Big Tech Stocks: Q3 Earnings Preview

October 22, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Oct 19, 2023,10:47pm EDT

Earnings season has officially kicked off, with Big Tech headlining a busy week next week: Microsoft and Google report on Tuesday, followed by Meta on Wednesday, and Amazon on Thursday. Big Tech stocks have seen their dominance over the broader indexes soar this year, with the Magnificent 7 reaching nearly 30% of the S&P 500’s weighting, higher now than at its peak in 2022 and up from 20.0% at the beginning of this year.

In the Nasdaq 100, the combined weighting of Big Tech stocks is even higher, at 44.8%. The Nasdaq 100’s rebalance earlier this year in July dropped the overall weighting of the group from 55% to ~38%, but already, we’ve seen a 6 percentage point increase in just over one quarter.

This outsized influence that the Magnificent 7 has over the indexes is just one of the many reasons that Big Tech earnings reports next week will be some of the most closely watched this season. EPS estimates for the group will be in focus – estimates have all pushed higher during Q3, with Amazon, Meta, and Nvidia seeing some of the largest increases, and investors will likely be assessing how the group stacks up against heightened expectations.

View Post: Click Here

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Microsoft: AI to Help Drive A ‘Noticeable Acceleration’ This Year

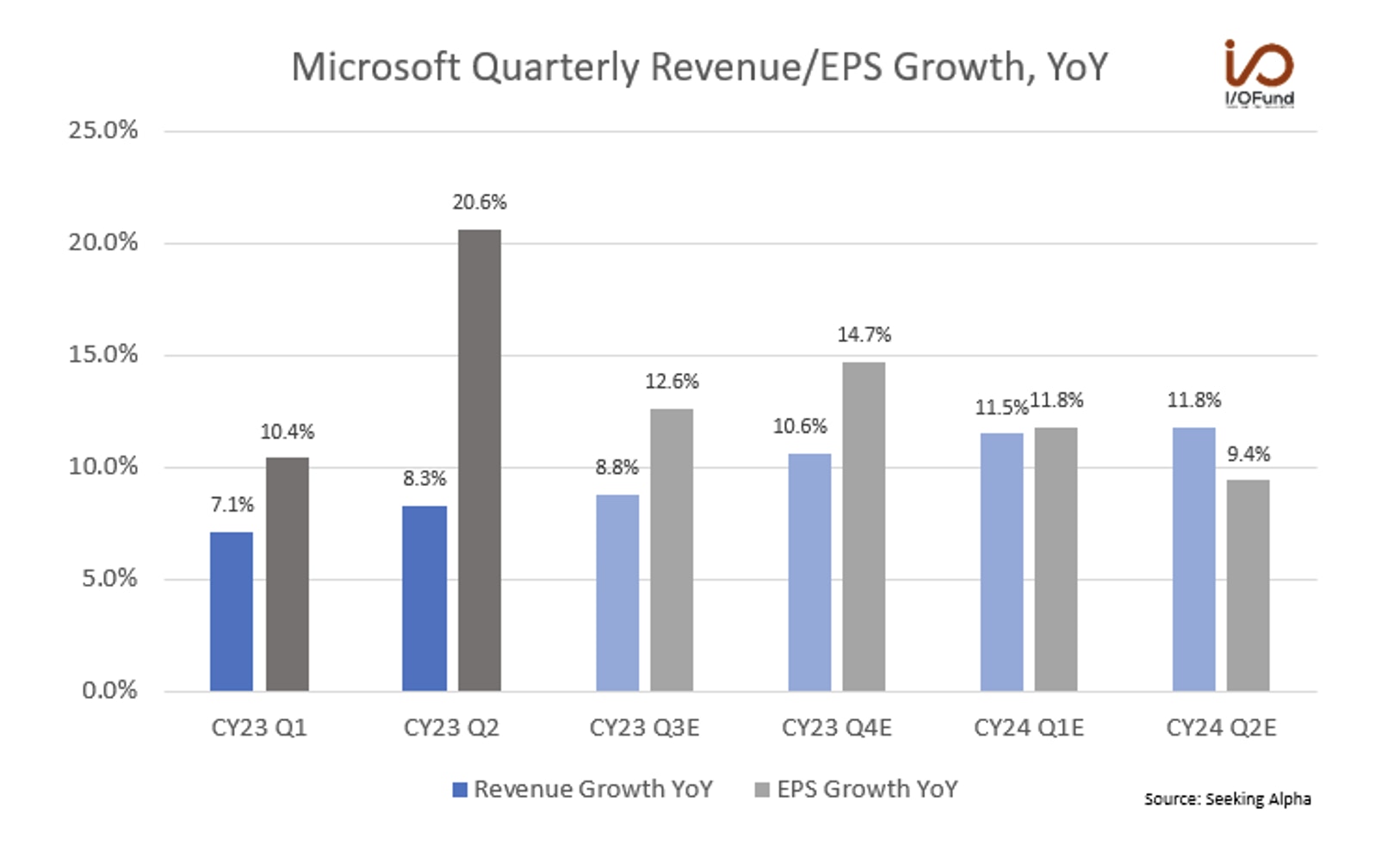

For Microsoft, a noticeable acceleration is expected this year, with revenue growth accelerating back to the low-double digits through FY25. For the quarter, revenue growth is estimated to be about +8.8% YoY to $54.5 billion, with EPS forecast to grow +12.6% to $2.65. Revenue growth is currently forecast to return to +10% to +12% growth over the next three quarters through calendar Q2 2024.

Source: SEEKING ALPHA

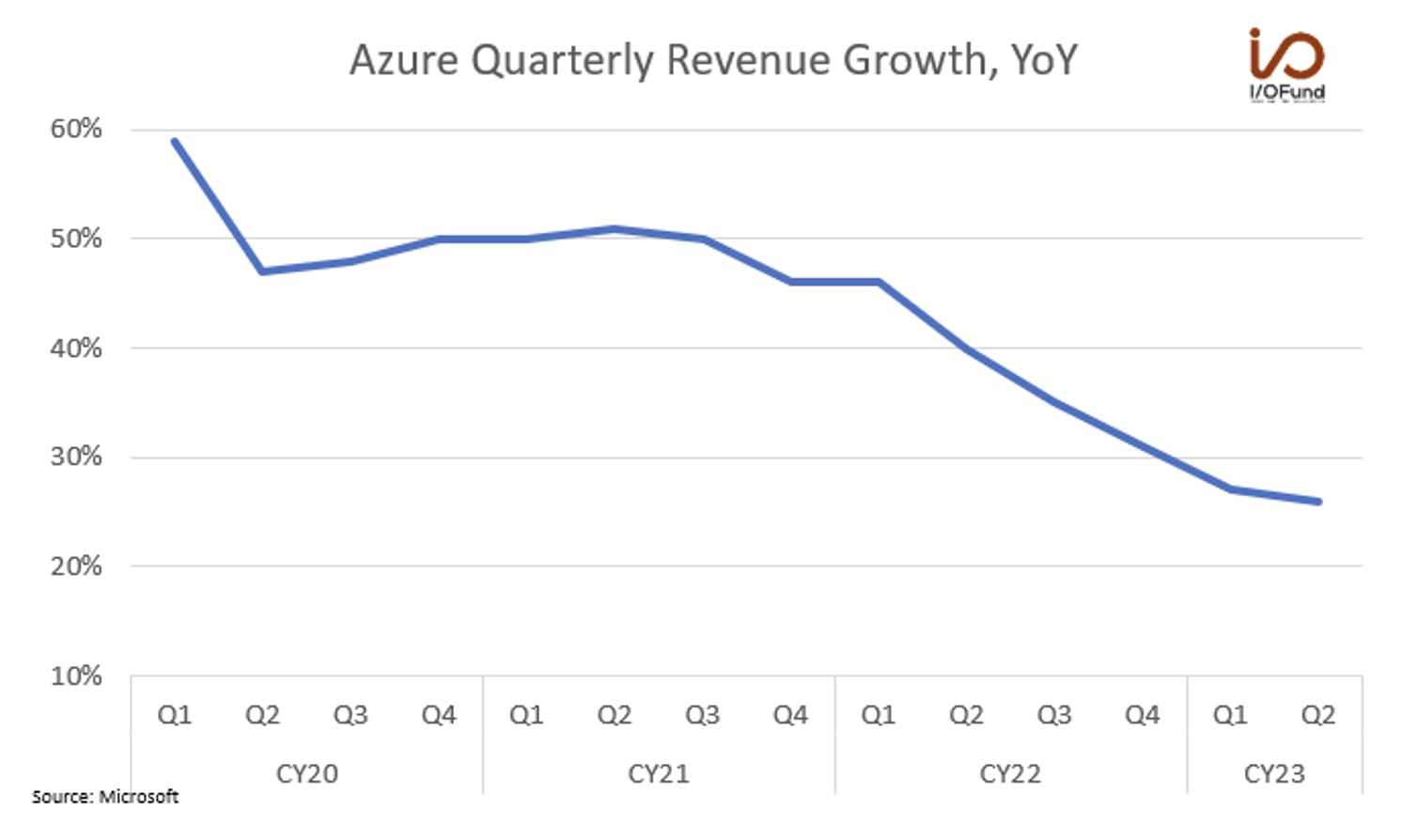

Azure and AI will be two of the key areas to watch, given the overlap between the two. Microsoft is devoting 13% of Capex to AI in 2023, the most among the top cloud service providers.

Azure’s growth in the prior quarter was 27% in constant currency, including about 1% from AI services, a decline from 31% two quarters ago. Excluding currency impacts, growth slowed to 26% from 27%, hinting at a possible inflection point back to higher growth.

Source: MICROSOFT

Microsoft also stands to benefit from its consumption pricing model for OpenAI’s APIs, given that the APIs are all new workloads for Azure this year. Microsoft said last quarter that it had “great momentum across Azure OpenAI Service” with around 100 customers added each day, bringing total customers to more than 11,000.

In addition, commercial subscriptions for Office 365’s Copilot AI assistant are expected to start on November 1, at a $30 per month per user price point, opening up a potential multibillion-dollar revenue opportunity over the next few years, with the first insights likely to come next quarter.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

Alphabet: Search & Cloud Momentum to Continue

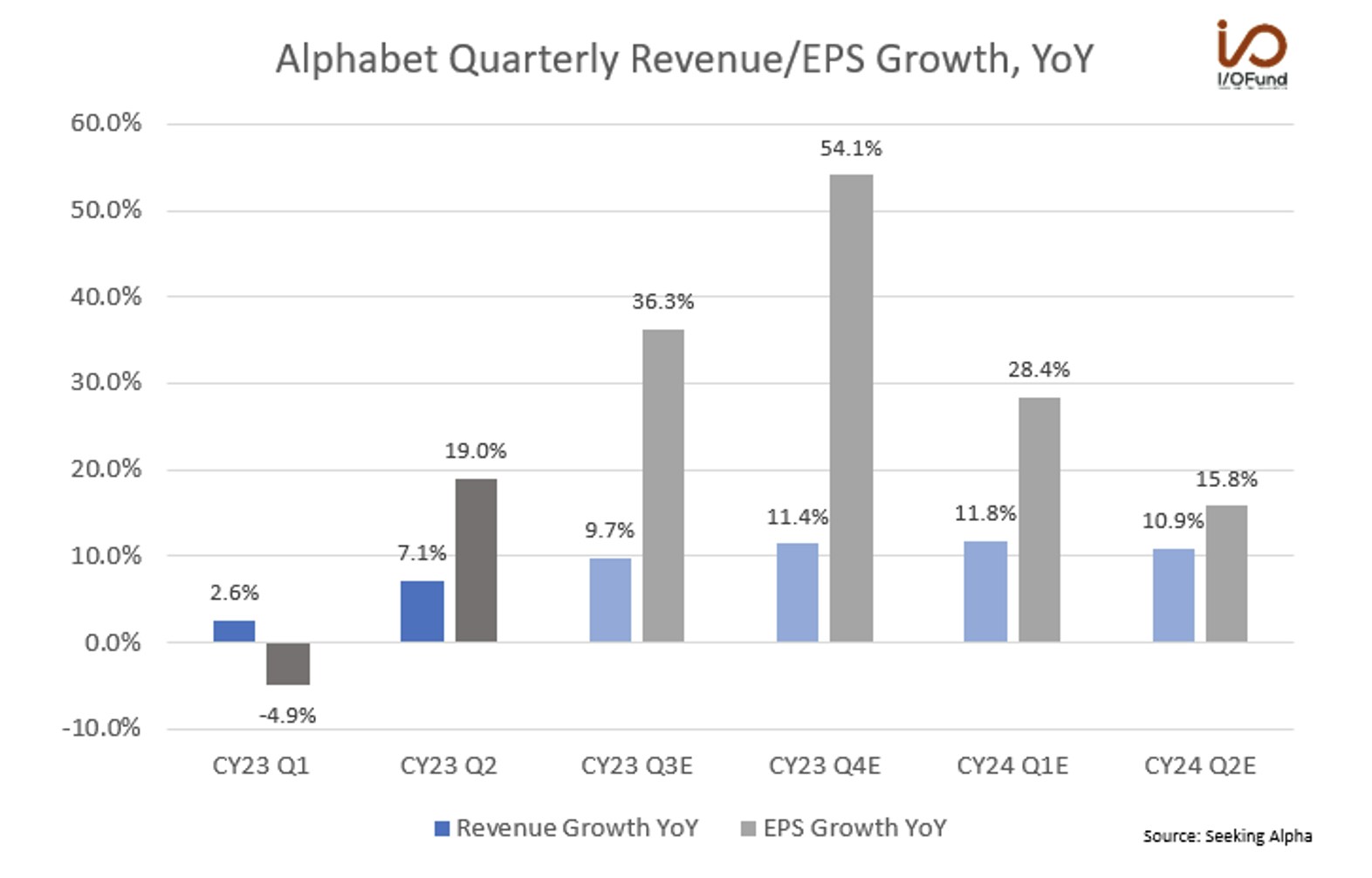

Like Microsoft, Alphabet is expected to see revenues reaccelerate to the low double-digits through Q2 2024, a marked acceleration from forecasts at the beginning of the year. Revenue for Q3 is forecast to rise +9.6% YoY to $75.7 billion, with EPS growing +36.0% YoY to $1.44.

Source: SEEKING ALPHA

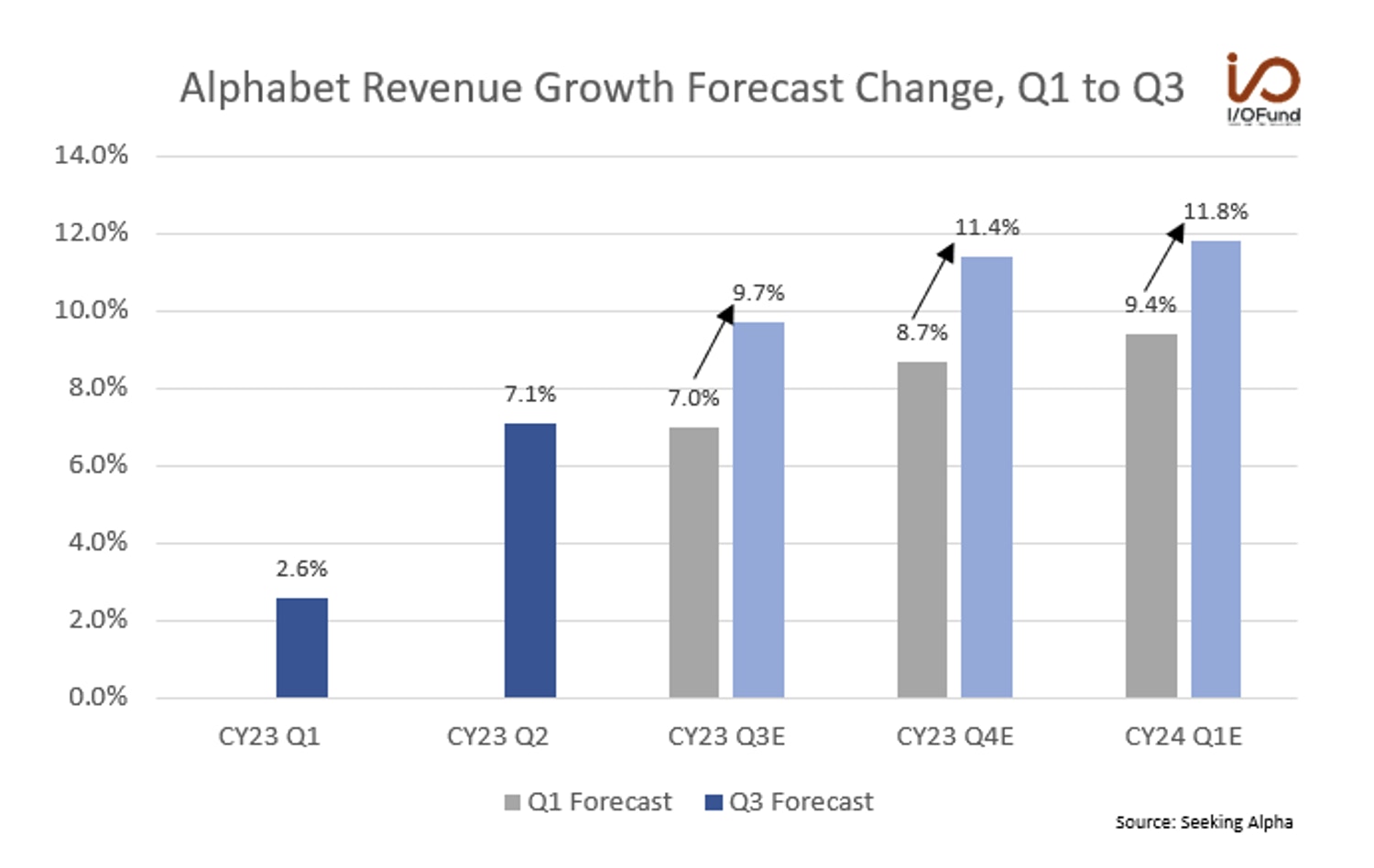

The combination of resilient Search growth, strong Cloud performance, and the integration of AI into Alphabet’s services is driving revenue growth expectations higher. Forward revenue growth rates for the next two quarters have risen upwards of 2 percentage points since the beginning of the year.

Source: SEEKING ALPHA

Search and Other advertising growth is picking up, rising 5.4% QoQ to $42.6 billion, as Google begins “building the next major evolution in Search” with AI integrations driving a higher ROI. As the I/O Fund highlighted previously, Alphabet’s Search “has proven resilient because it provides advertisers an attractive ROI on their ad spend. Looking ahead, Search Generative Experience, [Google’s generative AI-powered search tool], will improve advertisers’ ROI and will likely provide Alphabet additional pricing power. This will also improve their retail vertical” – a trend already surfacing, with Q2’s Search growth driven by retail alongside SGE’s launch.

Google Cloud will also be under the microscope, after posting two consecutive quarters of operating profitability, with operating margin reaching almost 5% last quarter. Revenue for Cloud stabilized at 28% growth YoY in both Q1 and Q2, as the platform remains a leading choice for training generative AI models. As enterprises start to think more deeply about AI and integrating AI across their organizations, Google Cloud stands to benefit in multiple ways – via its large language models such as Bard, its generative AI offerings including the recently launched Duet AI, offering AI model training with multiple AI supercomputers, and by “expanding our total addressable market and winning new customers,” according to CEO Sundar Pichai.

However, Google is in the midst of its antitrust trial, with regulators concerned that Google has been keeping an illegal monopoly on search. Google is reportedly paying Apple nearly $20 billion per year to remain the default search engine on Apple’s devices, are at the forefront of the case.

For a deeper dive into Alphabet and how the Search giant is entering its Year of Execution, read more here.

Meta: Ad Impressions to Drive Revenue Growth

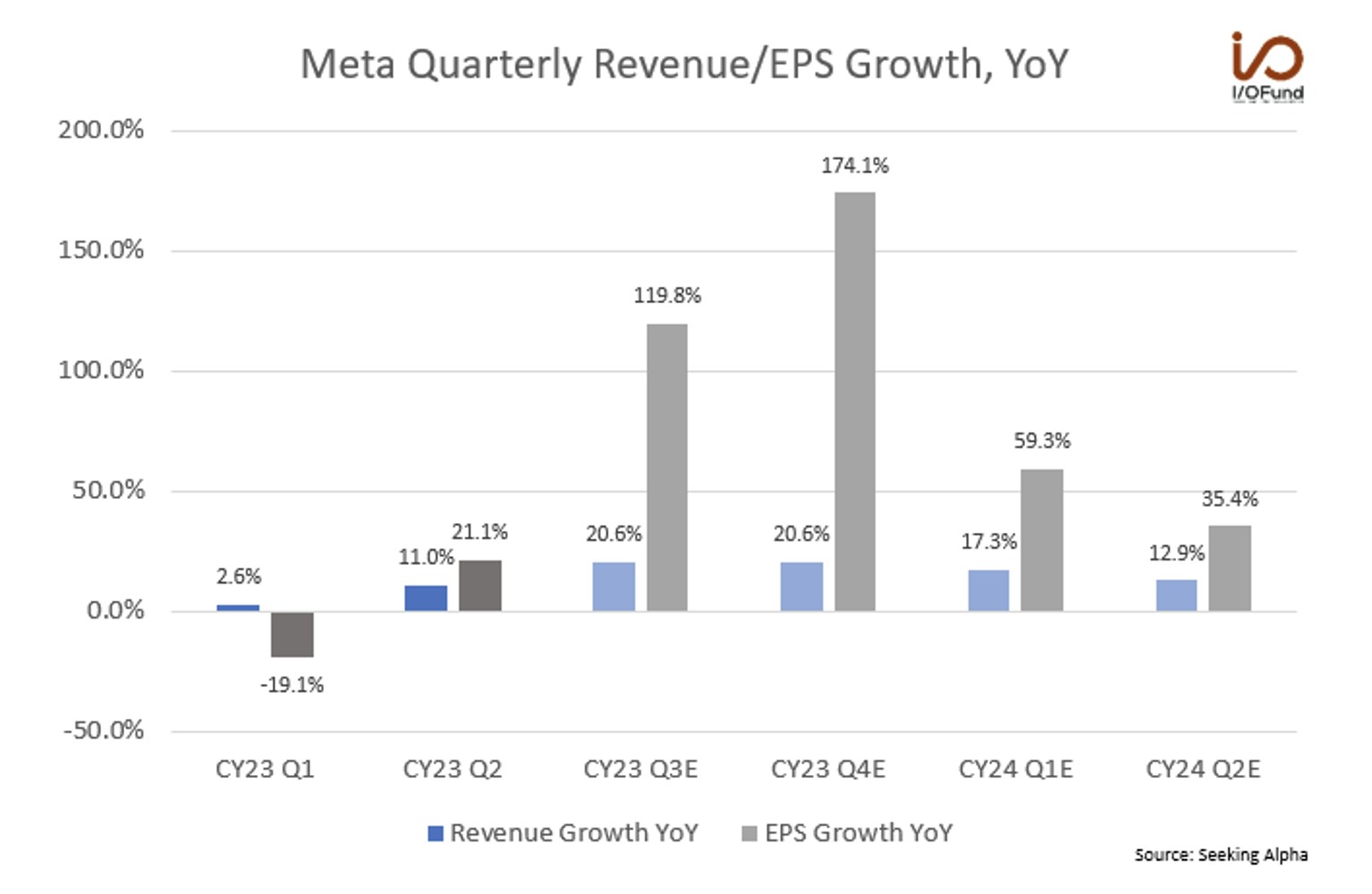

Meta’s Q3 EPS estimate surged during the quarter, rising $0.60 from an estimate of $2.98 on June 30 to $3.58 by September 30. Meta returned to positive growth in Q1 this year, with revenues up +2.6%, and has since seen revenue growth accelerate – Q3 and Q4 are both expected to see YoY revenue growth up more than +20%.

Meta also has seen improvements in operating efficiency this year. Operating margin has expanded 9 percentage points in just two quarters, from 20% in Q4 to 29% in Q2. Revenue growth reaccelerating to more than +20% through the end of the year is set to drive EPS growth in the triple-digits as operating margin expands further.

Source: SEEKING ALPHA

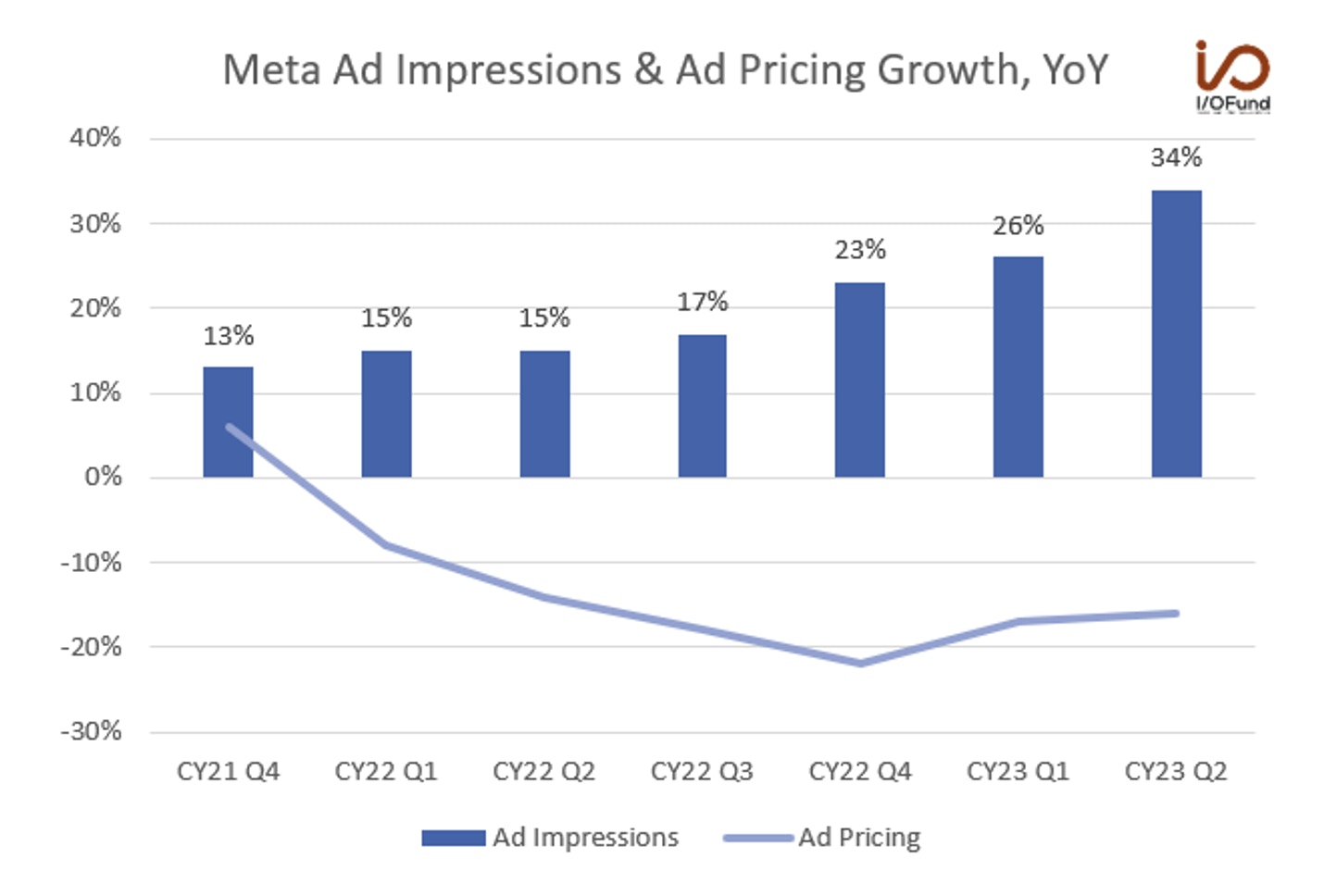

Q3 is expected to be a banner quarter setting Meta up for a strong end-of-year finish: Meta is estimated to post 119% EPS growth to $3.58, with revenues expected to rise 20.6% to $33.4 billion. As an advertising-driven company, with more than 98% of revenues coming from ads, the mix of ad impressions and ad pricing will determine growth. So far this year, ad impressions have served as the primary driver, rising 26% YoY in Q1 and 34% YoY in Q2, offsetting weak pricing, which declined 17% YoY in Q1 and 16% YoY in Q2.

Source: I/O FUND

Over the past four quarters, advertising spend looks to have bottomed out, recovering from Q4’s (-22%) decline, while ad impressions continue to accelerate past 30%. Impression growth has been driven by APAC and Rest of World, which, as lower monetizing regions, have contributed to that decline in pricing. AI is only just beginning to scratch the surface in optimizing ads and increasing ROI for advertisers, and Meta is seeing “strong advertiser demand,” with almost all of its advertisers “using at least one of [its] AI driven products.” Meta is continuing to release new AI advertising products, such as Meta Lattice for predicting ad performance and AI Sandbox for generative AI-powered ad generation.

Amazon: AWS Growth in Focus

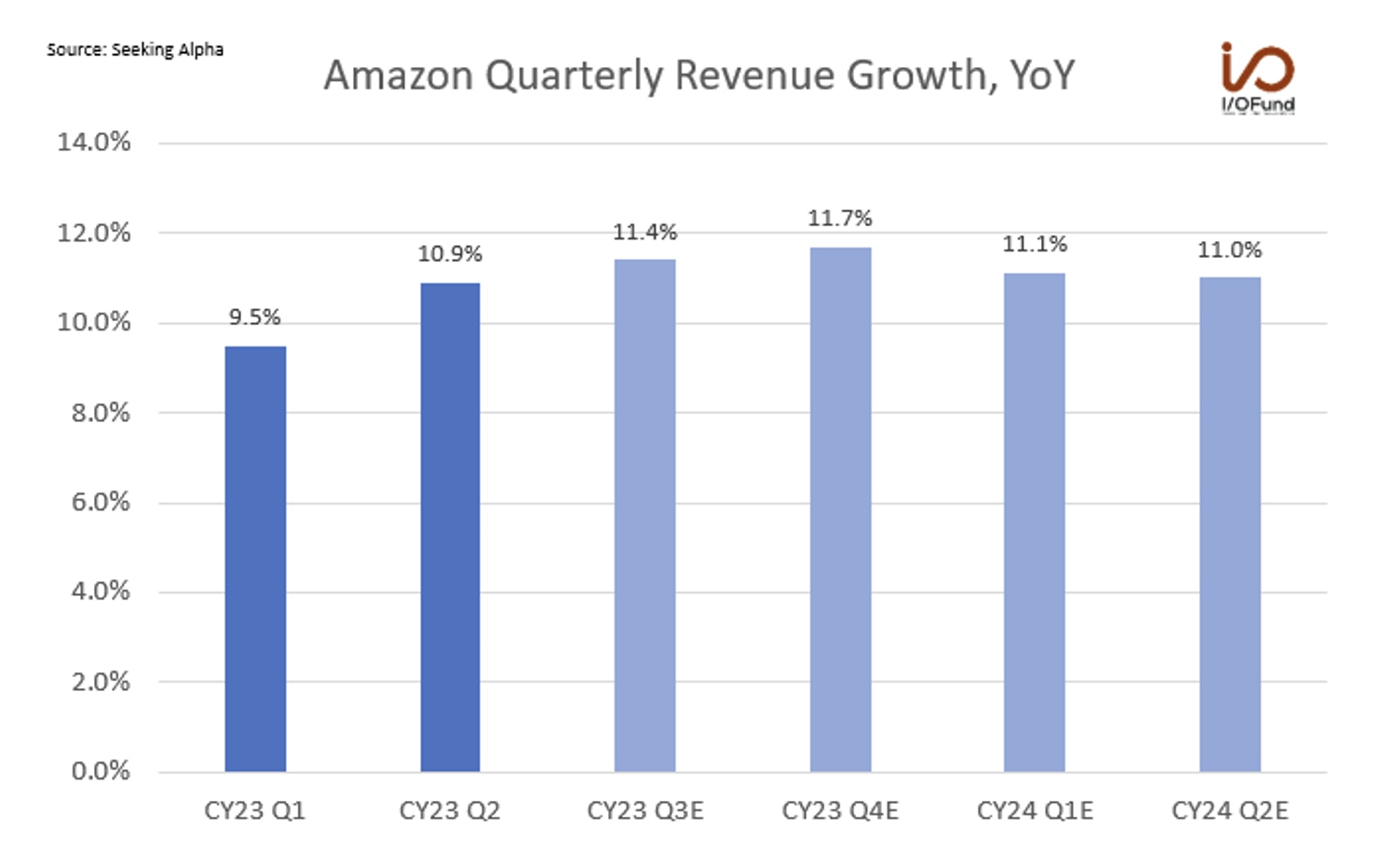

Amazon is expected to see a slight acceleration in revenue growth through the end of the year, with Q3 and Q4 forecast to see revenues increase 11.4% and 11.7% respectively, following Q2’s 10.9% growth. EPS estimates for Q3 point to +114% growth to $0.60, as operating margins for North America are expected to continue a 5-quarter streak of improvement.

Source: SEEKING ALPHA

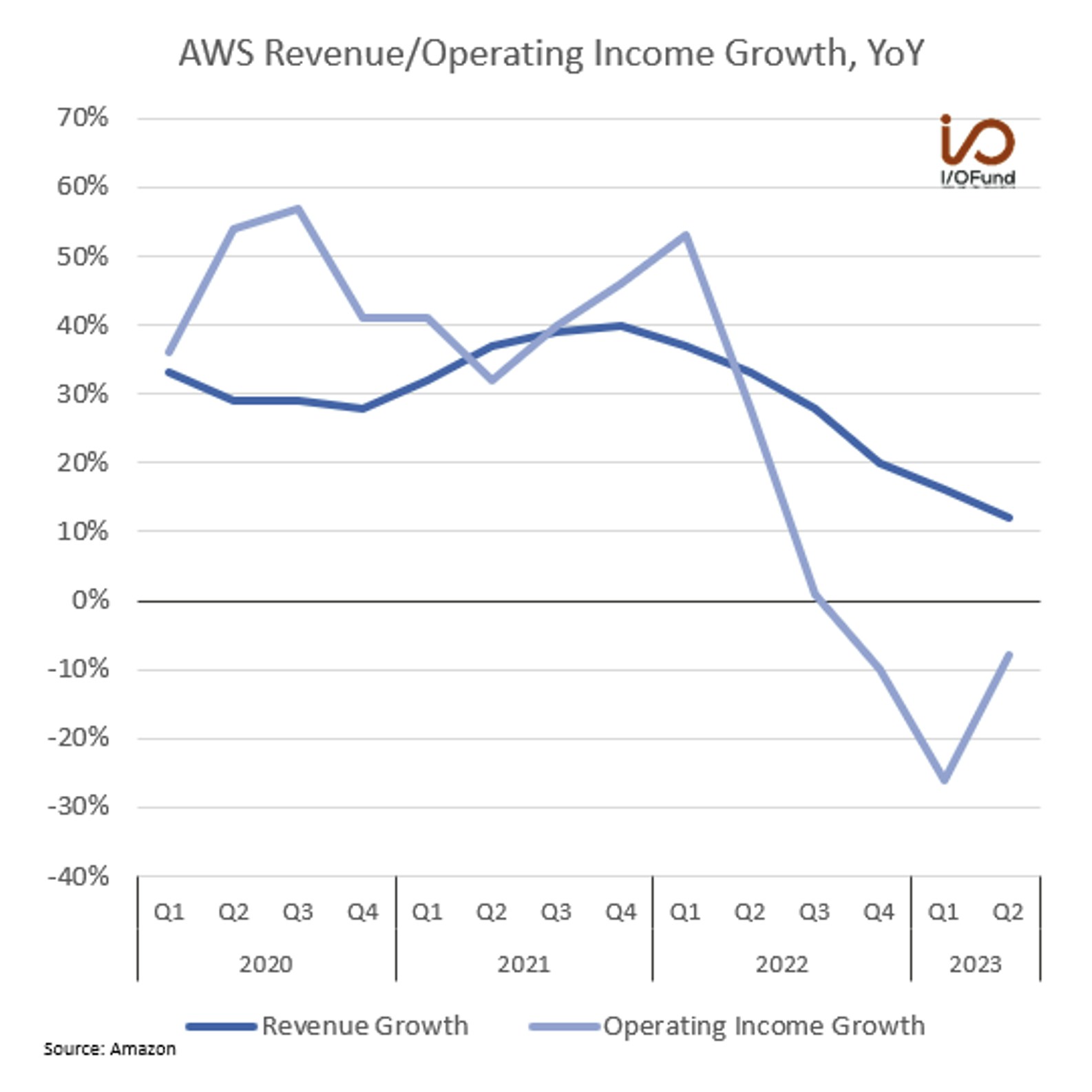

AWS will also be a major focus of the upcoming report, as its revenue growth rate has declined for 7 straight quarters, from 40% growth in Q4 2021 to just12% growth in Q22023. Operating income has declined for three consecutive quarters but is on the verge of inflecting back to growth.

Source: AMAZON

While AWS generates just ~17% of Amazon’s total sales, its influence down the line is increasingly large. In Q2, AWS contributed nearly 70% of Amazon’s $7.7 billion of operating income; on a TTM basis, AWS generated $21.1 billion in operating income, or 119% of Amazon’s total $17.7 billion, weighed down by losses on the e-commerce side.

Given that outsized impact on Amazon’s bottom line, an inflection in both AWS’ revenue growth and a pivot back to growth in operating income will help drive more confidence in Amazon’s high EPS growth rates over the next couple years – earnings are forecast to grow 43% and 41% in FY24 and FY25, respectively. However, should AWS fail to show that inflection in revenue growth and post a fourth consecutive quarter of declining operating income, higher EPS estimates over the next three to four quarters could come under pressure.

Watch the Video: Click Here

Conclusion:

Heightened expectations stemming in part from surging AI interest and cloud spend stabilizing are the major theme heading into Big Tech’s earnings week next week. Meta and Google are forecast to see the strongest revenue accelerations over the next two to three quarters, while Amazon is expected to see a small bump up with AWS’ growth a prime factor. Microsoft’s AI initiatives are expected to drive revenue acceleration over the next four quarters as the company devotes more than 13% of its Capex to AI.

We have buy levels we are targeting for Big Tech, which we share with our premium research members each week as the stocks progress. We believe our target buy levels will set us up for gains in FAANG stocks when the next bull cycle begins. We provide in-depth macro and individual stock analysis so that readers can better understand why we buy/sell. In this market, we frequently take gains. You can learn more here including information on our weekly webinar series, where we review our positions live and discuss some of the top stocks of the week.

Every Thursday at 4:30 pm Eastern, the I/O Fund team holds a webinar for premium members to discuss how to navigate the broad market, as well as various stock entries and exits. We offer trade alerts plus an automated hedging signal. The I/O Fund team is one of the only audited portfolios available to individual investors. Learn more here.

I/O Fund Equity Analyst Damien Robbins contributed to this report.

Recommended Reading:

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i