Nvidia Suppliers Send Mixed Signals for Delays on GB200 Systems – What It Means for NVDA Stock

February 23, 2025

Beth Kindig

Lead Tech Analyst

Nvidia has led the Mag 7 for two years with a return of 853% since Jan of 2023. The second closest Mag 7 return in this time frame is Meta at 495% with all other Mag 7 stocks returning less than 200%, and popular tech ETF QQQ returning 105% in that time frame. All the above is outstanding performance, yet one stock has clearly set itself apart.

Given the spectacular outperformance of more than 7X the QQQs, it goes without saying there is outsized pressure on Nvidia’s stock, whether it’s from short sellers who are still in disbelief, or from investors who are simply wanting to book gains.

Recently, a low-cost large language model (LLM) from China sent the stock down 25% in two days. In the heart of the aftermath, I spoke with Charles Payne on Fox Business News, discussing key reasons investors should stay the course, given cheaper AI development will drive more demand (not less). The stock has nearly recouped its losses, trading 6% below its high before the Deep Seek news broke. Ultimately, Deep Seek is immaterial to AI demand, or perhaps even a net add given AI is too expensive to develop for most developers, resulting in fewer consumer and enterprise applications.

When it comes to Nvidia, there’s no denying the Street gets plenty wrong. Perhaps most egregious was when the Street dropped the stock 60% based on a gaming miss, as Ethereum’s merge to proof of stake in September of 2022 was expected to be the death knell for the AI juggernaut. A month later, the AI GPUs that drove the 7X outperformance shipped. The disconnect was staggering.

The I/O Fund has a strong track record on this stock, discussing every twist and turn publicly for our free stock newsletter readers with documented gains of up to 4,100% as far back as 2018 based on a very-early AI thesis. That gaming miss that resulted in a drop of 60%? We bought that too.

However, it’s important that I pause the exuberance and discuss something stirring beneath the surface. Recently, in this quarterly only, key suppliers are providing mixed guidance on the timing of Nvidia’s Blackwell GB200 systems. The commentary is subtle, and it would require knowing this stock thoroughly to identify the change in tone.

To put it simply, if Blackwell GB200s were ramping, we would see strong sequential growth for Q1. At the very least, there would be some indication Q2 is setting up for strong growth, and yet the commentary is shifting toward a second half discussion. When you add that suppliers do not want to get into the crosshairs with Nvidia, yet are under SEC regulations on how they offer guidance, the language used is incredibly easy to miss.

Ultimately, my spidey senses are up as commentary for Q1 and Q2 should be stronger on the products and solutions that supply Nvidia’s GB200 NVL systems. Meanwhile, Nvidia’s management team is under immense pressure as the company has beat revenue estimates by $1 billion or more for six quarters. This means even a minor delay or minor adjustment in expectations could come under close scrutiny.

As a reminder, we don’t make earnings calls, as many factors can affect stock price. For example, even though I’m getting mixed signals on the timing for GB200 NVL systems, Nvidia’s B200s are ramping, and theoretically can absorb some of this demand.

Instead of making an earnings call, we present quality research so that investors are fully informed to make their own decisions. From there, we take this a step further and publish every single trade we make on our research site. In finance, full transparency is rare, yet through never-ending tenacity, my firm has offered up to 4100% gains on Nvidia alone. We continue this long-standing dedication to our readers in the analysis below.

Nvidia’s Future Hinges on Blackwell – GB200s are the Standout SKUs

Due to the cyclical nature of GPU shipments, the differences in each generation are critical for investors to track. The Hopper generation has driven immense revenue growth over the past two years, while the Blackwell generation is expected to drive revenue that exceeds 2023 and 2024 combined. Hopper brought Nvidia to a $100 billion data center segment – at $26.3 billion in fiscal Q2 2024 – yet I pointed out how Blackwell could drive the data center segment to $200 billion-plus ten months ago.

You can read more about the nuances of each generation of Nvidia’s AI accelerators here, and why Nvidia’s future generations of GPUs can help Nvidia Stock reach $10 Trillion in Market Cap.

The rack-scale GB200 NVL72 features 36 GB200s, or 72 B200 GPUs and 36 Grace CPUs, offering up to 30X inference improvement and up to 5X training improvement versus the HGX H100, with significant improvements in energy efficiency and data processing speeds. The GB200 NVL72 was designed to address and unlock real-time inference for trillion-plus parameter models.

Despite being on an accelerated timeline, Blackwell will deliver the largest leap generationally to date for Nvidia’s AI GPUs.

- The B200 GPU will deliver a 2.5X training improvement and 5X inference improvement over the H100.

- Blackwell will see a massive upgrade in chip size, at 208 billion transistors compared to the H100’s 80 billion transistors.

- The B200 will also have 20 petaflops of FP4 compared to the H100’s 4 petaflops of FP8. I’ve covered the importance of this awhile back, and more recently following DeepSeek.

Blackwell’s pricing power is one of the key factors behind its growth potential, with the GB200 expected to be priced between $60,000 to $70,000, around double the H200’s estimated $32,000 price tag. For rack-scale solutions, the price tags are much heftier – the GB200 NVL36 (featuring 18 GB200s and 18 Grace CPUs) is estimated to carry a $1.8 million price tag, while the GB200 NVL72 is estimated to command an eye-watering $3 million price tag.

Roughly 35,000 NVL72 racks are estimated to be shipped this year, that’s already up to $105 billion in revenue for Nvidia. This volume correlates to shipments of ~2.52 million GB200s, versus Hopper shipments of 2 million-plus in 2024. To note, the revenue and volume do not include the NVL36 racks, B200s, B200As, B300s, and Hopper GPUs still on deck this year.

Nvidia B200s Will Be in High Demand and Likely Ship in Volume in H1

There is certainly a scenario where Nvidia’s GPUs are in such high demand that other SKUs can help make up for a delay on the much-larger GB200 NVL systems. The B200s are expected to be in high demand and companies such as Super Micro are shipping B200 HGX systems in volume. This is one reason Super Micro has seen favorable price action despite lowering their fiscal year guidance; it’s assumed the company can make up for any delays on the GB200s with B200 and B200 HGX systems.

However, the market does not like surprises. As of now, the market is expecting the GB200s to ramp in Q1 and further ramp in volume in Q2. It will be a tall order to meet these expectations (on the dot) with lower priced GPUs and HGX systems.

SECTION TAKEAWAY: Blackwell is a significant undertaking to have 36 GPUs and up to 72 GPUs communicate as one GPU (number depends on the SKU, with complexity increasing if it’s a single rack versus multi-rack configuration). Previously, Nvidia’s AI systems combined 8 GPUs. This significant leap not only increases pricing from roughly $32,000 per GPU to up to $3 million per system, but it also greatly increases the need for new networking architecture and comes with increased power requirements.

Nvidia GB200 Delay Rumors Grow – The I/O Fund’s Take for Q1 & Q2

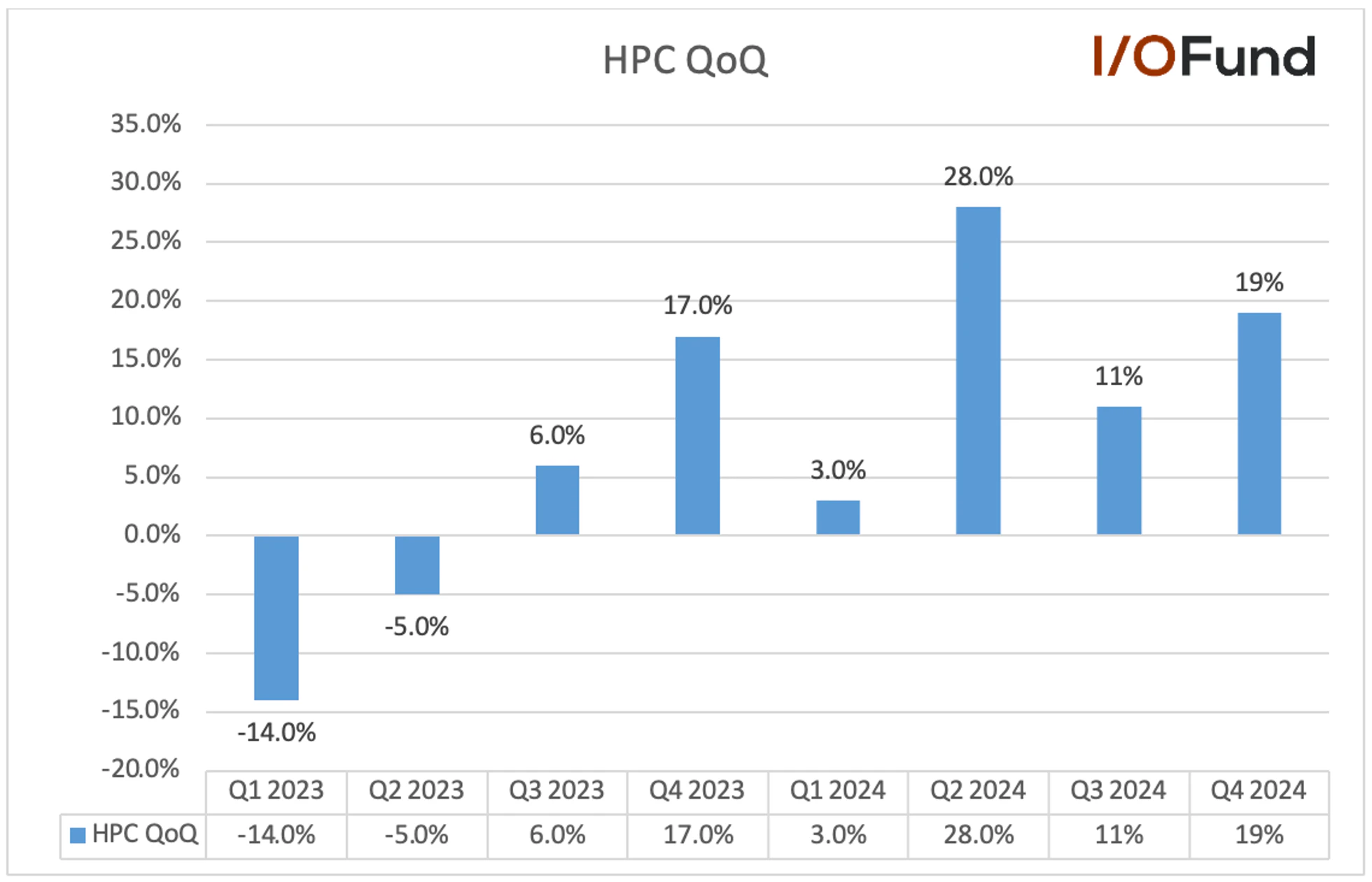

Dating back six months, there have been rumors that the GB200s are delayed. The first rumor came from The Information, stating machines were sitting idle at Taiwan Semiconductor, where Nvidia’s chips are made. I informed my readers at the time this was unlikely to be the case as TSMC was reporting record high-performance computing revenue. In fact, TSMC continues to report strong HPC revenue.

NVDA stock outlook: TSMC shows no signs of idle machines with strong QoQ growth for the HPC segment during Q2 to Q4.

In January, analyst Ming-Chi Kuo reported there were “Short-term Potential Risks in Nvidia and Related Supply Chain,” stating that GB200 NVL72 shipments in 2025 could reach roughly 25,000 to 35,000 racks compared to 50,000 to 80,000 racks from last year. The same analyst reported earlier in the year that “The biggest challenges in NVL72 development mainly stem from the 132kW thermal design point (TDP) requirement, which makes it the highest-power-consuming server in history. Nvidia and its supply chain need more time to solve unprecedented technology issues.”

This post piqued my interest as the emphasis would be outside the foundry. Instead, this would suggest an entirely new delay with thermal management issues (direct liquid cooling), or perhaps with power management solutions, or even networking related --- rather than a material delay related to TSMC and yield issues.

To cross-examine this possibility, below is a brief summary from some of the more well-known direct-liquid cooling suppliers, PMIC suppliers (power management integrated circuits), and a few networking companies outlining commentary that leads to a higher probability there is a delay for the GB200s. If my read-through from these management teams is correct, the delay falls somewhere on the thermal/power solutions or networking components part of the supply chain rather than on TSMC.

Explaining the Lower Rack Shipments of NVL72 Systems

Regarding the statement that the GB200 NVL72 shipments in 2025 could reach roughly 25,000 to 35,000 racks compared to 50,000 to 80,000 racks from last year, I want to take a step back and clarify here that while that would represent a substantial drop, it’s more representative of a significant shift in NVL72 share from last year, and more reflective of what key partner TSMC can handle in terms of CoWoS capacity.

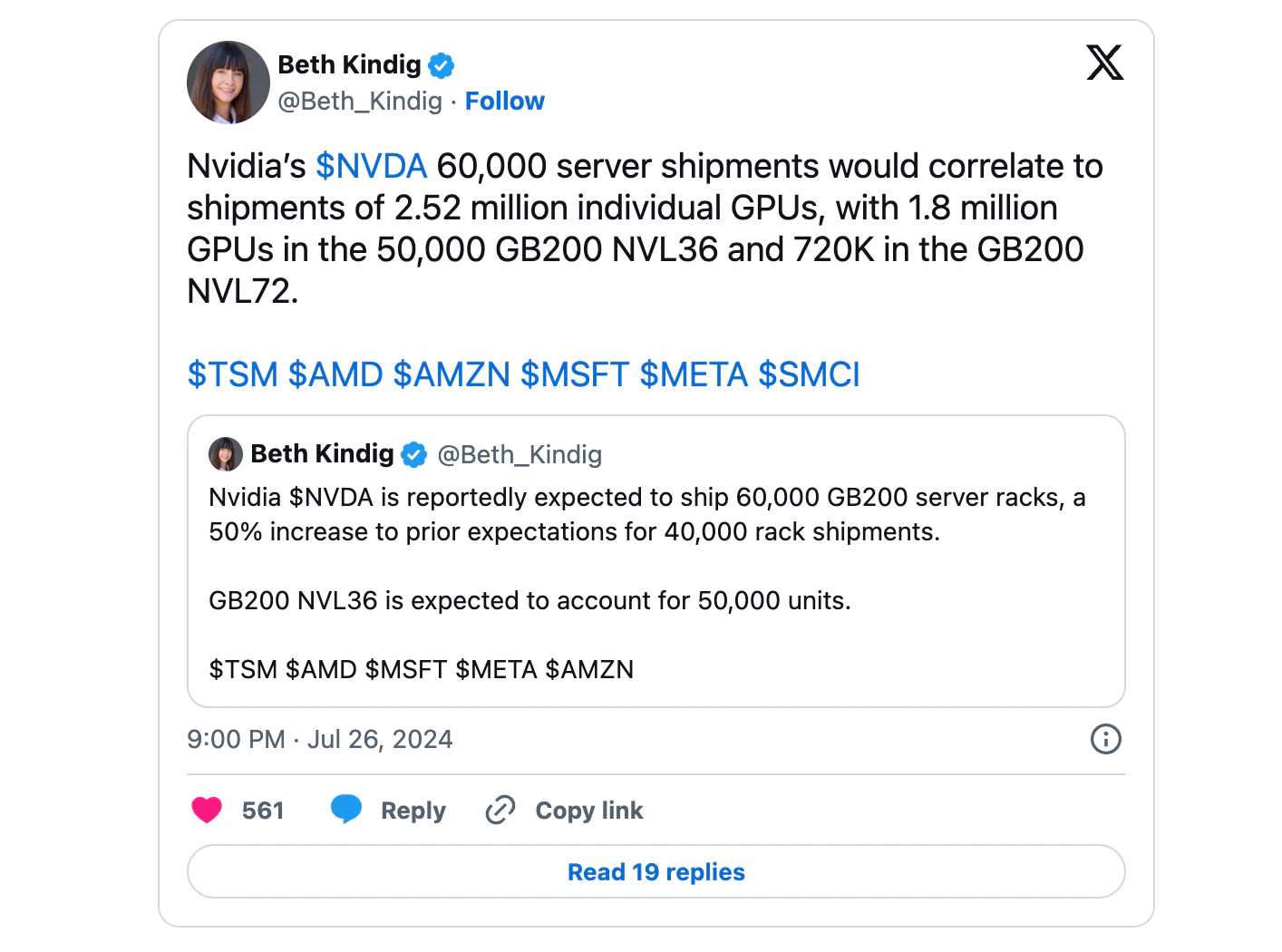

In July of 2024, estimates for GB200 racks were revised 50% higher from 40,000 to 60,000 racks, with the NVL36 at more than 80% share at 50,000 racks with the remaining 10,000 racks to be NVL72.

This would correlate to 2.52 million GPUs shipped – coincidentally, the same amount of GPUs expected to be shipped with 35,000 NVL72 racks, with more on deck from NVL36 configurations.

So, while it may look to be a large decline, GPU shipments at 35,000 NVL72 racks plus additional NVL36 racks would actually be higher than last year’s 60,000 NVL72 and NVL36 estimate due to a large shift towards the NVL72 configuration.

Additionally, the industry’s more recent, most optimistic forecasts for 50,000 to 80,000 NVL72 racks would be unrealistic and practically impossible for TSMC to meet – at the midpoint, this would require ~4.68 million B200 GPUs, or more than 292,000 in CoWoS wafer allocation simply for the NVL72 (not including NVL36).

Current estimates from Morgan Stanley place the B200’s CoWoS allocation at ~220,000 wafers for 2025, or more than 30% of TSMC’s total capacity for the year. This coincides with estimated B200 GPU shipments of 3.52 million, more than enough to handle 35,000 NVL72 racks and similar volumes of NVL36 racks.

SECTION TAKEAWAY:

With what the I/O Fund knows today, the product mix of NVL72 being higher, thus resulting in a lower number of racks being delivered, is not the issue. Rather, it’s the timing that could pose an issue due to Wall Street potentially having to face uncertainty on what quarter NVL systems would ship in volume.

Blackwell Necessitates Direct Liquid Cooling – Super Micro and Vertiv’s Comments

In June, we wrote an analysis on AI Power Consumption: Rapidly Becoming Mission Critical which stated that as the industry progresses towards a million-GPU scale, more emphasis is placed on future AI GPU generations to focus on power efficiency while delivering increasing levels of compute. Data centers are expected to adopt liquid cooling technologies to meet the cooling requirements to house these increasingly large GPU clusters, and the percentage of air-cooled systems shipped versus liquid cooled systems will change (dramatically) with Blackwell’s NVL systems.

Therefore, any changes to Blackwell’s NVL systems timing would appear in commentary from companies that provide direct-liquid cooling solutions and servers, as the previous generations are air cooled.

Super Micro Lowers FY25 Revenue Guide, Pushes Back 30% Liquid Cooling Target

Super Micro recently reported preliminary fiscal Q2 results, in which it cut its fiscal 2025 revenue guide while hinting that Blackwell GPUs could take longer to ramp in the first part of the calendar year.

At Computex in June 2024, CEO Charles Liang stated that he “expects 15 percent of racks [SMCI] sells this year to use DLC, and 30 percent to employ it [in 2025].” In August 2024, Liang slightly changed his tune, noting that they now expect “25% to 30% of the new global datacenter deployments to use DLC solutions in the next 12 months.”

I remember this comment well, as it was part of the evidence used to debunk the August rumors considering SMCI had moved up their timeline for DLC delivery (from end of year 2025 to mid-year 2025).

Two weeks ago in the February 2025 report, this timeline was shifted back with Liang stating that Super Micro now believes that “DLC or overall liquid cooling market share will grow all the way to 30% or even more in the next 12 months” -- it’s not a dramatic shift in tone but rather pushes the 30% target back from mid-year 2025 noted in August, to beyond the original year-end timeline --- to now technically being early 2026.

The August earnings call also housed one critical piece of information regarding Blackwell and Super Micro’s 2025 revenue. Wells Fargo’s Aaron Rakers questioned management about Blackwell and guidance for December 2024 and onwards. Liang explained that for the December quarter, Blackwell “will be very small. Engineering sample small volume. So the real volume, I believe, had to be March quarter next year. And that's why we foresee only $26 billion to $30 billion.”

But now, SMCI implied they are not able to ship Blackwell in the March quarter:

“Do you guys have a forecast from NVIDIA? You know when you think you're going to start to see you know supply the GPU, so that you can ship the NVL72 where visibility is still pretty low on availability of the GPUs?

Sign up for I/O Fund's free newsletter with gains of up to 2600% because of Nvidia's epic run - Click here

Charles Liang

We already proved pretty much everything. And now, just waiting for – and we are in some allocation, some volume, but the volume demand is way much bigger. So we are waiting for more allocation. So hopefully very soon we can ship in much higher volume."

Super Micro revised its FY25 guidance lower at the beginning of last week, now seeing revenue of $23.5 billion to $25.0 billion, or more than 13% lower than the initial guide at midpoint. Q3 revenue was guided between $5 billion and $6 billion, below the $5.95 billion estimate. A weaker-than-expected March and FY25 guide plays into management’s comments of a lack of Blackwell NVL72 availability, with Super Micro only just beginning volume shipments of Blackwell-based racks:

Q: Jon Tanwanteng, CJS Securities: “I was wondering if you could break down the factors ...driving the reduction in the 2025 revenue guidance. How much is maybe pricing related? How much do you think is related to delays or availability of Blackwell?”

A: David Weigand, Super Micro CFO: “Yeah, I would say, Jon, that probably the biggest factor was just the delay in new technology because we were, when you think about it, we were all set to go. We were all set to ship with liquid cooling. We were ready. But the problem was that not everything else was.”

This was corroborated by Liang:

“Once Blackwell [is] in volume production, I believe we will have strong growth. And now we are just preparing, diligently preparing all the logistics, including the system enclosure, thermal solution, for sure GPU supply from our vendor Nvidia. So we are well prepared and once logistics ready, we are ready to ramp up our growth.”

Super Micro has walked back the revenue guide that hinged on Blackwell’s NVL systems shipping in volume in the March quarter. Management was also quite clear that the new product was facing a delay as they await more GPU supply.

Vertiv Signals Softer Q1

Vertiv is a provider of thermal and power management solutions and is a leader in direct liquid cooling. The company stated they benefited from a “particularly strong” Q4, with revenue rising nearly 26% YoY as they overdelivered by nearly $200 million as customers wanted products as soon as possible.

Vertiv’s strength in Q4 may be tied to key partner Dell, as its AI server backlog in fiscal Q3 (October quarter) rose more than 18% QoQ to $4.5 billion after being flat QoQ in Q2, and its AI pipeline rising more than 50% QoQ. Analysts placed Dell’s AI server pipeline at $16 to $17 billion, up from $11 to $13 billion previously, a rather large jump for one quarter. However, Dell noted that one factor for its softer Q4 and fiscal year guide was the “unpredictability of the AI shipments” as there are “some more timing differences than what we were anticipating when we gave the guide the last quarter.”

For Q1, Vertiv guided a deceleration to 19% YoY growth, with FY25 revenue growth guided at 16%. Management defended this deceleration into Q1 by saying: “Now of course, Q4 was particularly strong. So we should not look at Q1 as a quarter-to-quarter, really look at the first quarter sales as the acceleration that has taken place. With a 19% organic growth in the first quarter, I feel very, very good about what that tells us about our overall trajectory” and also that it is “higher than what we actually saw in 2024.”

Liquid cooling capacity is not a constraint for Vertiv, as they had said last summer that they were “on track to finish in 2024 with a 45x capacity increase compared to baseline at the end of 2023.”

I agree with the analyst sentiment (and weak price action) following the report that the commentary doesn’t check out exactly. Per I/O Fund numbers, management is contradicting itself by guiding for organic growth of 19% at the midpoint for Q1 but 16% growth for the fiscal year (i.e., slower growth later in the year) while stating shipments will increase QoQ.

Additionally, the QoQ/YoY has to be looked at which is lower than what typical seasonality would account for, as our numbers indicate Vertiv was down (12.1%) due to seasonal sequential growth from Q4-Q1. This year, Vertiv is down (16.9%) from Q4-Q1.

My conclusion (still to be confirmed) is that Vertiv may see a weak Q2 before there is an acceleration into the back half.

One Q&A exchange in Q4’s call voiced these concerns:

Q: Steve Tusa, JP Morgan: “Obviously, there's a lot of focus on orders, I think, for good reason. Everybody's trying to discern the trend relative to these CapEx numbers, the pipelines that are obviously pretty eye-popping. You're now two quarters step down relative to what we see at your customers and the way they're spending in these pipelines. What is that disconnect? Is there some sort of disconnect between you guys and everybody else talking about doubling their data center businesses?”

A: Giordano Albertazzi, Vertiv CEO: “I don't think there is a disconnect, quite honestly. If you look at our orders trajectory last year, if you think about a 60% year-on-year growth in the first half of the last year, that's a lot of growth. When our customers talk about their CapEx, of course, they also talk about a lot of the silicon part of their CapEx, not all the data centers. So, I feel pretty good about our visibility of the market and what we win in the market.”

Networking Companies Shift Tone on Timing for GB200s

Please note: the full research including company names, management statements and stock tickers are provided to our research members We offer a more generalized discussion below.

PCIe 6.0 supplier:

PCIe 6.0 is a networking standard expected to initially ship with Nvidia’s Blackwell. A key supplier stated to expect this in the second half of the year, as these products “are driving higher dollar content opportunities [...] on a full rack and full accelerator basis and we expect volume deployments to begin in the second half of this year.”

Revealed at GTC in March of 2024, PCIe 6.0 was initially expected to launch with the GB200s. The following quote from this supplier also hints that merchant GPUs (Nvidia) will not be driving H1 – which would be odd if Blackwell was shipping. “Now, if you look into 2025, we see both contributing growth. The first half of the year will be more predominantly the internal AI accelerator programs. But if you get into the back half of the year, the transition on the merchant GPUs will also be very strong for us. This is where you'll see the custom rack configurations start to deploy and that’s where we see a big dollar increase in our contemporary GPU with [our product] starting to ramp.”

PMIC Suppliers:

PMICs (power management integrated circuits) are a critical part of the picture for Blackwell, given that these components were linked to Blackwell’s rumored power management issues. Major PMIC suppliers were unable to confirm volume shipments in the first quarter in recent earnings calls.

One PMIC supplier that we covered on our Advanced site on Feb 5th, is stating that “We know that we're not the only one players going after this, so the share is still to be determined. The final design, everything is still to be finalized as well, too. So we're working closely with the customer. Again, at this point, we can say that we're targeting for a mid-year launch.”

This company is either discussing Blackwell Ultra with the B300s, or they are implying GB200s are delayed.

The competing PMIC supplier stated: “Just to add a little bit of color to how we see the year rolling out, we believe that we will be off to a slower start in the first half of the year. But as the year develops, the customer base is expected to broaden as hyperscalers launch their new products. We have multiple product ramps with both existing customers as well as with these new hyperscalers.”

The takeaway is that neither PMIC supplier can confirm they are shipping in volume in Q1 or Q2, yet meanwhile, both are saying they are still part of the supply chain.

Semtech Suddenly Pulls Guidance on Active Copper Cabling (ACCs)

Perhaps the most drastic commentary to come out of the last few weeks was when a key supplier pulled its Q1 guidance intra-quarter.

Semtech filed an 8-K stating that “net sales from its CopperEdge products used in active copper cables are expected to be lower than the Company’s previously disclosed floor case estimate of $50 million due to rack architecture changes, with no expected ramp-up over the course of fiscal year 2026.”

ACC content had been estimated to be substantially higher with 36x2 configurations – it had been rumored back in October 2024 that Nvidia was halting development of one of the NVL72 configurations, the NVL36x2, which linked two 36 GPU racks together in a side-by-side system. Semtech pulling guidance strengthens this view.

The shift in architecture to discontinue the 36x2 configuration was said to possibly “disrupt the supply chain for assembly and cooling solutions,” by removing dual-rack configurations and focusing solely on single-rack NVL72 and NVL36 configurations. DLC suppliers have been pushing back Blackwell’s ramp later in the year, suggesting that the market may have faced some impacts from this rumored design change late last year.

While shifting architectures is not a big deal in the medium-term (as stated above, NVL72 single rack configurations are expected to see a higher mix); it’s the suddenness that Semtech pulled it’s guidance that is cause for concern as the company had reaffirmed its optimistic revenue floor guidance based on two factors – the timing of Blackwell’s launch and changes in rack design. This suggests both factors may be in play, as a late-stage design change was expected to have downstream impacts on timing for DLC ramping.

Potential Flat Q1 or Flat Q2

A week after we began covering the topic for our research members, Mizuho’s Vijay Rakesh stated he is expecting a “more flattish” Q1 with data center revenue of $36.7 billion versus $37.4 billion consensus.

To reiterate, if there is an issue, it will appear in Q1 or Q2 according to management commentary provided above. For Q4, the QoQ growth in the data center is expected to be $2.6 billion, compared to $4.5 billion QoQ from Q3-Q4.

What to Look for in Nvidia’s Q4 Report

We have yet to see a DLC supplier come in strong, so we believe the risk is elevated that Nvidia reports a weaker-than-expected Q1 or Q2 as the B200s absorbing a timing delay on the GB200s is a tall order.

In terms of the GB200s shipping on time, I’m open to this – and highly prefer it, given I continue to hold a large Nvidia position. However, I can't find clear evidence in the supply chain that these larger systems are ramping for a strong Q1 performance.

HP Enterprise stated that they’ve only now shipped their first Blackwell based system, while Super Micro walked back its FY25 guidance in part due to a soft fiscal Q3, which they had previously said would be when Blackwell increases in volume.

Combined with comments from Vertiv and Dell, as well as other suppliers noted in this analysis, there appears to be an air pocket, of sorts. A quarter that doesn't blow it out of the water would be unusual for Nvidia as it has consistently smashed expectations since Hopper’s breakout quarter in 2023.

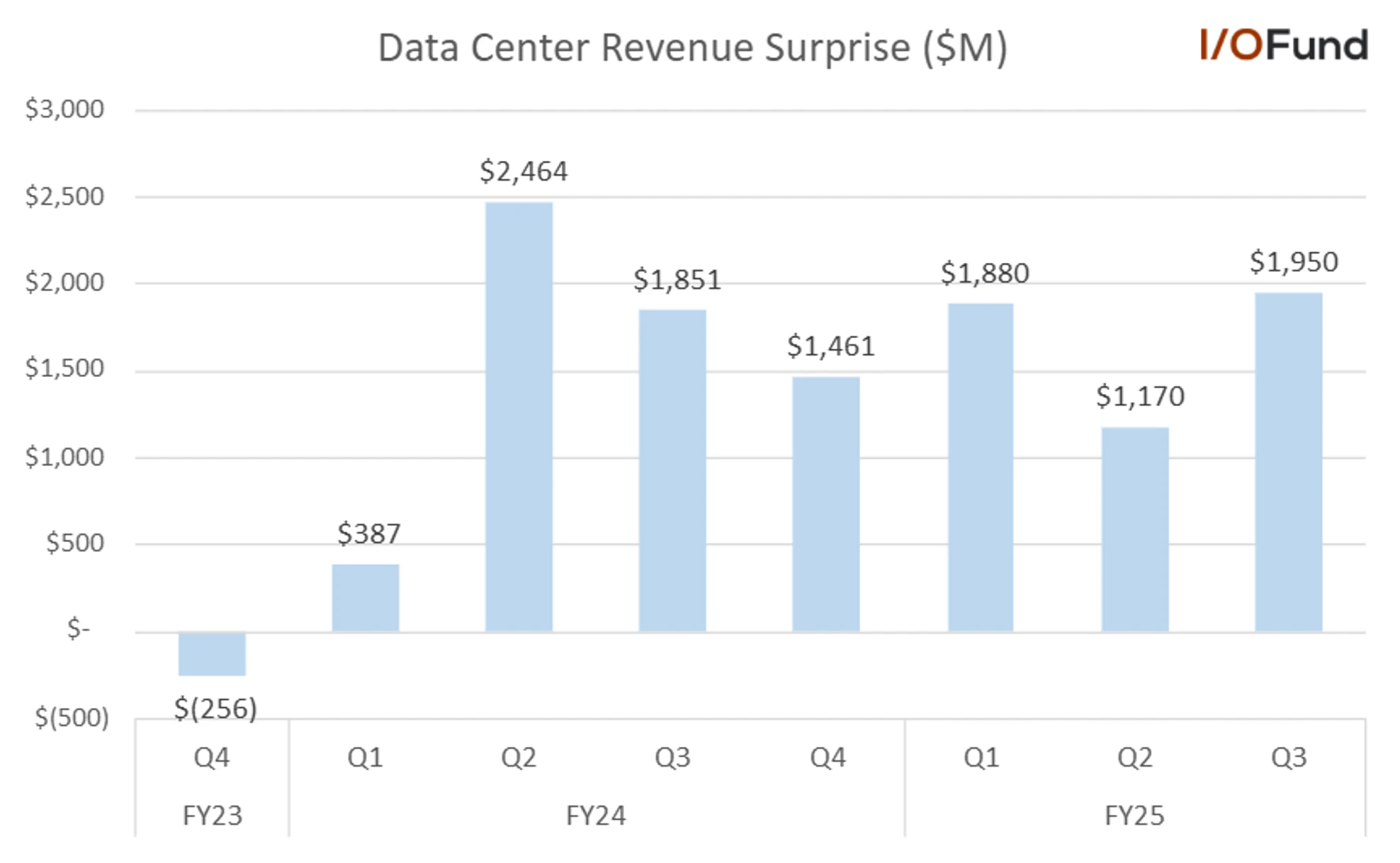

On that note, Nvidia’s data center revenue has consistently exceeded expectations by at least $1 billion or more for six consecutive quarters, with fiscal Q2 ‘24 being the largest at a nearly $2.5 billion beat. Last quarter, fiscal Q3 ‘25, was the second largest at nearly $2 billion.

Nvidia’s Q2 ‘24 saw the largest beat at $2.5 billion, while Q3 ‘25 followed with a nearly $2 billion surprise, driven by strong demand for Hopper

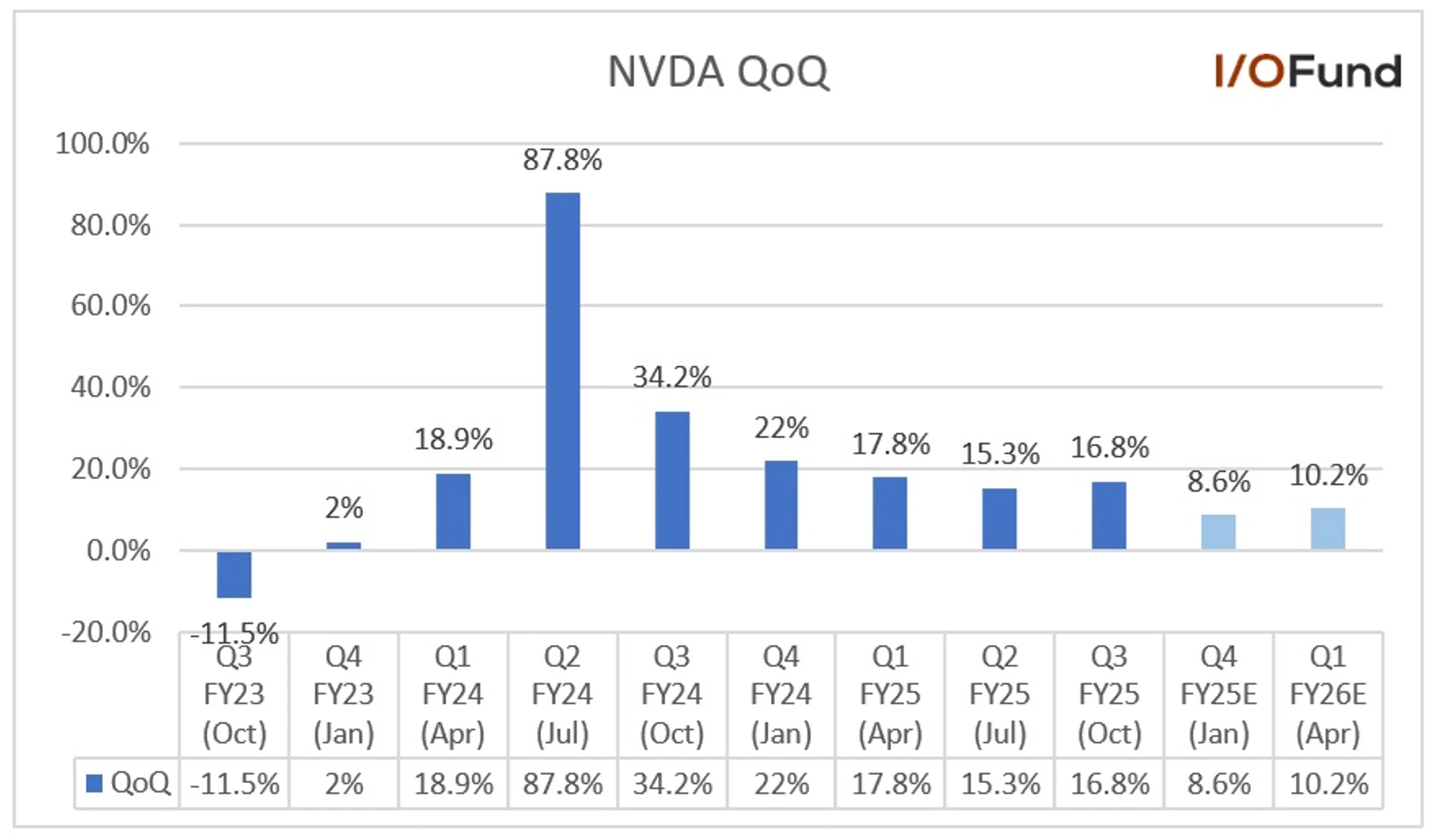

This has driven a string of impressive top-line beats each quarter, with the smallest revenue beat being $1.29 billion in fiscal Q2 ‘25. The shrinking size of revenue beats in that quarter correlated to a deceleration in QoQ revenue growth to 15.3%, one factor behind the more than 6% decline Nvidia felt the day following that report.

For the upcoming fiscal Q4 report, revenue is expected to be $38.1 billion, for QoQ growth of 8.6% while Q1 ‘26 is expected to see revenue of $41.98 billion, for QoQ growth of 10.2%.

Conclusion:

Given market jitters around DeepSeek, which turned out to be a non-issue, something more material related to the GB200s, such as growth slowing below expectations at the start of the new fiscal year, could send the stock below $100 -- which we would see as a buying opportunity. We provided a more detailed buy plan before the earnings season began in the article “Where I Plan To Buy Nvidia Stock Next”

There is a scenario where Nvidia’s stock marches higher – perhaps based on the remaining strength from Hopper and the B200s, B200 HGX systems and B200As packaged with CoWoS-S and having a lower thermal design power (TDP). Or perhaps the string of suppliers discussed here are simply stating the GB200s are not ramping in volume in Q1 but will in Q2. Even still, I prefer to wait to see how this resolves as my firm has been tracking key suppliers and AI proxies for six years to confidently build our positions.

Ultimately, my firm trimmed our Nvidia position (to a 10% allocation) and will happily buy lower should the assumptions in this analysis materialize. Nvidia remains the stock of the decade; however, stock returns – and product launches -- are not perfectly linear.

The I/O Fund has recently added five new small and mid-cap positions poised to benefit from the ongoing AI spending war. Join us every Thursday at 4:30 p.m. for our exclusive 1-hour webinar, where we cover market entries, exits, and key insights on the broader market. Take advantage of $50 off our Advanced monthly service, now priced at $99/month. Use Code SAVE50ADV through Feb 28th Midnight

Disclosure: The I/O Fund owns Nvidia and a handful of Nvidia suppliers including some of the suppliers listed in this analysis. To view the full portfolio, subscribe here.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund own shares in NVDA at the time of writing and may own stocks pictured in the charts.

Recommended Reading:

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su