Why We’re Skipping Coinbase and Prefer Voyager Digital: Overview of Crypto Trading

March 17, 2021

Beth Kindig

Lead Tech Analyst

Voyager Digital is a smaller cap that gives investors exposure to the Bitcoin and crypto trading trend at a reasonable valuation. The company offers zero commissions and more coins than its competitors, including the rumored $100 billion market cap Coinbase that is going public soon, Kraken and Gemini. The stock is listed on the OTC market, which is higher risk than the Nasdaq as these stocks tend to be thinly traded.

Voyager is a zero-commission competitor to Robinhood, and due to many PR mishaps, has opened a door for Voyager to become a replacement for customers who seek fewer politics around their crypto trading app.

Voyager also comes with the added benefit of offering 9% interest on stable coins as the company is a consortium for stable coins, including USD Coin (USDC) and Tether’s USDT, which have surpassed $7 billion in circulation. As such, it provides exposure to decentralized coins like Bitcoin and stable coins based on the fiat system.

Although I am personally in favor of decentralized crypto and not stable coins, Big Tech and the Fed are likely to put immense pressure on adopting stable coins. Voyager allows investors exposure to both at a market cap of $2.18 billion, at time of writing. You can read my Facebook Libra article here where I am especially against this company entering the stable coin market.

Below we explain what makes Voyager a compelling investment, including what it does, how it makes money, valuation, catalysts, management, and potential risks.

Voyager: Zero Commissions, More Coins

As longtime crypto investors, we know all too well the issues around Coinbase and the other sites. The primary issue is the commissions that Coinbase charges, which are exorbitant to say the least. To make a $5000 trade on Coinbase, you will be charged about $80 in commissions. This isn’t competitive in an environment where stocks are traded at $0.

Voyager does not charge commissions on crypto trades and offers 9% interest on stable coins. One thing to note is that Voyager does not offer insurance like Gemini, and that our fund does not hold large amounts of crypto on trading platforms. Instead, we store crypto in cold storage wallets and use trading platforms for trading only. We discuss how Voyager makes money below, the differences in crypto platforms and how investors typically store their crypto below.

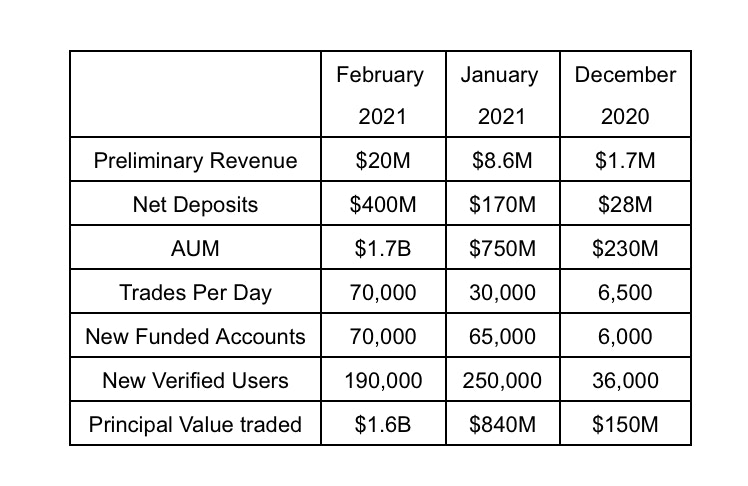

The fallout with Robinhood over GameStop has created an influx of customers for Voyager. Total revenue growth between December and February was over 1000% from $1.7 million to $20 million in monthly revenue.

Please note, my readers often ask me about the volatility of crypto and my answer to this is that crypto promises to be some of my most volatile investments. Stocks and crypto prices can drop 60% or more – and this has happened since my official coverage on bitcoin when it was priced at $12,000 and saw $4,000 before finding a base. You can read my past coverage here on Bitcoin in the summer of 2019.

Financial Overview

Although Coinbase was first to market, there is plenty of room for competitors to disrupt the company’s non-existent customer service and excessive commissions. For those who don’t trade crypto, you might be surprised to know that after paying such high fees, you are given no customer service whatsoever. The I/O Fund prefers Gemini as a commission-based platform as there is insurance offered to offset the cost of commissions.

Voyager is FDIC-insured. However, the crypto held with Voyager is not insured. Gemini, which operates as a trust, has private insurance. Like us, crypto investors generally store their assets on a cold storage crypto wallet, which means it is not connected to the internet. In the event there is no insurance, the risk to cold storage wallets is minimal.

Significant Growth from Robinhood Tailwinds

Crypto investors are a tightknit community and we think word-of-mouth will grow nicely in this niche as it actively looks for new platforms. In December, the company reported $1.7 million in revenue and has grown to $8.5 million in January of 2021.

The company reported $2.5 million in revenue from Feb. 1 to Feb. 4—which we predicted could lead to $17 million in revenue in February. The company exceeded this and reported $20 million in revenue for February.

Assets under management (AUM) grew from $230 million in December to $800 million by early February. Total assets under management by the end of February was $1.7 billion.

Trades per day averaged more than 30,000 for the month ending Jan. 31, up from approximately 6,500 in Dec. of 2020, representing 450% growth in daily trade volume. By early February, daily trades averaged 60,000 trades per day or nearly 1000% growth. In the March earnings report, the company reported a total of 70,000 trades in February.

In January, the value of customer trades increased over 500% to $840 million, up from $150 million in December of 2020. Over twelve months, the overall number of trades increased from 8,500 trades in December of 2019 to 1 million trades in January of 2021, an increase of 117,000%. This number may be irrelevant as most of this is priced in right now, yet we think it's important to look at the ongoing strength before the Robinhood issues.

Basic users grew from 150,000 in December to 440,000 by early February. The company reported 605,000 verified users at the end of February.

Here is the full statement from Steve Ehrlich, cofounder and CEO of Voyager, regarding the Robinhood catalyst and what investors can expect moving forward:

"While we believe our recent business metrics reflect the growing interest in the cryptocurrency ecosystem and long-term benefits of our business model, the unprecedented external events over the past week, including decisions made by competitive products, have brought significant upside to our metrics.

While we don't expect a repeat of the unprecedented external events of the past few weeks that have catalyzed the recent growth, we anticipate continued meaningful growth in our business, including from the pipeline of approximately 80,000 customers who have signed up and that we are presently onboarding.

We remain focused on executing our long-term business plan and expect Voyager will continue to grow the business in a more traditional pattern throughout the balance of 2021. To support this growth, we anticipate increased expenditures to materially increase our employee headcount during this period, while also growing our technology architecture stack in the near-term to accommodate significantly more users."

The company closed a private placement of $46 million on January 21st, 2021.

Voyager has seen 75%+ sequential quarter growth with increasing operating margins in 2020. Per the Investors Presentation, Voyager had a previous goal of reaching $20 billion AUM based on $500 million AUM as of Q1 2021 (this was achieved at nearly 3X the company’s original goal with currently $1.7 billion AUM). The company believes it can achieve 90% CAGR on number of funded accounts and 35% CAGR on average account size.

The company also states it takes $35 to acquire an account, and the company makes $30 per account in monthly revenue—which is excellent unit economics. Customer acquisition costs have averaged from $20 to low $30s per new account, according to Stifel Research.

In contrast, monthly revenue per account has accelerated from $40 per month at the calendar end of 2020 to $80 per month in C2021. A catalog of research reports are available from various funds and analysts covering the company, which is fairly extensive coverage considering the company's small market cap.

Voyager is a strong choice for alternative coins, as the app allows you to trade many tokens that Coinbase or Kraken does not support. For example, Voyager offers Dogecoin, a meme coin pushed by Elon Musk. It also offers interest on Bitcoin, Ethereum, Polkadot, and Chainlink.

Voyager sees its diversification across revenue streams as a way to minimize volatility. The revenue streams include listing fees, interest revenue, alternative coins and major coins.

Quarterly Financials

Voyager reported Fiscal Q2 2021 results March 1 for the period ending Dec. 31. The company had $3.56 million in revenue with $2.06 million in fees and interest income of $1.51 million. There was a net and comprehensive loss of $9 million.

Voyager expects to continue bringing new products to The Voyager platform, according to the report. In 2021 and beyond, executives anticipate adding debit cards, credit cards, stock trading, and the ability to trade on margin. Voyager will also look to grow internationally by expanding into Canada and Europe.

Fiscal Q1 2021 results were reported on November 30th for the period ending September 30th. The company had $2 million with $1.6 million in fees and interest income of $400,000. There was a net and comprehensive loss of $3.97 million or ($0.04) EPS.

The company had cash and cash equivalents of $7.48 million and debt of $1.12 million at the last earnings report, which includes a PPP loan. There was an update for fiscal Q2 2021 on January 5th with quarterly revenue expected to reach $3.5 million.

Voyager also completed a private placement during the quarter, which increases gross proceeds raised during fiscal 2021 to C$13.8 million. It completed the acquisition of LGO, SAS, an AMF regulated entity that provides Voyager with a fully licensed European entity to accelerate its European strategy.

How does Voyager Make Money?

Voyager’s revenue is not dependent on commissions or fees. The company plans to introduce a debit card, credit card, margin, loans, and advisory products over the next year or so. Right now, the business model creates revenue in two specific ways:

1. Smart Order Routing: When you place an order to buy or sell a cryptocurrency, Voyager provides a listed price that you accept. It then connects your order to 12 exchanges. Unlike securities, which by law must have the same price across all domestic exchanges, cryptocurrencies are priced at variable levels. In other words, the same coin can be listed at two different prices at the exact same time.

Voyager uses your order to capitalize on this inefficiency by performing an arbitrage across various exchanges. The profits from such a move would typically surpass any commission or fee, allowing Voyager to provide exceptional pricing. Voyager will thus share the profits from this arbitrage with you in an attempt to execute your order at a lower price than you agreed to.

This business model will likely remain profitable until regulations change or there is too much competition in the arbitrage. Changes to the process would appear in the margins.

2. Voyager operates like a bank. In their terms and conditions, Voyager very clearly states “We will lend, sell, pledge, rehypothecate, assign, invest, use, commingle or otherwise dispose of funds and cryptocurrency assets to counterparties, and we will use our commercial best efforts to prevent losses.”

If you receive a loan from a bank, the loan is used by the bank as collateral for other investments. This creates multiple derivatives on a single asset. This is similar to Robinhood in that the users take on counterparty risk. Should Voyager become insolvent, you will need to stand in line behind other creditors to receive your money back.

For taking on this risk, Voyager offers significant yield in a yield-starved economy. Like a bank, a minimal deposit must be kept to receive this interest payment, which can be as high as 9%. As part of this program, it may take up to 7 days for you to withdraw any crypto from your account. Voyager Digital is engaging in fractional lending practices, which banks have been doing for centuries.

However, Voyager is not considered a bank or a broker-dealer. It does not provide FDIC or SPIC insurance for your crypto if there is a run on the bank, or if something occurs that would prevent them from meeting obligations. To conclude, FDIC insurance applies to the cash you hold at Voyager, but there is no insurance for the crypto held there. We discuss the differences in crypto trading platforms below.

Catalysts: Stablecoins and Global Expansion

Last March, Voyager acquired Circle Internet Financial’s trading app, which provided an additional 40,000 clients. The acquisition strengthens Voyager in offering the USDC stable coin that has $7 billion in circulation. Circle is backed by Goldman Sachs and is the founder of the consortium for USDC. The USDC coin allows global transfer of dollars at an instant and for a very low transaction cost.

The stable coin is part of a consortium that is also sponsored by Baidu, IDG Capital and Bitmain with participation on trading apps, such as Voyager and Coinbase. The supply of USDC has grown by 41% since the start of 2020. A recently announced acquisition of France-based digital asset exchange LGOUY expands Voyager Digital’s reach into Europe. Similarly, the firm is targeting to grow its footprint in Canada. We believe this global expansion should further boost Voyager's platform in terms of customers and revenue.

Valuation

When we first covered Voyager on our premium site in January, the company was trading at a forward P/S of 100. We knew the revenue was growing substantially and the company would catch up to its valuation quickly. This is one reason that we think following people who understand tech growth is essential as Voyager is now reporting $20 million in revenue for the month of February alone. This places Voyager’s valuation at a forward P/S of 10 if we assume $200 million in revenue this year based off February and January numbers.

Compare this to Coinbase, a company expected to open at a $100 billion valuation, per a private auction as reported by Bloomberg. The company’s revenue in 2020 was $1.14 billion, up from $482 million in 2019 for 136% growth. If we generously assume similar growth in 2021, the revenue will be between $2.5 billion and $3 billion. Therefore, even if Coinbase can continue this high level of growth, the company will trade at a 30 forward P/S or higher.

Given these numbers and the likelihood Voyager will surprise to the upside from February’s revenue, we think the valuation on Voyager is more attractive at this time. This comes with risk as Voyager is on the thinly traded OTC markets. However, Coinbase is pursuing a direct listing and these have not performed well historically with both Spotify and Slack trading well below their opening DPO price for nearly two years after listing.

Coinbase has 2.8 million monthly transacting users and 43 million verified users. Assets under management are at $90 billion, per the S-1 filing.

Management

We personally do not see any red flags among management, which can often be the case in smaller cap companies.

CEO Stephen Ehrlich has experience running brokerages and financial companies. He was the CEO of E-Trade Professional Trading arm before it was bought by Lightspeed, and was then the CEO of Lightspeed Financial, CEO of PennTrade, and CEO of Tradier. Oscar Salazar is a Co-founder and he was early in Uber as the CTO.

The one issue that I do see is that they are involved in another company called Pager, a digital health startup. I prefer a founding team with one focus.

Major Differences in Crypto Trading Platforms plus Risks …

Since then, most major exchanges like Coinbase and Gemini have become custodians, which addresses the security risks. Coinbase, for example, keeps 98% of cryptocurrencies held in cold storage, where it is stored securely offline. The remaining 2%, which are held in hot storage, comes with insurance.

Gemini takes these security features a step further. Being classified as a trust, Gemini adheres to strict fiduciary capital reserve and cybersecurity standards by one of the toughest financial regulators, the New York Department of Financial Services.

The company also secured the SOC for Service Organizations Type 1 examination, which is typically reserved for the most stringently run financial services or technology firms. A SOC 2 review from an independent, third-party like Deloitte validates that Gemini is holding itself to high security, availability and confidentiality standards. Because of these additional measures, Gemini has become a favorite exchange/custodian for intuitional investors.

Voyager Digital was hacked as recently as December of 2020, but no customer data or assets were lost as the company shut down its systems when the vulnerability was detected.

As mentioned above, cryptocurrencies do not come with FDIC or SPIC insurance. FDIC protects depositors from banks becoming insolvent, providing guaranteed insurance of up to $250,000. The SPIC protects investors from a broker-dealer going bankrupt, providing insurance up to $500,000 in the unlikely occurrence of a broker-dealer becoming insolvent.

Counterparty risk is a reality for any crypto investor holding their coins at an exchange/custodian. If a custodian does not segregate coins and provide unique private keys that the company cannot access, the risk remains that an investor could lose a portion of their coins in the event of insolvency.

This happened to BitGrail in 2019, an Italian exchange. The courts declared that because all crypto deposits were directed towards the primary address of the exchange, and were not segregated, it was impossible to determine the coins' ownership. Thus, the remaining coins were used to pay off creditors, wiping out most of the individual investors using that exchange.

To be clear, we don't think this will happen with Voyager but are providing a 360-degree view of the risks. We think the crypto landscape has become much more secure since Mt. Gox and BitGrail, and these old stigmas prevent many investors from participating in this sweeping trend.

Coinbase, for example, clearly states that they do not segregate coins and control all private keys. In their terms and conditions, the company states that "Coinbase may use shared blockchain addresses, controlled by Coinbase, to hold Digital Currencies held on behalf of customers and/or held on behalf of Coinbase."

On the other hand, Gemini does segregate coins and states that not even the founders, CEO or president can access coins held in cold storage. They are further in the process of securing privately backed FDIC-like insurance for further protection and safeguards in the unlikely case of insolvency.

Please note, Voyager Digital is a thinly traded over-the-counter (OTC) stock. The OTC markets come with higher risk as there are no central brokers compared to stocks traded on the Nasdaq. As a small cap OTC stock tied to crypto moves, Voyager promises to be a roller-coaster ride.

Conclusion

Coinbase also now has a competitor (Voyager) undercutting them on commissions and on the breadth of tokens. For most crypto investors, the process of holding tokens securely in cold storage is easy enough, and therefore, Voyager Digital is likely to be very popular despite the lack of insurance on crypto.

In our opinion, Voyager is a serious competitor to Coinbase – and most certainly to Robinhood. For our goals and desired gains in the I/O fund, we will take the 10 forward P/S on a company growing rapidly rather than an overpriced DPO at a much higher valuation.

Eventually, Voyager’s growth will settle but we think the value proposition of undercutting Coinbase on commissions will continue to help the app take market share in the word-of-mouth community of crypto traders.

Gemini does well for the high-dollar crypto investors, but this is not the same crowd as Voyager Digital. We see Voyager Digital as a competitor to Robinhood and Coinbase at an attractive market cap. We like the management and the diversification with stablecoins, as the Fed and Big Tech are likely to support stablecoins as time goes on. Therefore, Voyager offers exposure to both and has global expansion on the horizon.

Beth Kindig and the I/O Fund currently owns shares of Voyager. This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

Follow me on Twitter. Check out my website or some of my other work here.

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb