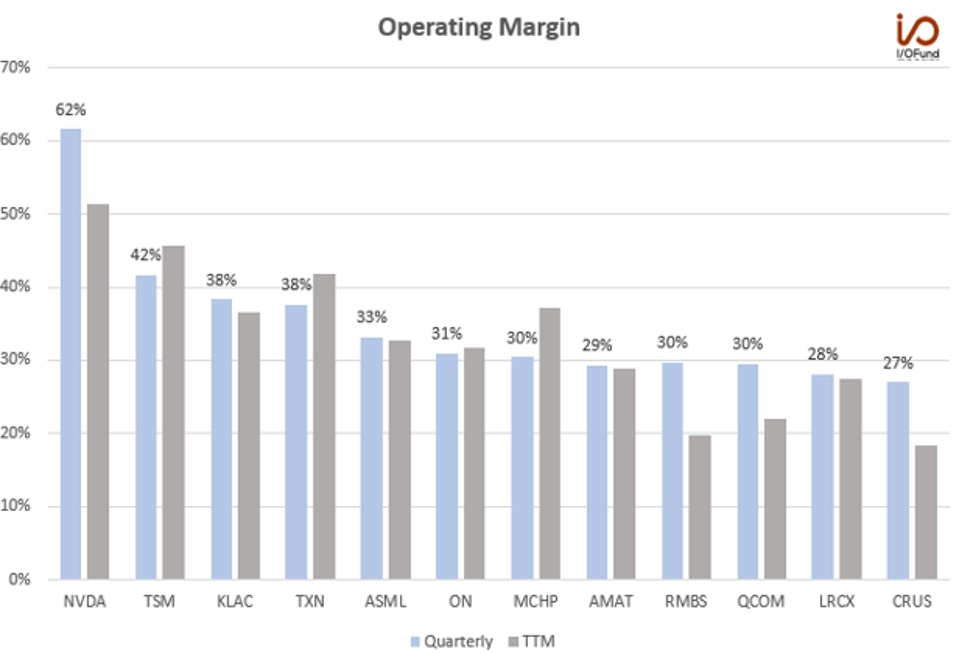

Operating Margin

Source: YCharts

Despite some of the blazing growth rates we are seeing emerge across the sector, only a handful of companies with the highest operating margins are seeing growth translate into increased operating leverage.

Due to the sheer pricing power of its H100 GPUs, Nvidia has seen its operating margin rise to nearly 62% in the most recent quarter, compared to a TTM operating margin of under 52%. This suggests that Nvidia will still feel these positive margin tailwinds over the next few quarters, assuming it can maintain a 60%+ quarterly operating margin as it scales its next-generation GPUs.

Smartphone strengths drove improvements in margins for Qualcomm and Cirrus Logic, while strong royalty revenue growth aided in Rambus’ margin improvement. TSMC is facing some margin headwinds, primarily due to its positioning in the ramp cycle of its 3nm node, which is still in the early stages.

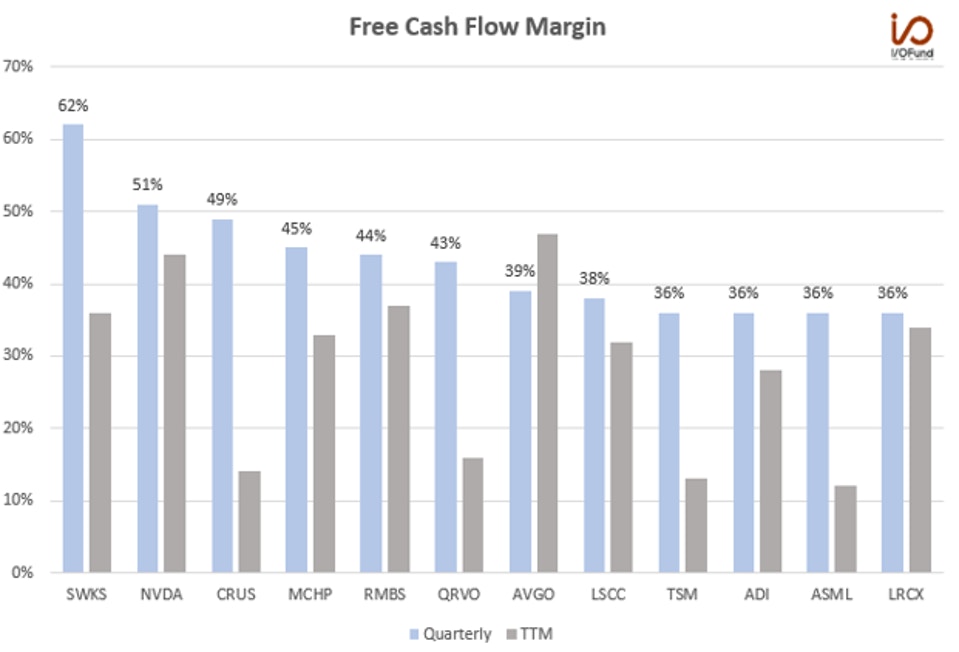

Free Cash Flow Margin

Source: YCharts

Strong free cash flow generation and high FCF margins are a core factor in the chip sector’s attractiveness to investors – not only does strong FCF generation allow companies to reinvest rather heavily in R&D and remain on the leading edge of innovation, but it provides an extra safety net when the macroenvironment sours.

Skyworks led the sector with a 62% free cash flow margin as the company reported record quarterly cash flow metrics. CEO Liam Griffin said the company “continues to execute well and generate robust profitability in light of ongoing macroeconomic volatility” and “delivered record quarterly free cash flow of $753 million, which reflects strong working capital management and moderating capex intensity.”

Taking a broader view of the entire sector, 18 semiconductor stocks reported quarterly FCF margins above 30%, with 9 having a 30% or higher free cash flow margin on a TTM basis. Skyworks reported a 62% FCF margin in Q4, followed by Nvidia at 51% and Cirrus Logic at 49%.

Conclusion

Nvidia has quickly become the market’s most-followed AI stock due to its ‘hockey stick’ data center revenue growth, and it also became the first semiconductor stock to break both $1 trillion and $2 trillion in market cap. However, it’s not the only one putting up strong growth numbers, with Micron expected to see 58% revenue growth this year, and Navitas projected to record over 40% growth.

Strong free cash flow generation has been a hallmark of some of the sector’s top performers. As building blocks for AI and other developing megatrends, semiconductors remain a vital sector to track for tech investors, due to their position at the forefront of AI, strong margins, and strong free cash flow generation.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

The AI Networking Stock That Beat Nvidia by 7X YTD for Returns of 135% YTD

AI networking stock Lumentum is among the key I/O Fund winners in 2026. We allocated heavily to LITE in January—a month before Nvidia backed the company. While most investors couldn’t stomach taking a

Bloom Energy — Our 2026 Top Pick Was the Best Performing Stock in April

April was the best month in six years for the Nasdaq-100. The single best-performing large-cap stock wasn't Nvidia, Microsoft, or Meta. It was Bloom Energy, up roughly 109% in one month. As you'll rec

Inside Nvidia’s $4B Optical Strategy—and Why CPO Changes Everything

Within the AI investment theme, there is nowhere that the supply chain shifts faster than in networking, leading companies to gain content on new platforms or lose incremental share. The reason is str

Is Nvidia Stock a Buy? Why Semiconductor Strength May Signal a Market Top

In this report, we take a deeper look at the technical scenarios, which suggests that Nvidia’s latest high is shaping up to be a potential bull trap. That view is corroborated by the broader semicondu

Nvidia’s $20 Trillion Thesis Is Intact. My 2026 Allocation Isn't

The thesis on Nvidia's hardware moat has played out exceptionally well, but that also highlights one of the biggest risks investors face, which is becoming emotionally attached to a winning stock. Whi

Bitcoin 2026 Price Prediction: Why the Dollar, Global Liquidity and Volume Signal More Downside Ahead

In our last Bitcoin analysis, "Bitcoin After the Cycle Peak: What Comes Next and How We're Positioning", we argued that Bitcoin was closer to a cycle low than most believed, even if one final drop rem

2026 Stock Market Outlook: Cycle Convergence & What's Next

In our last broad market update, the S&P 500 was trading near 6,850, grinding through its fifth consecutive month of going nowhere. I drew a clear line in the sand at the 6,780 level. This was where t

Arm Stock Could Win as Agentic AI Shifts the Bottleneck to CPUs

Arm unveiled an AGI CPU to address one of AI’s biggest bottlenecks, which is orchestration. During the chatbot craze of 2023-2025, GPUs did most of the heavy lifting while CPUs had become an afterthou

Nvidia Stock Prediction: The Path to a $20 Trillion Market Cap is Strengthening

The $20 trillion market cap will not come from GPU unit growth alone, though unit growth remains very important. Rather, the value proposition will increasingly focus on economic output. This marks a

Nvidia Stock to See New Growth Catalyst; 35X Faster AI with Groq 3 LPX

At GTC this week, Jensen Huang stated the revenue opportunity for Nvidia’s artificial intelligence chips may reach at least $1 trillion through 2027, up from a previous target of $500 billion. While t