Tesla Has a Demand Problem; The Stock is Dropping

March 07, 2025

I/O Fund

Team

After posting its first annual decline in deliveries in 2024, Tesla continues to face major hurdles to growth in 2025. There are shockingly large declines in Europe and China so far this year, coupled with automotive margins that hit a low in Q4 with more margin pressure likely in Q1. Management has also quietly shifted its tone on 20% to 30% delivery growth, with other segments offering no reprieve as Tesla continues to eat into its gross profit to push deliveries higher.

While optimism has risen for robotaxi services and Optimus robots, neither of the two look to be major drivers of growth in 2025, with initial use cases likely to be internal or small-scale in nature. Tesla continues to hype up a more affordable model, though questions remain about its ability to do so profitably as Tesla has made more progress cutting selling prices than it has cutting production costs.

Stay on the leading edge of AI with I/O Fund’s high-performing tech portfolio, which had 10 positions outperform the Nasdaq-100 in 2024, many held at high allocations, and we are prepping for a strong 2025. Take advantage of our limited-time monthly promotion for up to 20% off our Pro service here to access the I/O Fund’s portfolio, library of research, webinars, and more.

Tesla’s Automotive Growth Stagnates in 2024

Automotive growth stalled in 2024, with Tesla recording a (1%) YoY decline in deliveries for the year to 1.79 million vehicles. Q4 capped off the end to a rather tumultuous year for Tesla, as Tesla sold down a significant amount of inventory after Q1 2024 saw its first YoY decline in quarterly deliveries in four years.

Tesla stock sees its first annual decline in deliveries as growth stagnated in 2024.

China was a strong area of growth for Tesla in 2024 and in Q4, with Tesla’s deliveries in China reaching a record high of 82,927 vehicles in December and 196,902 vehicles in Q4, up nearly 16% YoY and also marking a fresh record. For 2024, China deliveries exceeded 657,000, rising 8.8% YoY. As a result, China accounted for 39.7% of global deliveries in Q4 and 36.7% in 2024, up more than 3 points from 33.4% in 2023.

For 2025, Musk had estimated vehicle deliveries could grow 20% to 30% YoY in Q3, which would correlate to deliveries between approximately 2.15 million and 2.33 million, or an average of at least 550,000 deliveries per quarter. Interestingly, this target was not repeated in Q4, with Tesla saying now that it only expects to “return to growth” in 2025. This subtle shift in tone is easy to miss, but it suggests that Tesla may be on track for 1.85 to 2.0 million vehicles this year, technically returning to growth but at a much lower rate than prior commentary.

This year looks to be off to a challenging start, with early data from across Europe showing plunging sales, while China sales accelerated their decline in February to notch a (29%) YoY drop for the first two months of the year.

ACEA data showed that Tesla registrations fell 45% YoY in January 2025 in the EU, Iceland, Liechtenstein, Norway, Switzerland and the UK, reaching a two-year low, despite broader EV sales rising 37%. In February 2025, registration data showed declines of (42%) to (48%) YoY in Scandinavia and France, while Germany saw sales decline a whopping (76%) YoY after falling (60%) in January.

Tesla stock is facing a tough road ahead in China as sales have slumped to start 2025, with February plunging -49% YoY.

China sales dropped (12%) YoY in January, but accelerated this decline in February, with preliminary data from the CPCA showing sales down (49%) YoY to 30,688 vehicles, the lowest monthly volumes in the country since August 2022. This also marks a (51%) MoM plunge from January’s 63,238 vehicles, and a more than (67%) plunge from December 2024. For comparison, rival BYD’s February sales surged 161% YoY for BEV and PHEVs, with global sales up 56% YoY in the first two months. CPCA data also showed the NEV market rose 82% YoY in February, with Tesla lagging the market by a 131 point difference. Tesla is now offering an 8,000 yuan (~$1,100) insurance subsidy on Model 3 vehicles in China in an effort to revive demand.

Given this weakness already in Q1 in core regions, there are whispers that deliveries could fall to significantly below 400,000. There are mounting indications that Tesla is facing a demand problem, not only within plunging sales across multiple markets worldwide, but also in more aggressive financing perks. Tesla recently launched new financing and free lifetime supercharging perks this week to boost demand, offering 0% APR or zero due at signing for Model 3s and discounts on older Model Ys.

If Q1 does come in weak due to global sales weakness and transitionary impacts to production from the refreshed Model Y, Tesla will have to make up substantial ground in the back half of the year to reach its optimistic targets, as Musk’s prior 20% to 30% volume growth target would already be pushing the upper limits of Tesla’s installed manufacturing capacity.

Tesla’s Margins Have Faced Significant Pressure

Tesla has prioritized affordability to drive growth in delivery volumes and prevent inventory build-ups through 2024, with this coming at the expense of margins. In Q4, CFO Vaibhav Taneja reaffirmed these priorities, saying Tesla is still committed to reducing inventory and vehicle production costs – as expected, this came at quite a cost to margins. Management has also discussed for multiple quarters the plan to launch more affordable models in the first half of 2025, but there’s limited evidence that Tesla can do so in a margin-accretive way that quickly.

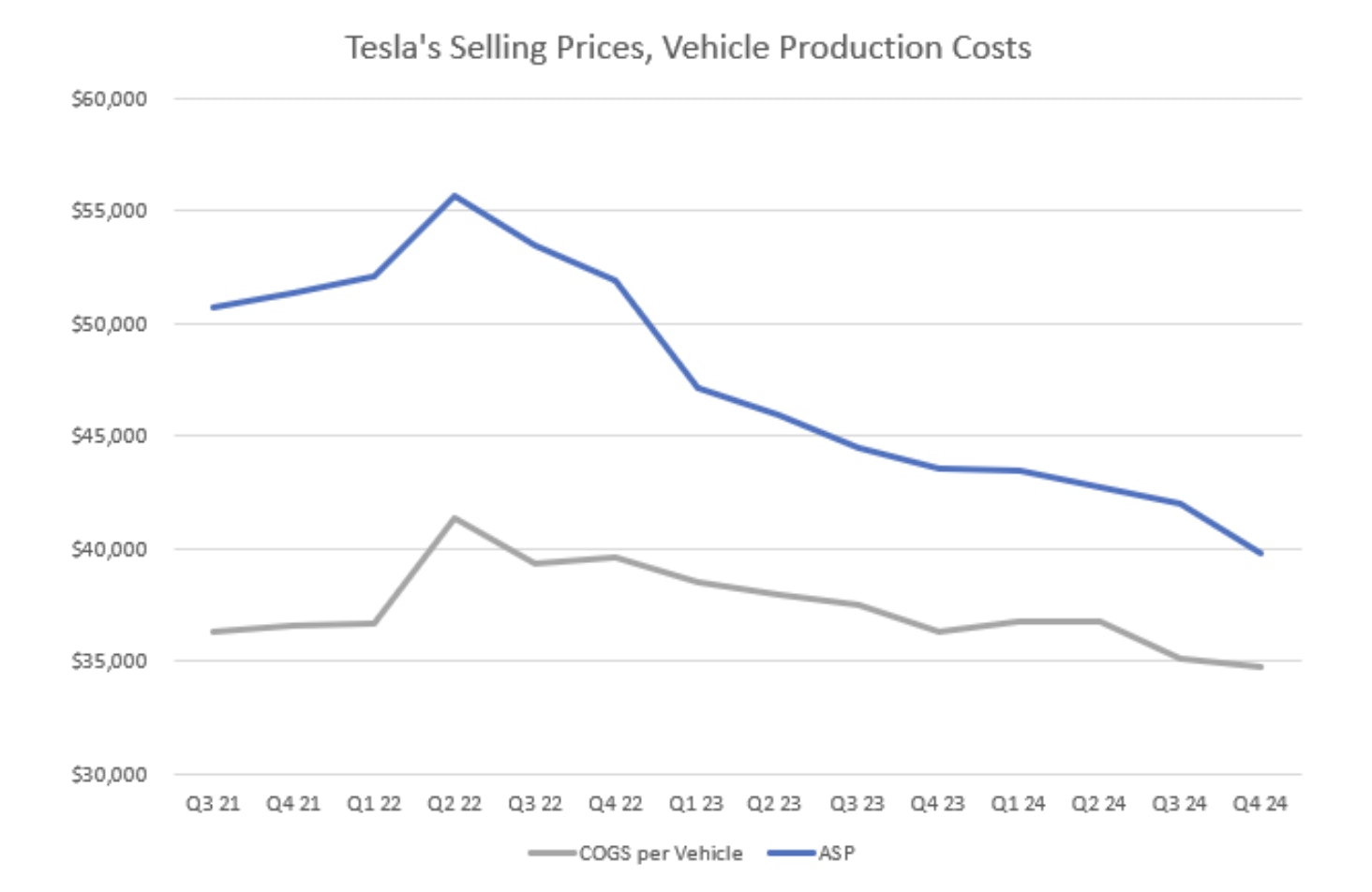

Taneja explained in Q4’s earnings call that Tesla was “able to get our overall cost per car down below $35,000, primarily by material costs,” despite increased depreciation as Tesla transitions to its refreshed Model Y. Calculations show that COGS per vehicle declined just (1.1%) sequentially in Q4 to ~$34,716, or a reduction of $390 from Q3.

Tesla’s actions to aggressively sell down inventories, which declined nearly $2.5 billion sequentially in Q4 to $12 billion, were possibly due to “attractive financing options but also other discounts and programs which impacted ASPs.” As a result, ASPs fell (5.2%) sequentially to $39,818 in Q4, a decline of approximately ($2,174) from Q3. This was the largest QoQ decline in ASPs since Q1 2023. Essentially, Tesla reduced production costs at less than 1/5th the rate of ASPs in the quarter.

Tesla’s average selling prices declined more than 5% QoQ in Q4 2024, while production costs declined just 1.1% QoQ.

Over the last three years, ASPs have been declining at a faster rate than COGS, pressuring margins quite substantially in the process. Tesla said that it saw a new record for deliveries in the highly competitive Chinese market, which (as we have discussed in our analyses Tesla Sells 33% Of Vehicles Below Average Cost, BYD Pulls Ahead in November 2023 and Tesla’s China Market Share Continues To Slide in December 2023) are detrimental to ASPs and likely a factor in the larger QoQ decline.

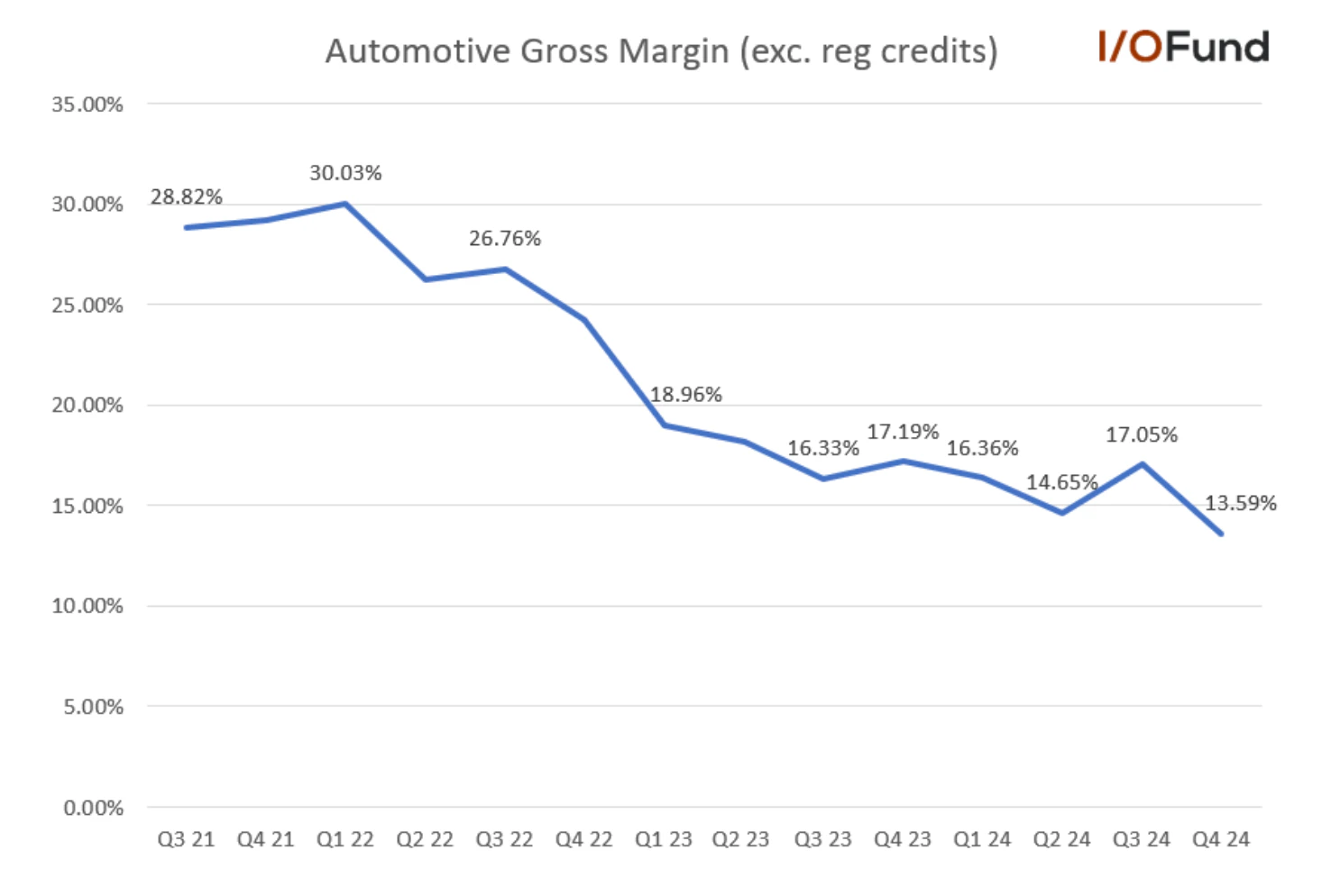

Putting this all together, automotive gross margin dropped more than 3.5 points sequentially to 13.59% in Q4, more than a full point below Q2’s 14.65% margin. This was visible within Tesla’s growth rates – automotive revenues declined (8%) YoY and (1%) QoQ despite a 2% YoY and 7% QoQ increase in deliveries. This was also mostly expected given management had stated that sustaining margins in Q4 would be challenging.

Tesla stock witnessed automotive gross margin (excl. regulatory credits) fall to a fresh low at 13.59% in Q4 2024.

On a per-vehicle basis, Tesla’s average gross profit was ~$5,102 in Q4, down more than (29%) YoY and (26%) QoQ due to the sharper decline in ASP. This is a far cry from the $14,000+ gross profit per vehicle Tesla was recording in late 2021 and early 2022.

As it stands, Tesla risks its per-vehicle gross profit falling below $5,000 in 2025 unless it can quickly drive production costs below $34,000 per vehicle or reverse its decline in ASPs. The aforementioned 0% APR financing perks and other promotional discounts are likely to weigh on ASPs, as was the case in Q4.

Margin Issues to Persist in Q1

Tesla has outlined more headwinds in the first half of 2025, and energy storage has been unable to offset automotive weakness recently, facing similar growth headwinds in Q4 – revenue and gross profit increased just 1.5% and 0.7% from Q2 despite deployments being more than 17% higher.

For Q1, there’s not likely to be much relief on the margin front, as management said that production of the refreshed Model Y kicking off in February will “result in several weeks of lost production” in Q1, and that “margins will be impacted due to idle capacity and other ramp related costs” that will ease once production is ramped. Energy storage is also likely to see margin pressure in Q1, with Shanghai production set to ramp with both Powerwall and Megapack remaining supply constrained.

Sign up for I/O Fund's free newsletter with gains of up to 2,250% because of Nvidia's epic run - Click here

Questions also remain about Tesla’s ability to launch and ramp a more affordable model as promised this year. Tesla has stated for multiple quarters now that it remains on track to launch this vehicle in the first half of 2025, with it being a cornerstone to the previous 20-30% delivery growth forecast given management’s intense focus on improving affordability for customers to drive delivery growth in 2024. Tesla can tout Q4’s production costs as the lowest on record, but the bigger picture shows that Tesla has made very little progress in actually reducing production costs over the past three years. In fact, production costs have declined just (5%), or ~$1,830, since the end of 2021, or a little more than a $150 reduction per quarter on average.

If Tesla’s goal is to make an affordable model at a $25,000 price point and make it profitable at scale, production costs would need to be more than 30% lower than current levels. A 30% reduction in production costs from Q4’s level would equal ~$24,300, or a gross margin of under 3%. To produce a $25,000 vehicle at a ~15% margin, production costs would need to come down to ~$21,750, or nearly 40% below its average cost. Simply reshuffling logistics scheduling to reduce quarter-end weighting of deliveries or relying on materials costs coming down in the face of tariffs is not enough.

And if this is truly something that is feasible to do within the year, it begs the question, why hasn’t Tesla done this yet? There is little evidence that Tesla can flip a switch and bring to market a sub-$30,000 or $25,000 vehicle in the first half of the year without significant damage to margins.

The Bigger Picture at Play for Tesla Stock is Eroding Earnings

While I have heard numerous times that discussions on margins are short-sighted and that the bigger picture for Tesla is the long-awaited autonomous driving and robotics growth curve, I want to make clear that margins have led to a significant erosion in Tesla’s earnings power over the past few years.

At the beginning of 2023, Tesla was expected to earn $8.50 in earnings per share in 2025. At that time, automotive gross margin had actually contracted 5 points YoY, down from 29.2% in Q4 2021 to 24.3% in Q4 2023. To put it another way, Tesla was generating more in automotive gross profit at half the scale.

In Q3 2021, Tesla generated $3.67 billion in automotive gross profit, or $3.24 billion excluding leasing and regulatory credits, with deliveries of 241,391. In Q4 2024, Tesla generated $3.29 billion in automotive gross profit, or $2.39 billion excluding leasing and regulatory credits. This gross profit and margin erosion is why adjusted EPS peaked at $4.07 in 2022 and has since dropped to $2.42 in 2024.

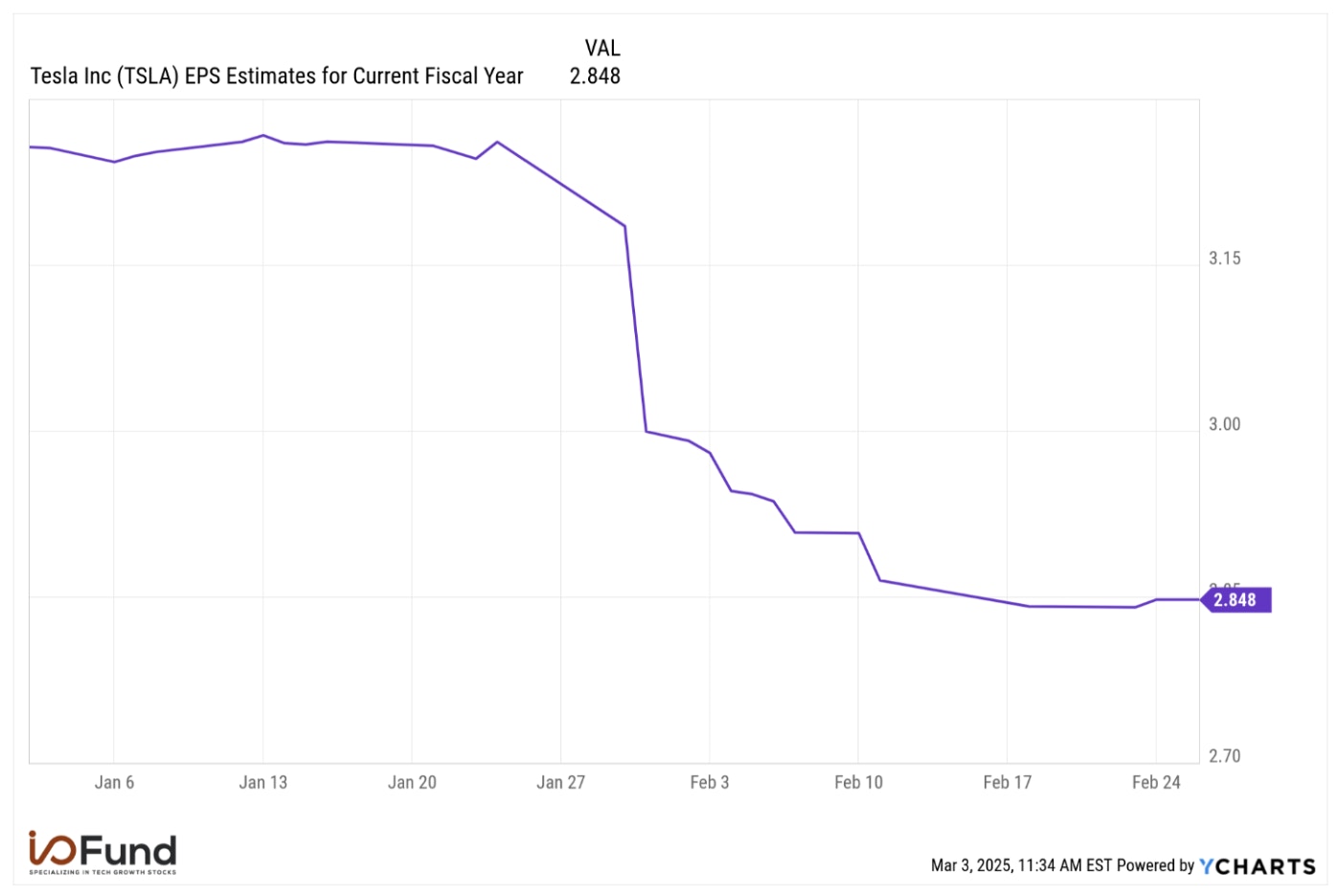

Now, 2025’s EPS forecast stands at just $2.85 at the beginning of March, more than (66%) lower than the estimate from two years ago. It’s also a rather sharp decline this year, down more than (12%) from $3.25 in mid-January.

Tesla stock’s EPS estimates have fallen -12% so far in 2025. Source: YCharts

This has been primarily caused by margin contraction and lower automotive gross profit, which have dragged operating margin much lower. Operating margin peaked at 16.8% in 2022, before contracting to 9.2% in 2023 and now to 7.2% in 2024, with Q4’s operating margin at 6.2%.

Robotaxis, Optimus Inconsequential to Tesla’s Growth in 2025

Robotaxis and Tesla’s Optimus humanoid robots are two core anchors for a majority of the multi-trillion-dollar valuation thesis, with Musk throwing out in Q4’s call that Optimus has “the potential to be north of $10 trillion in revenue.” However, for 2025, even if both are achieved, they’re likely to be only for internal use and not ready for commercialization in a way that will contribute to growth.

Tesla says that it is planning to launch unsupervised FSD as a paid service in Austin, Texas in June, with Tesla’s fleet testing the service out at its factory, from the end of the production line to the destination pick-up parking spot. Musk explained that Tesla is aiming to have unsupervised services with its internal fleet in multiple cities by the end of 2025. Tesla is also seeking the first permit to pave the way for an approval for robotaxi services in California.

However, given that FSD is still Supervised for consumers, analysts had questions about the progress Tesla is making on reaching full autonomy (ie. hands-off, eyes-off), with management explaining that it is close but not there yet:

“We need to be very confident that the probability of injury is low before we allow people to check with their email and text messages. … We're in this perverse situation where people will turn the car off autopilot so the computer doesn't yell at them, check the text messages while steering the car with their knee and not looking out the window. … If you have any problems with the system and when people are not looking, that is a dangerous thing. And that's what we're trying to avoid. The capability is getting there, but it's not fully there.”

Though Tesla laid forth that goal to have a robotaxi service running as soon as this summer, and discussed its ramp profile in Q3, the company provided no major update in Q4 on the Cybercab, its purpose-built robotaxi. Tesla said that it would be aiming for volume production in 2026 with a ramp to at least 2 million vehicles per year, potentially as high as 4 million in the future.

For Optimus, Musk threw out a rather sensational $10 trillion revenue figure, though he shared more details about the robot and Tesla’s production projections. Musk explained that the current production line Tesla is “designing is for roughly 1,000 units a month of Optimus robots. The next line would be for 10,000 units a month. The line after that would be for 100,000 units a month.” He added that Tesla will “probably not” succeed in manufacturing 10,000 in 2025, which is what its internal plan targets, but will aim to ramp production significantly faster than its automotive side.

Musk also predicted that it would not “take very many years before we're making 100 million of these things a year,” though initial use cases for Optimus will be inside Tesla factories, with commercial sales not expected until at least the second half of 2026. If anything, scaling production of either robotaxis or Optimus this year will likely add to costs and impact the bottom line.

Note on Tesla’s Capex

What’s interesting is that even with the $10 trillion revenue potential (and 100 million production numbers) for Optimus and 2 million for Cybercab, Tesla’s capex is not expected to meaningfully increase from 2024’s levels over the next three years. For 2025, 2026 and 2027, Tesla said that it expects capex to be at least $11 billion, compared with $11.34 billion in 2024. Musk had said in Q4 that Optimus’ AI training needs are “probably at least ultimately 10x of what's needed for the car,” suggesting significant amounts of compute would be needed.

In 2024, Tesla’s AI infrastructure assets rose $3.6 billion YoY to $5.15 billion, and it is still working on developing FSD. If you have to scale the compute factor by 10x, while ensuring plants can handle manufacturing millions of Optimus robots, millions of Cybercabs, existing models and a new affordable model, maintaining capex at or above $11 billion annually does not seem sufficient given that Tesla is just now approaching a 2 million vehicle scale annually after having spent close to $50 billion over the past decade.

Conclusion

Musk has been quite vocal about 2025 being Tesla’s “most pivotal year” and possibly the “most important” in its history. Despite strumming up optimism for Optimus and autonomous driving advancements this year, the growth story looks challenged with data for January and February showing substantial YoY declines across Europe and China.

Management’s commentary saw a subtle change from 20% to 30% growth in Q3 for deliveries to now only a return to growth mentioned in Q4, suggesting Tesla is also tempering expectations for deliveries in 2025.

2025’s EPS estimates are already dropping, falling more than 12% since the beginning of the year to $2.85, while revenue estimates have already been revised $4.3 billion lower to $112 billion. New products such as robotaxis and Optimus are unlikely to be growth drivers in 2025, with initial use cases likely limited to small scale and internal operations.

Margins came under more intense pressure in Q4, and are facing even more headwinds from idle capacity in Q1 as Tesla paused production in order to ramp up the refreshed Model Y, while Energy storage provided no relief despite a jump to record deployments in Q4. As Tesla is aggressively pushing for better affordability, it’s putting automotive gross margin at risk of falling into the single-digit range.

Price often bottoms before fundamentals, which means Tesla may be in a buy zone soon. Find out what potential entries the I/O Fund is watching for Tesla and other AI stocks in our upcoming webinar with Portfolio Manager Knox Ridley on Thursday, March 13 at 4:30pm EST. Learn more here.

I/O Fund Equity Analyst Damien Robbins contributed to this report.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb